Question

Answer

a)

(i)

Without the bonus issue this would give an EPS of 30p (13.8m/46m x 100).

The bonus issue of one for four would result in 12 million new shares giving a

total number of ordinary shares of 60 million. The dilutive effect of the bonus

issue would reduce the EPS to 24p (30p x 48m/60m).

The comparative EPS (for 2013) would be restated at 20p (25p x 48m/60m).

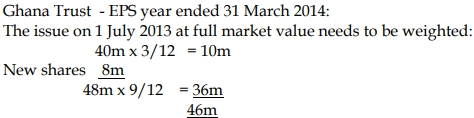

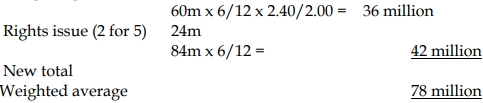

EPS year ended 31 March 2015:

The rights issue of two for five on 1 October 2014 is half way through the

year. The theoretical ex rights value can be calculated as:

Weighting:

EPS is therefore 25P (GHC19.5m/78m x 100).

The comparative (for 2014) would be restated at 20P (24Px 2.00/2.40).

(ii) The basic EPS for the year ended 31 December 2015 is 30p (GHC25.2m/84m x

100).

Dilution

Convertible loan stock:

- On conversion, loan interest of GH¢1.2 million after tax would be saved (GH¢20 million x 8% x (100% – 25%)), and a further 10 million shares would be issued (GH¢20m/GH¢100 x 50).

Directors’ options:

- Options for 12 million shares at GH¢1.50 each would yield proceeds of GH¢18 million. At the average market price of GH¢2.50 per share, this would purchase 7.2 million shares (GH¢18m/GH¢2.50). Therefore, the ‘bonus’ element of the options is 4.8 million shares (12m – 7.2m).

Using the above figures, the diluted EPS for the year ended 31st December 2015 is 26.7p (GH¢25.2m + GH¢1.2m)/(84m + 10m + 4.8m).