Question

Answer

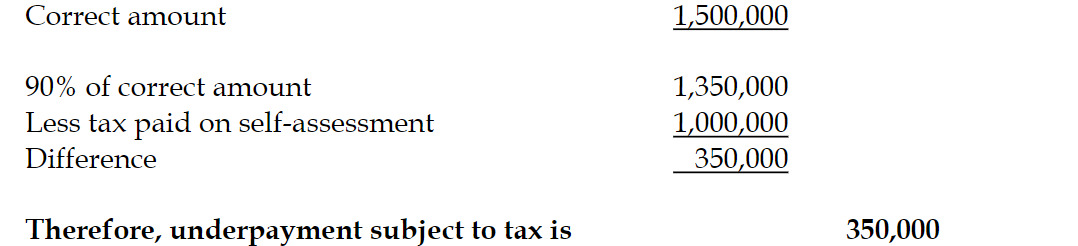

Computation of underpayment to be subjected to

Therefore, underpayment subject to tax is 350,000

(2 marks)

c) The following data is relevant to Naab Ltd tax affairs for 2018 year of assessment:

Self-assessment returns submitted:

Tax paid on self-assessment: GH¢1,000,000

Chargeable income: GH¢4,000,000

Actual Returns submitted:

Chargeable Income: GH¢6,000,000

Correct amount – Tax payable: GH¢1,500,000

Required:

What is the amount of tax underpayment to be subject to interest computation?

(2 marks)

Computation of underpayment to be subjected to

Therefore, underpayment subject to tax is 350,000

(2 marks)

Explain the following as used in tax administration:

i) Self-Assessment

ii) Pre-emptive Assessment

iii) Administrative Assessment

iv) Tax Audit Assessment

(10 marks)

i) Self-Assessment:

ii) Pre-emptive Assessment:

iii) Administrative Assessment:

iv) Tax Audit Assessment:

State TWO (2) advantages each of self-assessment to the government and the taxpayer. (5 marks)

Advantages to the Government:

Advantages to the Taxpayer:

Paa Tee is a sole proprietor and has not filed his tax returns for 2018 year of assessment as at April 1, 2019. He has approached you to file his tax returns for him and from all indications, he has paid all his taxes based on the self-assessment estimate.

Required:

i) What steps (if any) will you take to enable Paa Tee file his tax return and are there any financial implications in filing? (2 marks)

ii) What factors may give rise to an adjusted assessment by the Commissioner-General?

i) I would help Paa Tee apply for an extension if there are valid reasons for doing so, but the application must be made before the deadline of 30th April 2019. There is no financial implication if the filing is done on or before 30th April 2019, or if an extension is granted by the Ghana Revenue Authority.

(2 marks)

ii) The factors that may give rise to an adjusted assessment by the Commissioner-General are:

The Income Tax Act, 2015 (Act 896), as amended, requires all taxpayers to be on self-assessment as taxpayers know better their circumstances for tax purposes.

Required:

Evaluate FOUR (4) benefits of the self-assessment regime.

The self-assessment regime offers the following benefits:

Ghana Revenue Authority has embarked on comprehensive reforms geared towards “Voluntary Tax Compliance.” Among the reforms is requesting taxpayers to determine their tax liabilities and consequently the tax payable. This has been criticized by some taxpayers as increasing the cost of compliance or doing business. You have been engaged by the Ministry of Finance to help Ghana Revenue Authority educate taxpayers on these reforms.

You are required to explain to taxpayers:

i. Self-Assessment Tax Regime.

(4 marks)

ii. Critically examine the benefits taxpayers stand to derive from the Self-Assessment Regime that has become part of tax administration in Ghana.

(6 marks)

i. Self-Assessment Tax Regime

Self-assessment regime is a type of assessment regime where a taxpayer is made responsible for accurately computing and reporting their tax liability. The taxpayers are required to estimate their taxable income and the tax thereon for the year of assessment. Taxpayers on self-assessment may file revisions of their estimates and pay taxes in accordance with section 80 of the Internal Revenue Act 2000, Act 592 accordingly.

i. Persons on self assessment are persons specified in a notice published in the Gazette

or in a print media by the Commissioner General

ii. An estimate furnished under a revised estimate to the Commissioner General shall

remain in force until revised by the person together with a statement of reason for

the revision

iii. Where the Commissioner General is not satisfied with the estimate or revised

estimate, the Commissioner General may set aside the estimated assessment and

provisionally assess the person

(4 marks)

ii. Benefits of Self-Assessment

The benefits include but are not limited to the following:

a)

i) Explain the terms “Provisional Assessment” and “Self Assessment” in tax administration. (6 marks)

ii) Discuss the rationale for the shift from Provisional Assessment to Self Assessment. (8 marks)

a)

i) Provisional Assessment

Self Assessment

ii) Rationale for the Shift from Provisional Assessment to Self Assessment

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.