Question

Answer

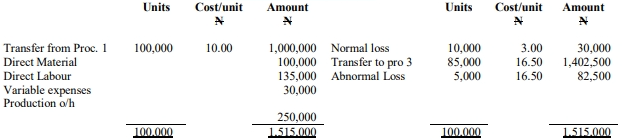

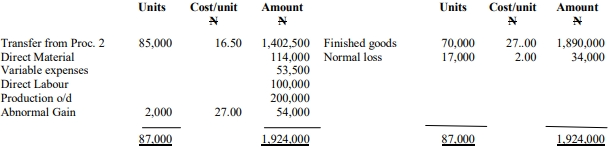

MAPUTO NIGERIA LIMTED

PROCESS 2 ACCOUNTS

a

i)

PROCESS 3 ACCOUNTS

ii)

b) NORMAL LOSS ACCOUNT

c) ABNORMAL LOSS ACCOUNT

ABNORMAL GAIN ACCOUNT

MAPUTO NIGERIA LIMITED manufactures its product through three processes. The following data relates to Process 2 and Process 3 for the month of October:

| Cost Components | Process 2 (N) | Process 3 (N) |

|---|---|---|

| Direct Materials | 100,000 | 114,000 |

| Direct Labour | 135,000 | 100,000 |

| Variable Expenses | 30,000 | 53,500 |

| Production Overhead | 250,000 | 200,000 |

Required:

a. Prepare Process 2 and Process 3 accounts (16 Marks)

b. Prepare the Normal Loss account (2 Marks)

c. Prepare the Abnormal Gain account (2 Marks)

MAPUTO NIGERIA LIMTED

PROCESS 2 ACCOUNTS

a

i)

PROCESS 3 ACCOUNTS

ii)

b) NORMAL LOSS ACCOUNT

c) ABNORMAL LOSS ACCOUNT

ABNORMAL GAIN ACCOUNT

Mawuena Ltd, a manufacturer of building materials, has recently suffered falling demand due to economic recession, and thus has unutilised capacity. Management has identified an opportunity to produce designer ceramic tiles for the home improvement market. It has already paid GH¢1.5 million for development expenditure, market research, and feasibility studies.

A new machine, with a useful life of four years, could be bought at GH¢6.5 million, payable immediately. The scrap value of the machine is expected to be 5% of the cost, recoverable a year after the end of the project.

The research and development division has prepared the following demand forecast:

| Year | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| Demand (units) | 110,000 | 130,000 | 150,000 | 145,000 |

The selling price is GH¢50 per box (at today’s price). Estimated operating costs, largely based on experience, are as follows:

| Cost per box of tiles (at today’s price) | GH¢ |

|---|---|

| Materials cost | 12.00 |

| Direct labour | 5.00 |

| Variable overhead | 2.50 |

| Fixed overhead (allocated) | 3.50 |

| Distribution (Variable) | 5.50 |

In addition to the initial cost of machinery, investment in working capital of GH¢0.2 million will be required in year two. Mawuena Ltd pays tax one year in arrears at an annual rate of 30% on returns from the project. Mawuena Ltd shareholders require a nominal return of 14% per annum after tax, which includes allowance for generally expected inflation of 5.55% per annum. (Ignore Capital Allowance).

Required:

Assess the financial desirability of this venture in real terms, computing the net present value offered by the project. (14 marks)

You should recognize that the proposed venture is to be assessed in real terms rather than money terms. This involves deflating the money terms discount rate and applying this to uninflated cashflows. You should also take care to include only relevant cashflows and to include the stated rate of taxation.

The real rate of return is calculated as:

(1+m)=(1+r)×(1+i)

Where m = money rate, r = real rate, i = inflation

In the case of this project, this becomes:

(1 + 0.14)=(1 + r)×(1 + 0.0555)

r= 8%

Allocated overheads are not relevant to this analysis as they will arise regardless of the decision being made.

The relevant operating costs per box are calculated as follows:

| GH¢ | |

|---|---|

| Materials cost | 12.00 |

| Direct labour | 5.00 |

| Variable overhead | 2.50 |

| Distribution, etc | 5.50 |

| Total | 25.00 |

Year-by-year cash flows and their discount factors:

| Year | 0 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|

| GH¢’000 | ||||||

| Sales revenue | 5,500 | 6,500 | 7,500 | 7,250 | ||

| Variable cost | 2,750 | 3,250 | 3,750 | 3,625 | ||

| Contribution | 2,750 | 3,250 | 3,750 | 3,625 | ||

| Tax (30%) | (825) | (975) | (1,125) | (1,087.5) | ||

| Net Contribution | 2,750 | 2,425 | 2,775 | 2,500 | (1,087.5) | |

| Initial investment | (6,500) | |||||

| Scrap value | 325 | |||||

| Working capital | (200) | 200 | ||||

| Free Cash Flow | (6,500) | 2,750 | 2,225 | 2,775 | 2,700 | (762.5) |

| Discount Factor (8%) | 1.00 | 0.926 | 0.857 | 0.794 | 0.735 | 0.681 |

| Present Value (GH¢’000) | (6,500) | 2,546.5 | 1,906.83 | 2,203.35 | 1,984.5 | (519.26) |

Net Present Value (NPV): GH¢1,621.92 million

As the net present value is positive, the project should be taken on.

Note: Initial research costs are sunk costs and should be excluded.

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.