Question

b) Sasraku Ltd manufactures and sells standard quality fuel pumps. Other companies integrate these pumps in their production of petrol engines. At present, Sasraku Ltd manufactures only three different types of fuel pumps: oil pump, gas pump, and diesel pump. Simon, the Management Accountant, allocates fixed overheads to these pumps on an absorption costing system.

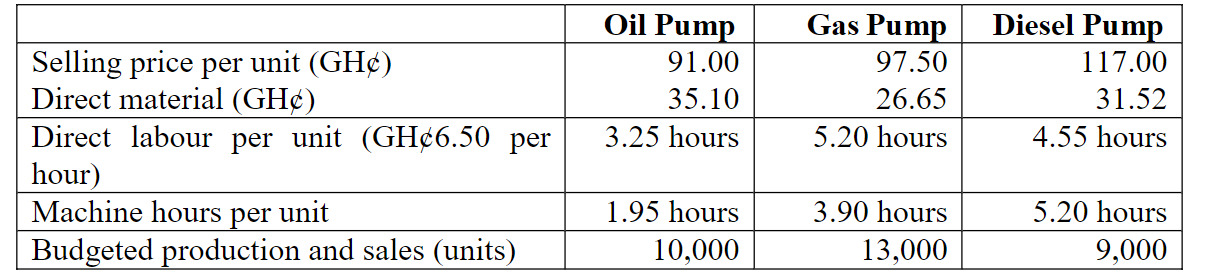

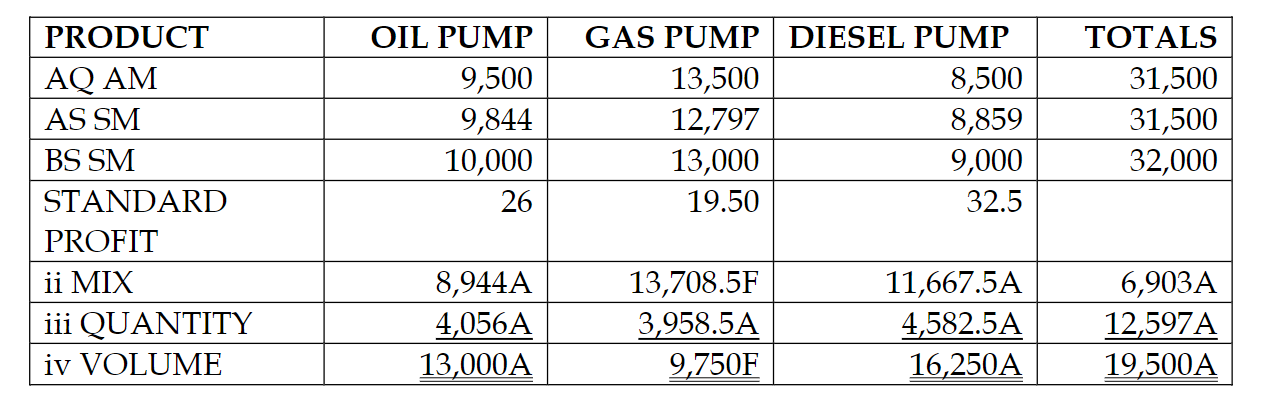

The standard selling price, volumes, and cost data for these three products for the last period are as follows:

The total fixed production overhead for the last period was estimated in the budget to be GH¢526,500. This was absorbed on a machine-hour basis.

The Board of Directors has decided to calculate the variances for the period to analyze the sales performance of the company.

The following information of actual volumes and selling prices for the three products in the last period was obtained:

Required:

i) Calculate the standard profit per unit.

(3 marks)

ii) Calculate the following variances for overall sales for the last period:

Sales profit margin variance

Sales mix profit variance

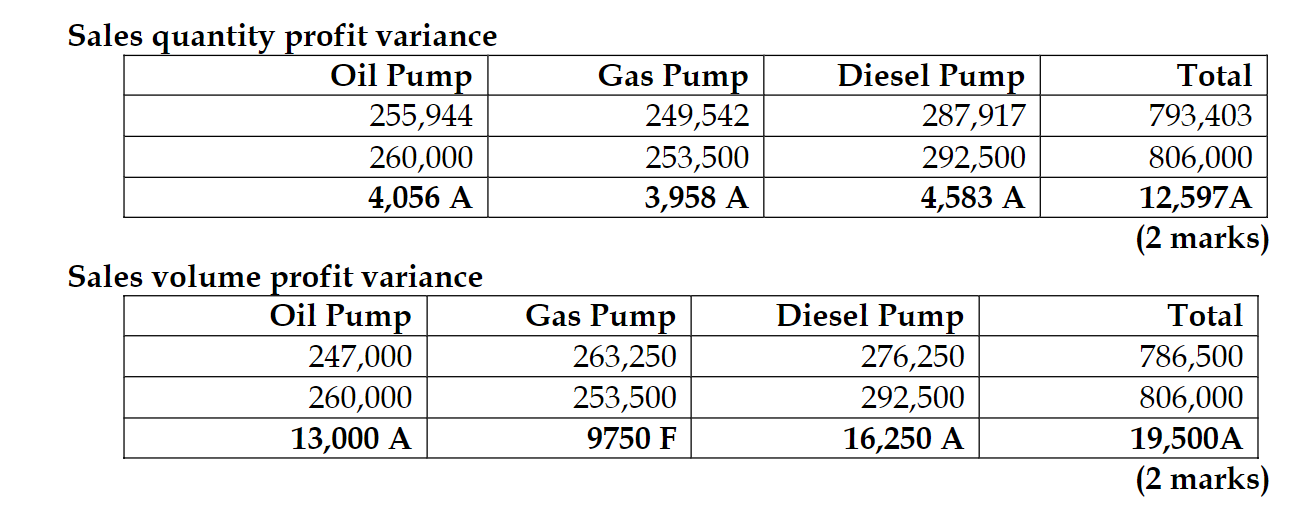

Sales quantity profit variance

Sales volume profit variance

(8 marks)

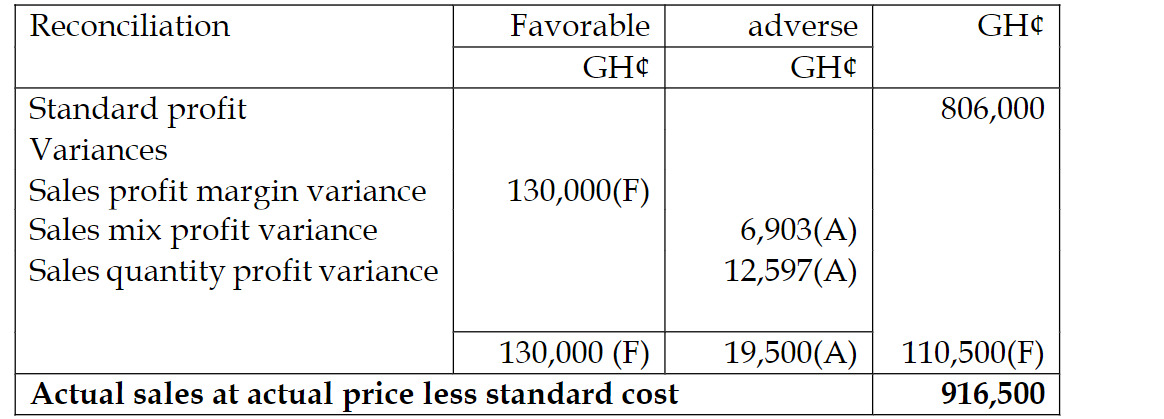

iii) Prepare a statement showing the reconciliation of budgeted profit for the period to actual sales less standard cost

(4 marks)

Answer

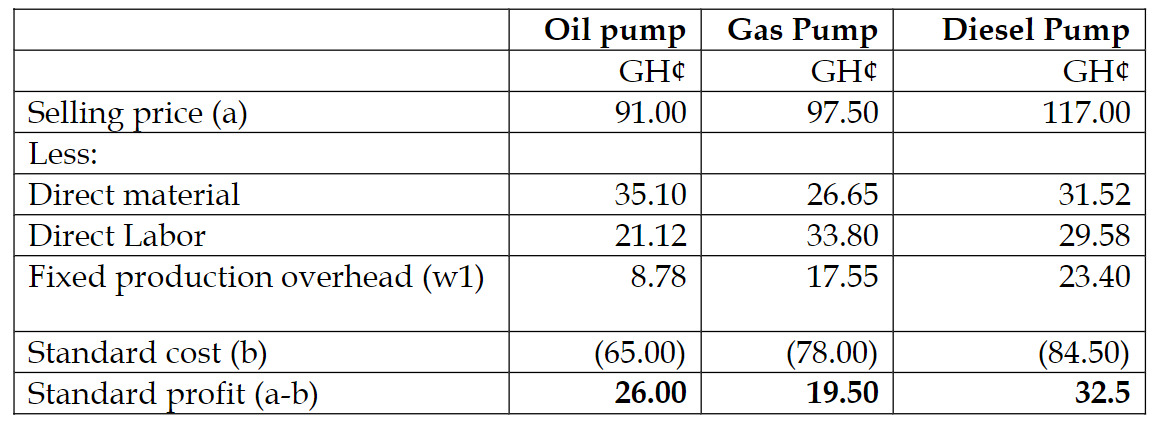

i) Calculation of standard profit per unit

Working

W1 calculation of overhead absorption rate Budget machine hours = (10,000*1.95) + (13,000*3.90) + (9,000*5.20) =117,000 hours As company follows absorption costing method, fixed overheads are allocated don

machine hours’ basis. Overhead adsorption rate = GH¢526,500/117,000 hours = GH¢4.50 per machine hour.

(3 marks evenly spread using ticks)

ii)

- Actual sales quantity at actual profit margin (at actual selling price less

standard cost)

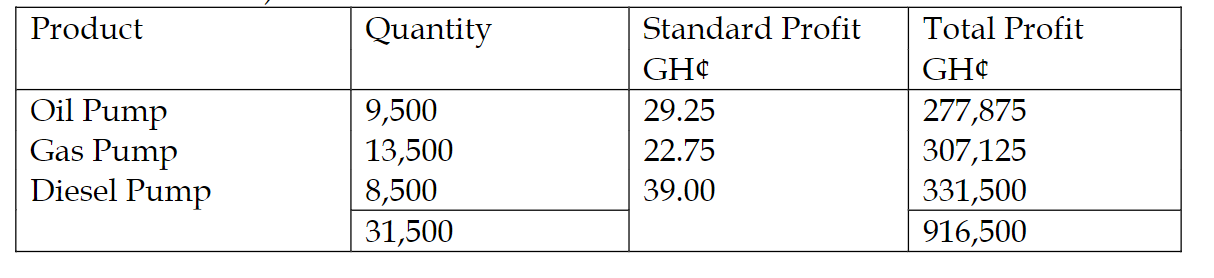

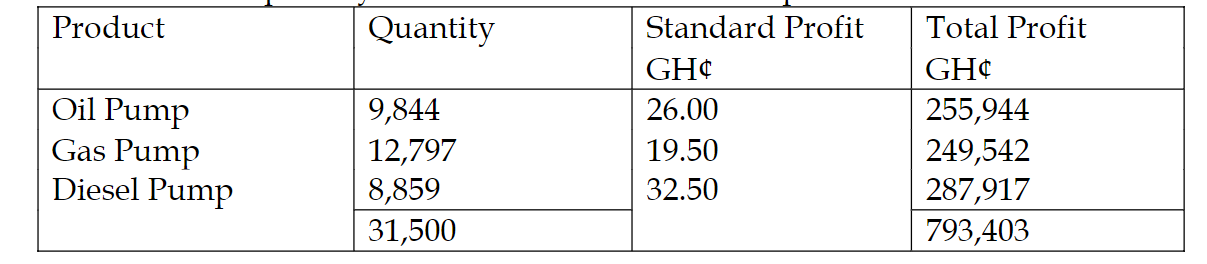

- Actual sales quantity at actual mix at standard profit

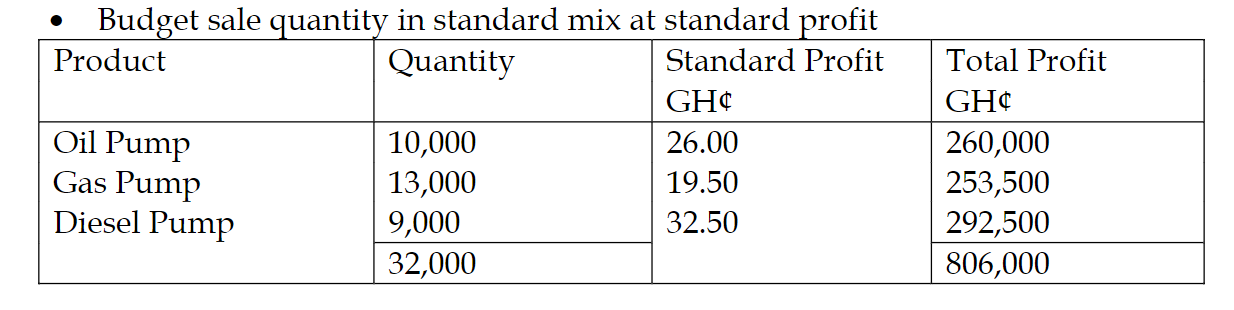

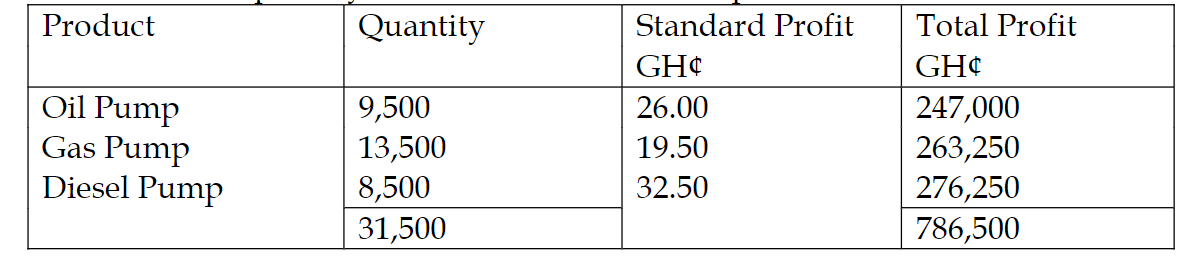

- Actual sales quantity at standard mix at standard profit

Alternative approach to actual sales quantity in standard mix t standard profit

= Actual quantity * average standard profit per unit

=31,500 units* GH¢25.1875 per units = GH¢793,403

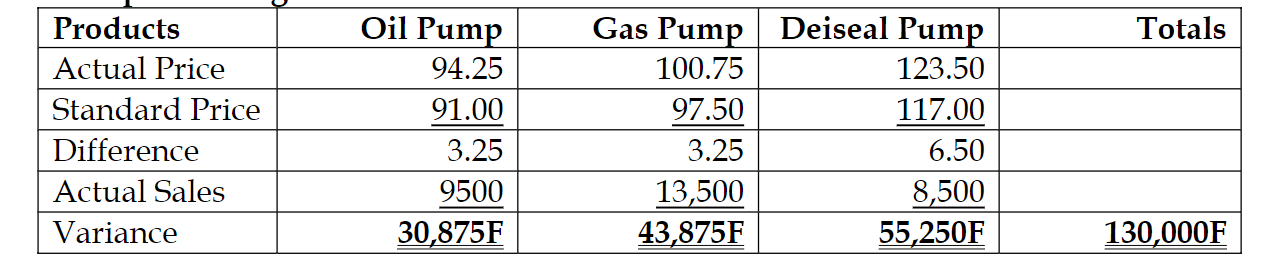

Sales profit margin variance

(2 marks)

Sales mix profit variance

Alternative solution

Sales profit margin variance

iii)Reconciliation statement

(4 marks evenly spread using ticks)