Question

Adu, Boateng, and Dogbe are trading in partnership under an agreement which provides for interest on partners’ capital accounts at the rate of 10% per annum, annual salaries of GHȼ7,500 and GHȼ4,000 for Boateng and Dogbe respectively, and the balance of the profit or loss shared among Adu, Boateng, and Dogbe in the proportion 5:3:2 respectively.

Partners’ cash drawings for the year ended 30 April 2021 were as follows:

| Partner | Amount (GHȼ) |

|---|---|

| Adu | 8,000 |

| Boateng | 5,000 |

| Dogbe | 6,000 |

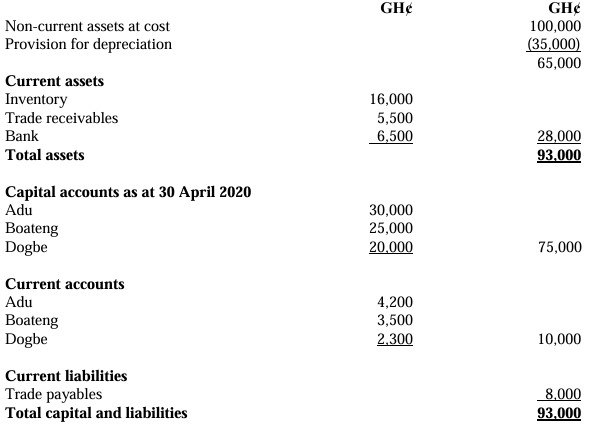

The draft Statement of Financial Position as at 30 April 2021 of Adu, Boateng, and Dogbe is as follows:

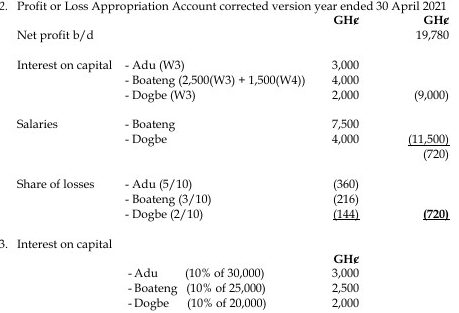

After the preparation of the draft final accounts for the year ended 30 April 2021, which disclosed a net loss of GHȼ10,500, it was discovered that:

- The partners’ cash drawings for the year under review have been debited to purchases.

- On 1 November 2020 it was agreed that Boateng should increase his partnership capital from GHȼ25,000 by transferring to the partnership a freehold property bought by Boateng five years earlier at a cost of GHȼ10,000 and currently valued at GHȼ30,000. Although the appropriate debit entry has been made in the non-current asset account, the corresponding credit entry appeared in the profit and loss appropriation account.

- The partners’ salaries for the year ended 30 April 2021 have been debited to staff salaries and credited to the relevant partners’ current accounts.

The partners have now decided that an allowance for receivables should be 4% of trade receivables.

Required:

a) Compute the revised net profit or loss of the partnership for the year ended 30 April 2021. (5 marks)

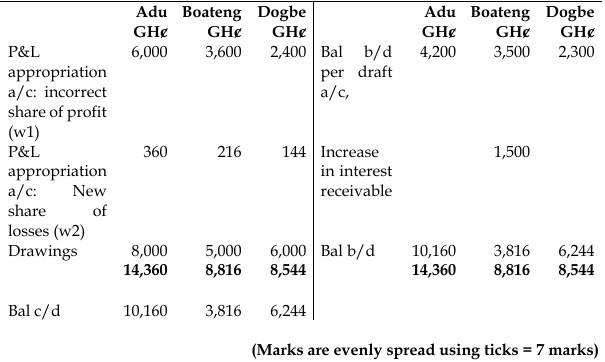

b) Prepare the revised partners’ current accounts for the year ended 30 April 2021. (Note: the partners’ current accounts should commence with the balances shown in the draft partnership Statement of Financial Position as at 30 April 2021). (7 marks)

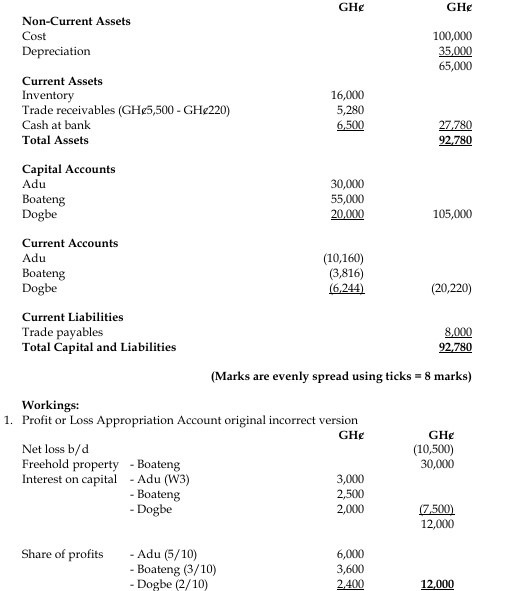

c) Redraft the Statement of Financial Position of the partnership as at 30 April 2021. (8 marks)

Answer

a) Revised Net Profit or Loss Calculation

| Description | Amount (GHȼ) |

|---|---|

| Net loss as per draft accounts | (10,500) |

| Add: Cash drawings wrongly debited to purchases, and so included in the cost of sales in the trading account | 19,000 |

| Adjusted net profit before salaries | 8,500 |

| Add: Partners’ salaries wrongly charged as an expense in the Profit & Loss account (7,500 + 4,000) | 11,500 |

| Net profit before allowance for receivables | 20,000 |

| Less: Increase in the allowance for receivables (4% of GHȼ5,500) | (220) |

| Adjusted net profit for the year | 19,780 |

Total Marks for 2a: 5

b) Revised Partners’ Current Accounts

c) Redrafted Statement of Financial Position as at 30 April 2021

4. Interest on extra capital

Interest on the extra capital should be provided for from 1 November 2020 until 30

April 2021 (6 months)

i.e., 6/12 x 10% x 30,000 = GHȼ1,500