Question

Answer

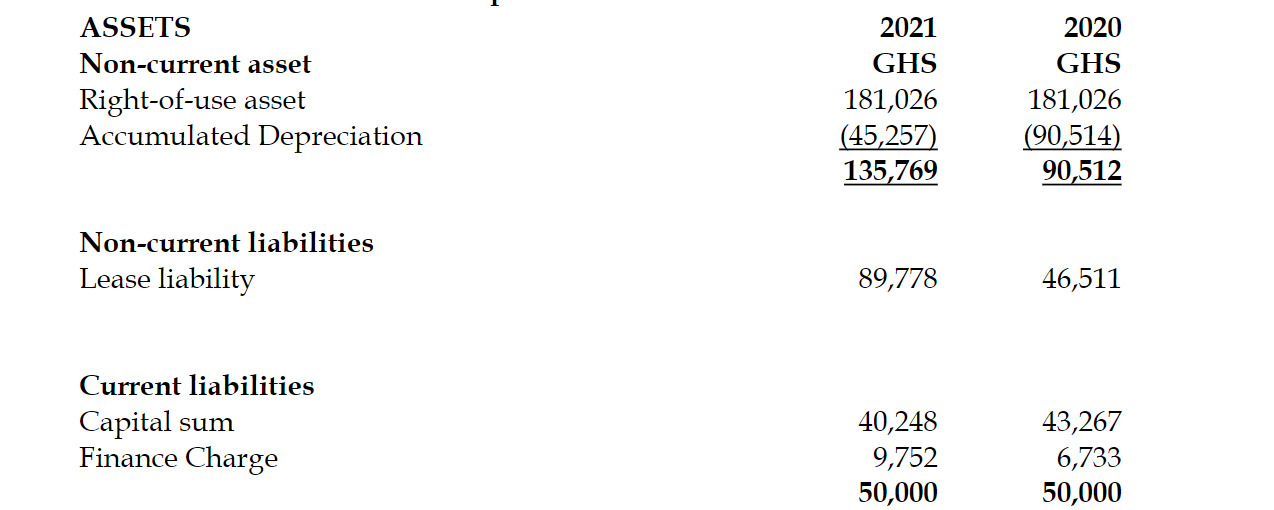

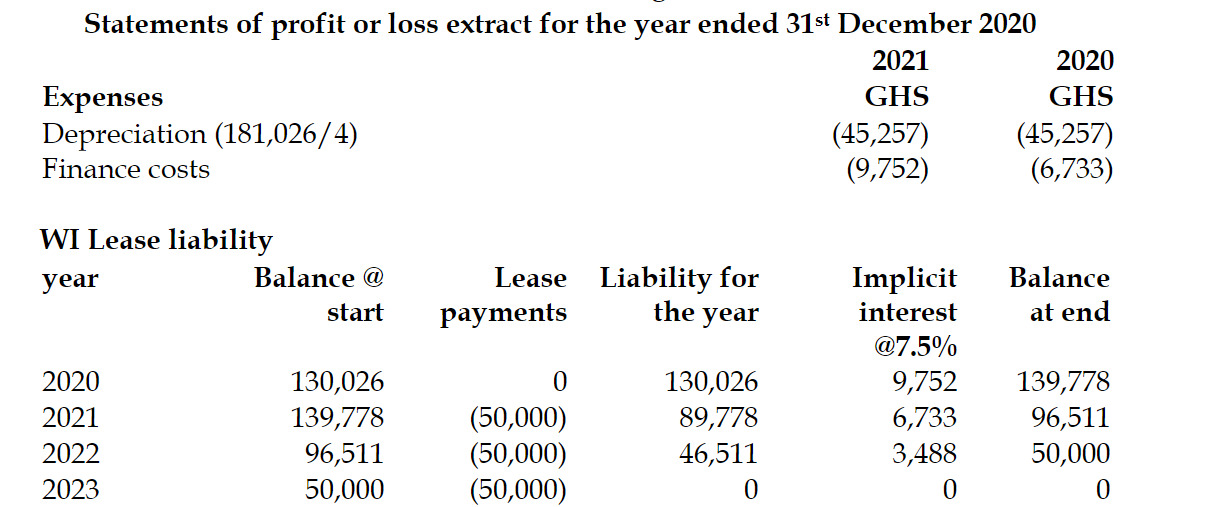

Kundugu Ltd

Statements of financial position extract as at 31st

December 2020

Kundugu Ltd

Annual depreciation = GHS181,026 ÷ 4 years GHS 45,257

Initial recognition of right-of-use asset 1 mark Initial recognition of lease liability 0.5 marks

Lease schedule 1.5 mark

SOFP (Extract) 2 marks

SOPL (Extract) 1 mark