Question

Answer

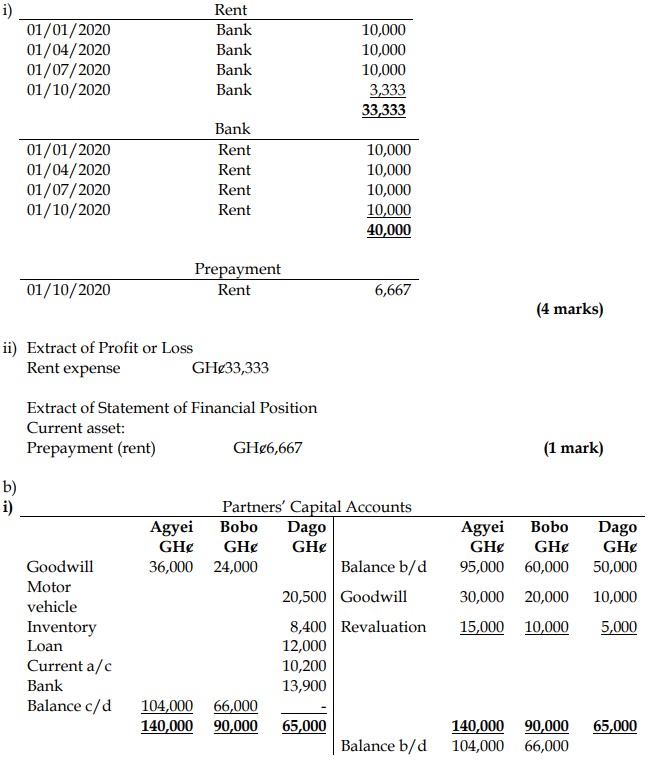

a)

Workings:

1. Revaluation surplus calculation:

GHȼ (116,325 – 80,000) – GHS (5,300 + (25,800 – 5,300) x 5%) = GHȼ30,000

Agyei 30,000 x 3/6 = 15,000

Bobo 30,000 x 2/6 = 10,000

Dago 30,000 x 1/6 = 5,000

2. Goodwill in old ratio:

Agyei 60,000 x 3/6 = 30,000

Bobo 60,000 x 2/6 = 20,000

Dago 60,000 x 1/6 = 10,000

3. Goodwill in new ratio:

Agyei 60,000 x 3/5 = 36,000

Bobo 60,000 x 2/5 = 24,000

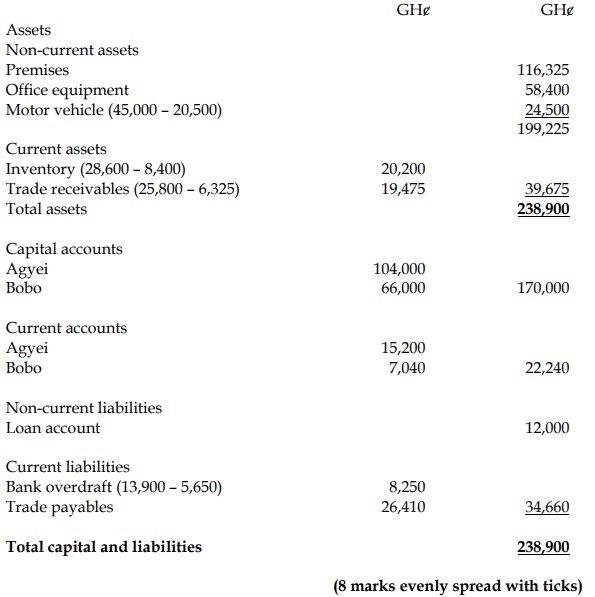

ii) Partnership Statement of Financial Position as at 1 July 2020