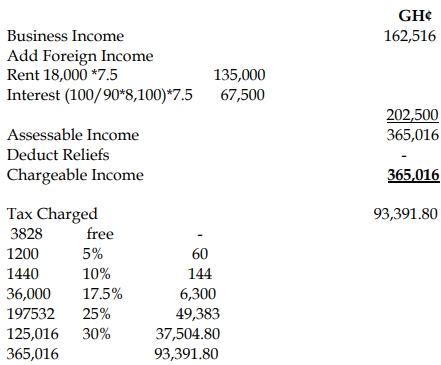

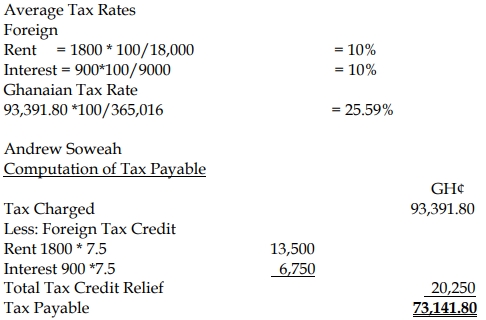

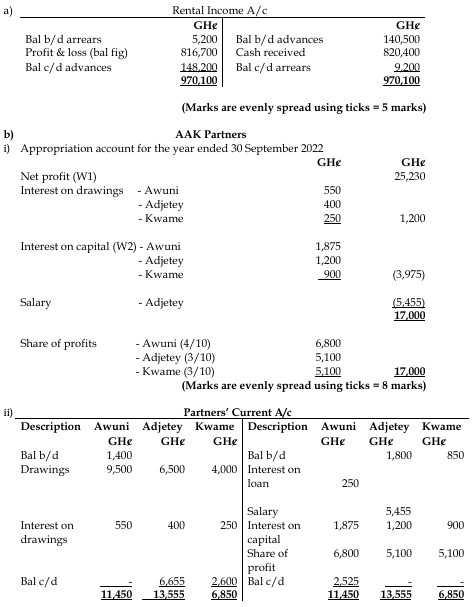

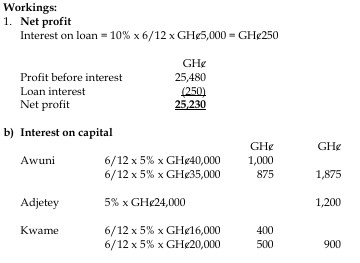

- 10 Marks

Question

A resident person who makes a payment to another resident person in respect of the rental of residential or non-residential premises is required to withhold tax in accordance with the Income Tax Act, 2015 (Act 896) as amended.

Required:

i) State the taxation principle applicable to rental income and the relevant rates. (5 marks)

ii) Given i) above, how will you treat this transaction, where a resident person makes a payment to another resident person conducting a business of sale or renting of residential or non-residential premises?

Answer

i) Taxation Principle for Rental Income and Relevant Rates

- Rental income received by a resident person from another resident person is subject to withholding tax.

- The applicable withholding tax rate for residential premises is 8%, while for non-residential (commercial) premises, the rate is 15%.

- This withholding tax on rental income is treated as a final tax for the recipient, meaning no further tax is charged on the rental income received.

(5 marks)

ii) Treatment of the Transaction for a Business of Sale or Renting of Premises

- When a resident person conducts a business involving the sale or renting of residential or non-residential premises, the payment is treated as a supply of services rather than an investment return.

- In this case, the withholding tax rate is 7.5% on the payment made to the business, and this withholding tax is not final.

- The withheld tax serves as an advance tax, and the recipient (the business) will still be required to account for corporate tax based on their total income.

- Tags: Non-Residential Premises, Rental Income, Residential, Withholding Tax

- Level: Level 2

- Topic: Withholding Tax Administration

- Series: MAY 2021

- Uploader: Theophilus