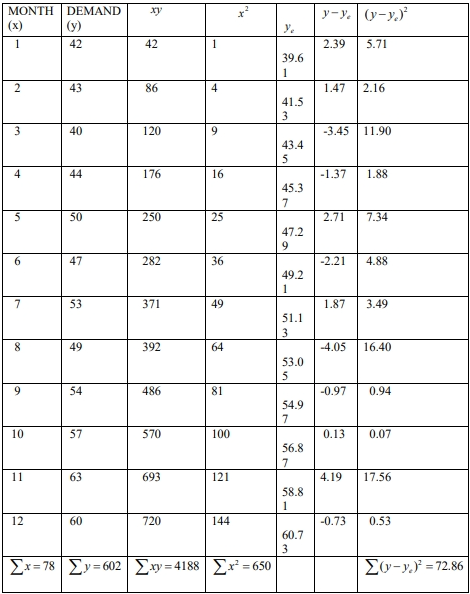

Question

Answer

The regression equation Y=a+bXY = a + bX is calculated as follows:

b =

a =

Thus, the regression equation is:

Y = 29.27 − 0.064X

(i) When X=280X the number of errors is:

Y = 29.27 − 0.064 (280) = 11.35

Therefore, a student studying for 280 minutes would make approximately 11 errors.

(ii) The expected change in the number of errors for a 1-minute change in study time is given by the regression coefficient b=−0.064b

Thus, a 1-minute change in study time is expected to result in a 0.064 fewer errors.

(iii) The formula for the Pearson Product Moment Correlation Coefficient rr is:

r =

Substituting the given values:

r =

Thus, the Pearson Product Moment Correlation Coefficient is -0.9261.

(iv) The coefficient of determination is calculated as:

![]()

The coefficient of determination is 85.77%, which means 85.77% of the variation in the number of errors made can be explained by the study time.