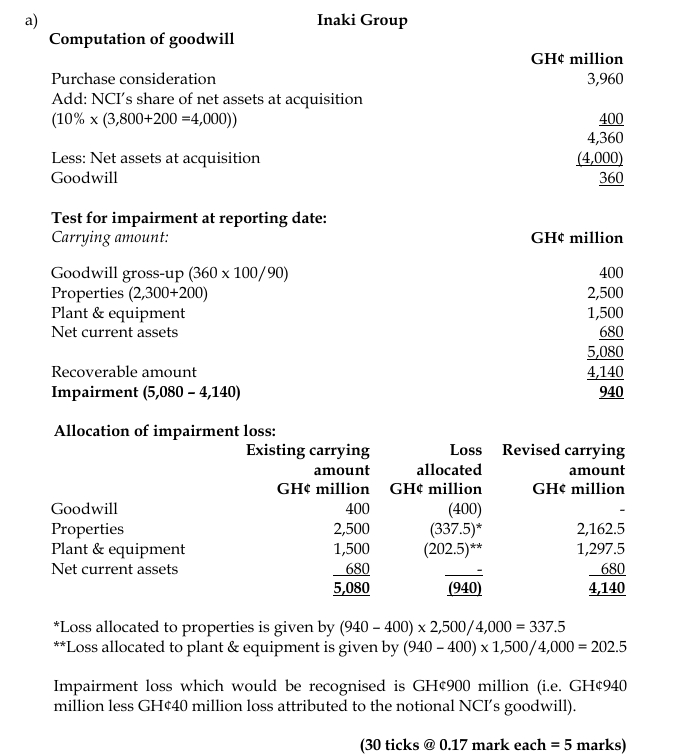

- 5 Marks

Question

Analyze the circumstances under which impairment losses arise and demonstrate the circumstances that may indicate that a company’s assets may have become impaired as per the provisions of IAS 36 – Impairment of Assets.

Answer

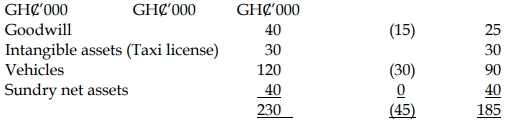

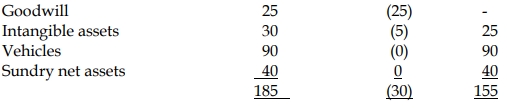

An impairment loss arises where the carrying value of an asset, or group of assets, is higher than their recoverable amounts. In effect the standard requires that assets should not appear in a statement of financial position at a value which is higher than they are worth. The recoverable amount of an asset is defined as the higher of its net realizable value (i.e. the amount at which it can be sold for net of direct selling expenses) or its value in use (i.e. its estimated future net cash flows discounted to a present value). IAS 36 Impairment of Assets recognizes that many assets do not produce independent cash flows and therefore the value in use may have to be calculated for a group of assets – a cash generating unit.

The standard recognizes that it would be too onerous for companies to have to test for impaired assets every year and therefore only requires impairment reviews when there is some indication that impairment has occurred. The exception to this general principle is where an intangible asset has an indefinite useful or is not yet available for use, in which case an impairment review is required at least annually. This also applies to goodwill acquired in a business combination. Impairments generally arise where there has been an event or change in circumstances. It may be that something has happened to the assets themselves (e.g. physical damage) or there has been a change in the economic environment relating to the assets.

Indicators of Impairment which may be available from internal or external sources:

o Poor operating results – this could be a current operating loss or a low profit. One year’s losses in itself does not necessarily mean there has been an impairment, but if this is coupled with previous losses or expected future losses then there is an indication of impairment.

o A significant decline in an asset’s market value (in excess of normal depreciation through use or the passage of time) or evidence of obsolescence (through market changes or technology) or physical damage.

o Evidence of a reduction in the useful economic life or the estimated residual value of assets.

o Adverse changes in the market or economy such as the entrance of a major competitor, new statutory or regulatory rules or any indicator of value that has been used to value an asset.

o A commitment to a significant reorganization or restructuring of the business.

o Loss of key employees or major customers.

o Increases in long-term interest rates which could materially impact on value in use calculations thus affecting the recoverable amounts of assets.

o Where the carrying amount of an entity’s net assets is more than its market capitalization.

- Tags: Carrying Value, IAS 36, Impairment, Indicators of Impairment, Recoverable Amount

- Level: Level 3

- Topic: IAS 36: Impairment of assets

- Series: MAY 2016

- Uploader: Theophilus