Question

Answer

a) NPV and IRR of Project-05

NPV of Project-05:

| Period | NCF (GH¢m) | DF @ 25% | PV @ 25% | DF @ 35% | PV @ 35% |

|---|---|---|---|---|---|

| EOY 0 | -34 | 1.0000 | (34.00) | 1.0000 | (34.00) |

| EOY 1-5 | 13.5 | 2.6893 | 36.31 | 2.2200 | 29.97 |

| EOY 5 | 10 | 0.3277 | 3.28 | 0.2230 | 2.23 |

| Total | NPV | 5.58 | (1.80) |

IRR of Project-05:

Project-05 should be considered for further appraisal as its NPV is positive and IRR is greater than the required rate of return.

(Marks allocation: NPV computation = 6 marks; IRR computation = 4 marks)

b) Sensitivity of Project-05 to Cost of Plant and Equipment:

Interpretation:

The cost of the plant and equipment will have to increase by 16.41% for the NPV of the project to become zero. This implies that the project will no longer be viable if the cost of equipment and plant increases by more than 16.41%.

(Marks allocation: Sensitivity calculation = 4 marks; Interpretation = 1 mark)

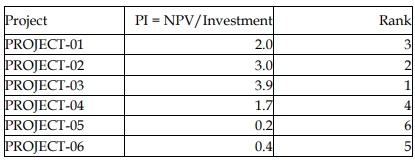

c) Recommended Portfolio of Projects:

Profitability Index (PI) of Projects

Allocating available funds to projects based on PI ranking:

| Rank | Project | Investment Required | Allocation | NPV |

|---|---|---|---|---|

| 1 | PROJECT-03 | 9 | 9 | 35 |

| 2 | PROJECT-02 | 15 | 15 | 45 |

| 3 | PROJECT-01 | 25 | 25 | 50 |

| 4 | PROJECT-04 | 12 | 12 | 20 |

| 5 | PROJECT-06 | 5 | 1 | 0.4 |

| 6 | PROJECT-05 | 34 | 0 | 0 |

Recommended Portfolio:

The company should fund Projects 3, 2, 1, and 4 in full and fund 1/5 of Project 6 for a combined NPV of GH¢150.4 million.

(Marks allocation: Profitability index and ranking = 3 marks; Recommended portfolio = 2 marks)