Question

Answer

Throughput Accounting Ratio (TPAR) is a relative measure that shows how many times the throughput per limited resource can cover the factory cost per limited resource. The formula for TPAR is:

TPAR=![]()

Calculation:

- Factory cost per bottleneck resource:

Factory cost per bottleneck=

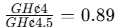

- TPAR for Product A: TPAR=

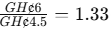

- TPAR for Product B: TPAR=

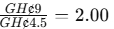

- TPAR for Product C: TPAR=

Comment:

- Product A: TPAR is less than 1 (0.89), indicating that Product A is not profitable as its throughput cannot cover the factory cost per bottleneck resource.

- Product B: TPAR is greater than 1 (1.33), suggesting that Product B is profitable.

- Product C: TPAR is the highest (2.00), indicating that Product C is the most profitable among the three products.