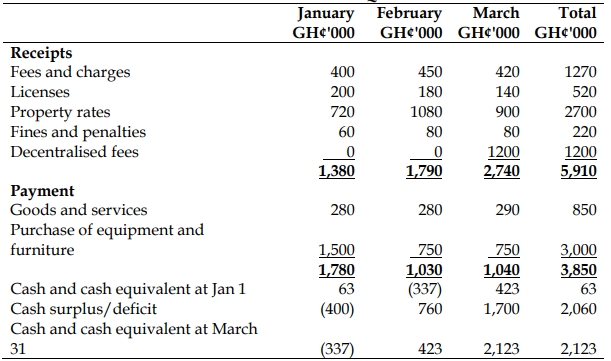

Question

Answer

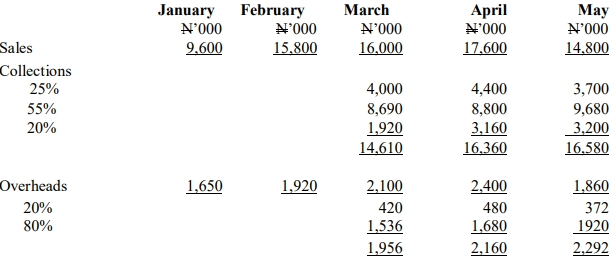

WHYME LIMITED

CASH BUDGET FOR THREE MONTHS ENDING MAY YEAR XXX

| March (N’000) | April (N’000) | May (N’000) | |

|---|---|---|---|

| INFLOWS | |||

| Sales Collections | 14,610 | 16,360 | 16,580 |

| Loan | 10,000 | – | – |

| Fixed Asset Disposal | – | 1,500 | – |

| Investment Income | – | 50 | 50 |

| Total Inflows (A) | 24,610 | 17,910 | 16,630 |

| OUTFLOWS | |||

| Purchases | 12,000 | 10,000 | 11,000 |

| Salaries | 1,670 | 1,700 | 1,750 |

| Salaries Deductions | 82 | 90 | 89 |

| Overheads | 1,956 | 2,160 | 2,292 |

| Fixed Assets | 12,000 | – | – |

| Loan Repayment | – | 2,500 | 2,500 |

| Investment | 2,500 | – | – |

| Total Outflows (B) | 30,208 | 16,450 | 17,631 |

| Balance B/F | 6,500 | 902 | 2,362 |

| Net Cash Flow (A – B) | (5,598) | 1,460 | 1,001 |

| Balance C/F | 902 | 2,362 | 1,36 |

Workings