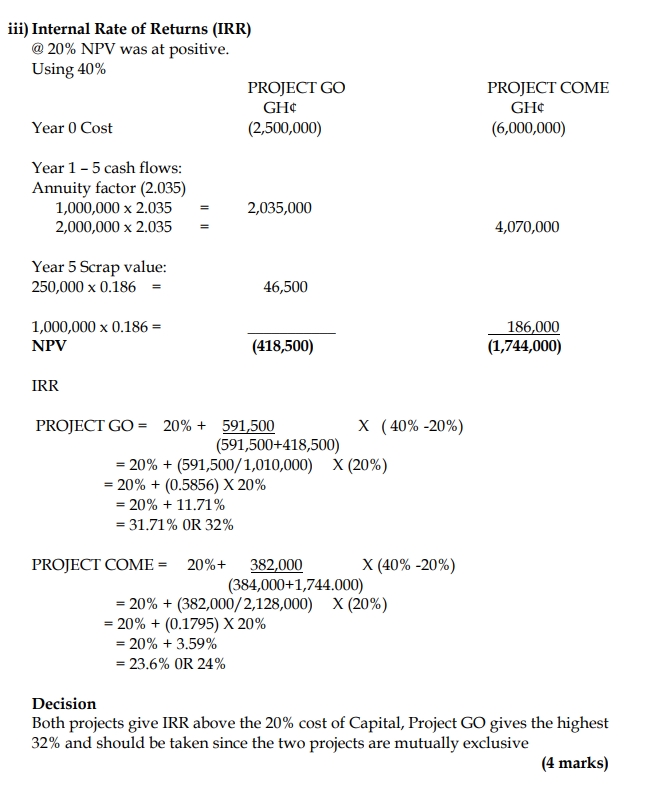

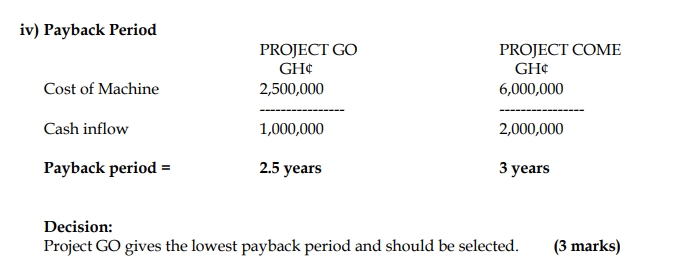

a) Advantages and Disadvantages of Payback Method

Advantages:

- Simplicity: The payback method is easy to calculate and understand, making it accessible to managers without extensive financial expertise.

- Liquidity Focus: It provides a quick estimate of the liquidity risk by showing how quickly an investment can recover its initial cost.

Disadvantages:

- Ignores Time Value of Money: The method does not account for the time value of money, meaning future cash flows are treated as equally valuable as immediate ones.

- Ignores Cash Flows After Payback: It only considers the period until the initial investment is recovered and disregards any cash flows that occur after the payback period.

b) NPV Calculation for DÉCOR Ltd’s Proposed Investment

Revenue Calculations:

| Year |

1 |

2 |

3 |

4 |

| Units Sold |

70,000 |

106,000 |

150,000 |

72,000 |

| Selling Price (GH¢) |

30 |

31.5 |

33.08 |

34.73 |

| Sales Revenue (GH¢) |

2,100,000 |

3,339,000 |

4,962,000 |

2,500,560 |

Variable Costs Calculations:

| Year |

1 |

2 |

3 |

4 |

| Units Sold |

70,000 |

106,000 |

150,000 |

72,000 |

| Variable Cost (GH¢) |

18 |

19.08 |

20.22 |

21.44 |

| Total Variable Costs (GH¢) |

1,260,000 |

2,022,480 |

3,033,000 |

1,543,680 |

Net Cash Flow Calculations:

| Year |

0 |

1 |

2 |

3 |

4 |

| Sales Revenue (GH¢) |

– |

2,100,000 |

3,339,000 |

4,962,000 |

2,500,560 |

| Variable Costs (GH¢) |

– |

(1,260,000) |

(2,022,480) |

(3,033,000) |

(1,543,680) |

| Fixed Costs (GH¢) |

– |

– |

– |

– |

– |

| Contribution (GH¢) |

– |

840,000 |

1,316,520 |

1,929,000 |

956,880 |

| Capital Allowance (GH¢) |

(2,000,000) |

500,000 |

500,000 |

500,000 |

500,000 |

| Taxable Profit (GH¢) |

– |

340,000 |

816,520 |

1,429,000 |

456,880 |

| Tax @ 25% (GH¢) |

– |

(85,000) |

(204,130) |

(357,250) |

(114,220) |

| Net Profit After Tax (GH¢) |

– |

255,000 |

612,390 |

1,071,750 |

342,660 |

| Add: Capital Allowance (GH¢) |

– |

500,000 |

500,000 |

500,000 |

500,000 |

| Net Cash Flows (GH¢) |

(2,000,000) |

755,000 |

1,112,390 |

1,571,750 |

842,660 |

| Working Capital Requirement (GH¢) |

(210,000) |

(123,900) |

(162,300) |

246,144 |

250,056 |

| Net Cash Flow After WC (GH¢) |

(2,210,000) |

631,100 |

950,090 |

1,817,894 |

1,092,716 |

| Discount Factor @ 15% |

1.000 |

0.8696 |

0.7561 |

0.6575 |

0.5718 |

| Present Value (GH¢) |

(2,210,000) |

548,805 |

718,363 |

1,195,265 |

624,815 |

Net Present Value (NPV): GH¢877,248

Decision: The project should be undertaken since the NPV is positive, indicating an addition to shareholder value.

c) Currency Risk Analysis

i) Foreign Exchange Loss to the Ghanaian Buyer: The original expectation was to pay:

US$280,000×GH¢4.2=GH¢1,176,000

However, the payment after the exchange rate change was:

US$280,000×GH¢4.6=GH¢1,288,000

Foreign Exchange Loss = GH¢112,000

ii) Currency Risk Explanation: Currency risk arises from exposure to the consequences of a rise or fall in an exchange rate. Here, the Ghanaian buyer was exposed to the risk of a fall in the value of the cedi, leading to a higher payment in cedi terms.

iii) Transaction Risk Explanation: Transaction risk occurs when a financial transaction is settled at a future date, exposing the company to potential exchange rate fluctuations. Here, the risk lasted from when the goods were sold on credit until the time of payment.

iv) Effect on Company’s Trading Profits: Trading profits can be significantly affected by currency movements. In this case, the foreign exchange loss of GH¢112,000 reduces the company’s profit, highlighting the impact of exchange rate volatility on financial performance.