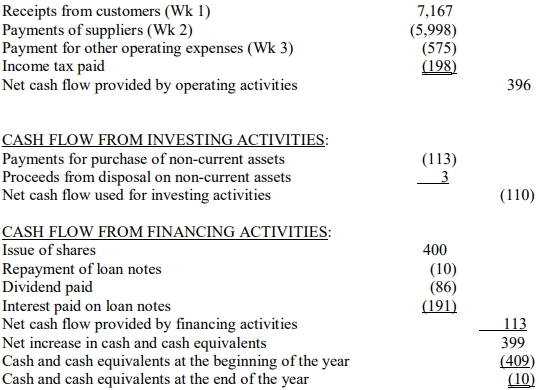

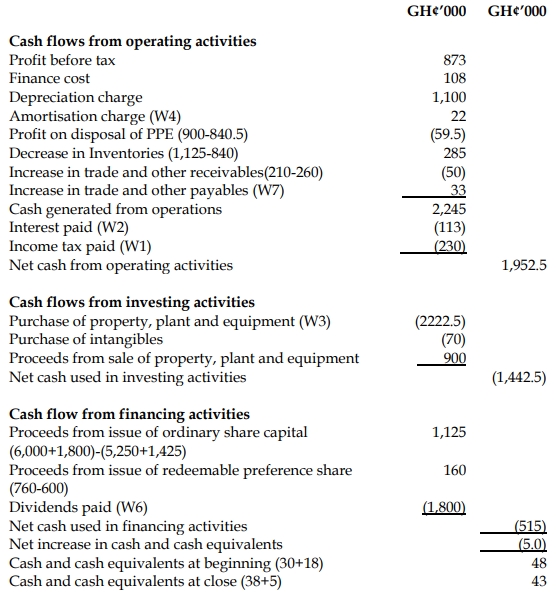

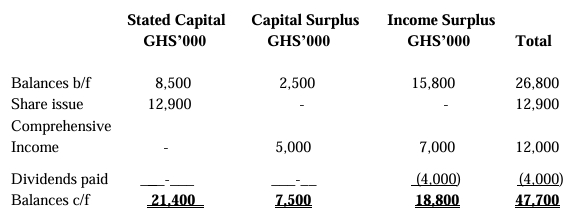

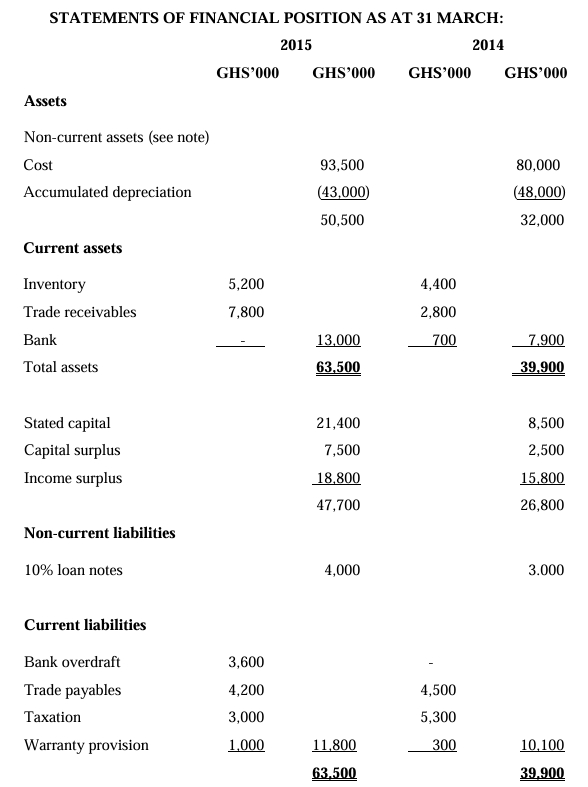

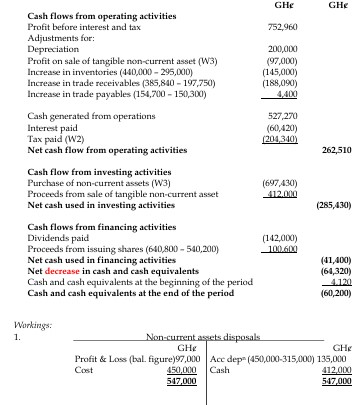

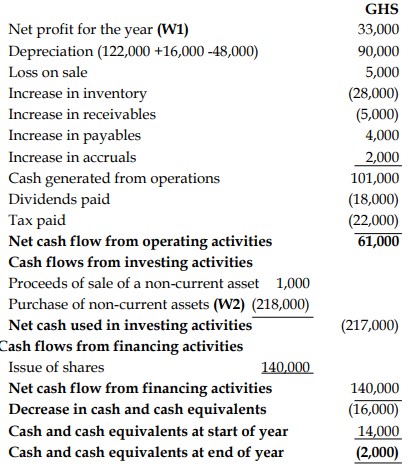

| Cash flows from operating activities |

|

| Profit before tax |

10,200 |

| Depreciation (W2) |

6,000 |

| Loss on disposal of displays (W3) |

1,500 |

| Interest expense |

600 |

| Operating cash flow before working capital changes |

18,300 |

| Increase in warranty provision (1,000 – 300) |

700 |

| Increase in inventories (5,200 – 4,400) |

(800) |

| Increase in receivables (7,800 – 2,800) |

(5,000) |

| Decrease in trade payables (4,500 – 4,200) |

(300) |

| Cash generated from operations |

12,900 |

| Interest paid |

(600) |

| Income tax paid (W4) |

(5,500) |

| Net cash from operating activities |

6,800 |

| Cash flows from investing activities |

|

| Purchase of property, plant, and equipment (W1) |

(20,500) |

| Cost of disposal of property, plant, and equipment |

(500) |

| Net cash used in investing activities |

(21,000) |

| Cash flows from financing activities |

|

| Share issue |

12,900 |

| Loan note issue (4,000 – 3,000) |

1,000 |

| Dividends paid |

(4,000) |

| Net cash from financing activities |

9,900 |

| Net decrease in cash and cash equivalents |

(4,300) |

| Cash and cash equivalents at beginning of period |

700 |

| Cash and cash equivalents at end of period |

(3,600) |