Question

Answer

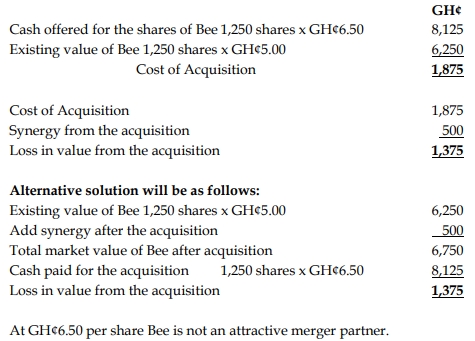

Since the net loss from the acquisition is GH¢1,375, Ape should not proceed with the merger as it results in a financial loss despite the synergy benefits.

Ape has 2,500 shares outstanding at GH¢10 per share. Bee has 1,250 shares outstanding at GH¢5 per share. Ape estimates that the value of synergistic benefit from acquiring Bee is GH¢500. Bee has indicated that it would accept a cash purchase offer of GH¢6.50 per share.

Required:

Identify whether Ape should proceed with the merger

Since the net loss from the acquisition is GH¢1,375, Ape should not proceed with the merger as it results in a financial loss despite the synergy benefits.

Despite substantial evidence, drawn from different countries and different time periods, that suggests the wealth of shareholders in a bidding company is unlikely to be increased as a result of taking over another company, takeovers remain an important part of the business landscape.

Required:

i) Explain briefly when a takeover will make economic and financial sense.

(3 marks)

ii) Discuss briefly FIVE (5) reasons why a takeover may fail to deliver an expected increase in wealth for the bidding company’s shareholders.

(5 marks)

i) When a takeover makes economic and financial sense

A takeover makes economic and financial sense when it creates value through synergies. The value of the combined business must exceed the sum of the values of the individual businesses. This can be expressed as:

PV Combined business > PV Bidding business + PV Target business

This means that the takeover should generate benefits such as cost savings, revenue enhancement, or improved efficiency, which would not have been realized if the companies operated independently. The combined entity should deliver a higher net present value (NPV) or enhanced future cash flows, justifying the merger or acquisition.

(3 marks)

ii) Five reasons why a takeover may fail to deliver the expected increase in wealth for the bidding company’s shareholders

b) As a Finance Manager in your company, you have been asked to produce an explanatory memo to Senior Management on the subject of Mergers and Acquisitions. Your memo should clearly outline what actions a target company might take to prevent a hostile takeover bid.

(5 marks)

Memo: Hostile Takeover Defense Strategies

To: Senior Management

From: Finance Manager

Subject: Actions to Prevent a Hostile Takeover Bid

In response to concerns regarding the possibility of a hostile takeover, there are several strategies that a target company can adopt to defend against such attempts. Below are five key actions:

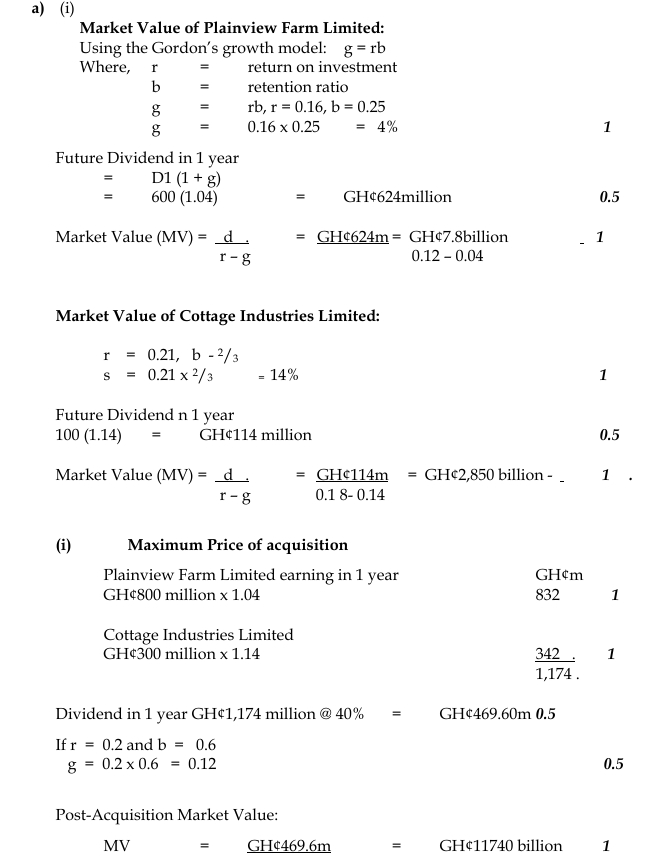

a) Plainview Farms Limited is considering acquiring Cottage Industries Limited. The extracts of the financial statements of the two companies are as follows:

Statement of Financial Position

| Plainview Farms Ltd (GH¢’m) | Cottage Industries Ltd (GH¢’m) | |

|---|---|---|

| Net Assets | 6,300 | 1,892 |

| Equity Capital | 2,000 | 1,000 |

| Income Surplus | 4,300 | 892 |

Income Statement

| Plainview Farms Ltd (GH¢’m) | Cottage Industries Ltd (GH¢’m) | |

|---|---|---|

| Profit after tax | 800 | 300 |

| Dividend | (600) | (100) |

| Retained earnings | 200 | 200 |

The two companies retain the same proportion of profits each year, and this is expected to continue in the future. Plainview Farms Limited’s return on investment is 16%, while Cottage Industries Limited’s is 21%. One year after the post-acquisition period, Plainview Farms will retain 60% of its earnings and expects to earn a return of 20% on new investment.

The dividends of both companies have been paid. The required rate of return for ordinary shareholders of Plainview Farms Limited is 12%, and for Cottage Industries Limited it is 18%. After the acquisition, the required rate of return will become 16%.

Required:

i) Calculate the pre-acquisition market values of both companies. (5 marks)

ii) Calculate the maximum price Plainview Farms Limited will pay for Cottage Industries Limited. (5 marks)

Expansion by organic growth or by acquisition should only be undertaken if it leads to an increase in the wealth of the shareholders.

Required:

i) Discuss TWO strategic issues that arise from pursuing growth through mergers and acquisitions. (4 marks)

ii) Discuss TWO strategic issues that arise from pursuing growth through organic growth. (4 marks)

There has been a merger among three companies: Ann Ltd, Bab Ltd, and Cee Ltd. The merger was geared towards creating a monopoly in the market. After careful revaluation of the assets and liabilities of the companies, the following is the outlook:

The following is the outlook of the new company after the merger:

Required:

As an intern of IKERN and Associates, write a memo to your partner on the company’s tax exposure after the merger.

Memo

To: Partner

From: Tax Intern

Date: 16 February 2021

Subject: Tax Exposure After the Merger

Introduction:

Following our discussion on the above subject matter, I furnish the following for your consideration.

Issues:

The gains on the realisation of an asset accruing to or derived by a company arising out of a merger, amalgamation, or reorganisation of a company are exempt from tax when there is continuity of at least fifty percent of the underlying ownership in the asset.

Tax Implication:

The merger of the three companies and the gains arising from the revaluations shall be assessed based on the underlying ownership in the new entity. If the underlying ownership in the new entity is less than 50%, the gains will be subject to tax at the corporate rate of 25%. If ownership is maintained at or above 50%, the gains are exempt from tax.

From the above gains, if the underlying ownership in the new company post-merger is less than 50%, the gains shall be taxed at the marginal rate of 25%. If the ownership is maintained at 50% or more, the gains will be exempt from tax.

The profit being made by the new company indicates the success of the merger, and it shall be taxed at the corporate tax rate of 25%.

Conclusion:

I hope the above helps you in your further action on the matter.

Yours faithfully,

Handsome Padii.

Farmer Ltd is a non-resident company based in the USA. Farmer Ltd has succeeded over the years in acquiring and selling companies in distress alongside its primary objectives of buying and selling cosmetics. In the 2020 year of assessment, it decided to announce its presence in Ghana by acquiring Bugum Ltd, a resident company. Bugum Ltd has had financial setbacks in its fortunes over the last couple of years and became vulnerable to predators.

Required:

Advise the management of Farmer Ltd, what the tax implications are if Farmer Ltd acquires more than 50% of the underlying ownership of Bugum Ltd.

Mergers and acquisitions have blessings for the predator(s) and may equally bring losses to the predator. Therefore, under section 62 of Act 896 (Act 2015), the following shall not be benefitted by the new owners, that is, Farmer Ltd in this case:

The management of Akolo Ltd (Akolo) has been running this business entity for some time now. At a seminar organized for some select businesses at the Trade Fair-Accra last year, the management of Abolo Ltd (Abolo) realized at the seminar that the two companies (Akolo and Abolo) have a lot in common with the same market share. Consequently, the two companies commenced processes to merge as one strong entity. The two agreed on a merger arrangement to benefit from the synergetic efforts.

The two companies intend to form a new entity called Akobolo Ltd (Akobolo).

Required:

i) What is the tax implication of the arrangement if, in the new company-(Akobolo), Akolo intends to hold 40% in the underlying ownership in the assets of the new company while Abolo holds 60%? (3 marks)

ii) What is the tax implication if both companies hold 50% each in the underlying ownership of the assets of the new company – Akobolo? (2 marks)

i) – Tax Implication of 40% and 60% Ownership:

Under section 47 of Act 2015 (Act 896), the gains on the realization of an asset accruing to or derived by a company arising out of a merger, amalgamation, or reorganization of a company is exempt from tax where there is a continuity of at least fifty percent of the underlying ownership in the asset.

In this arrangement, Akolo has 40% in the underlying ownership in the asset of the new company, which suggests the realization of the assets and consequently, any gains made are subject to tax by adding it to business income and subjecting it to applicable tax rates.

In the case of Abolo, which intends to hold 60% in the underlying ownership in the assets of the new company, any gain from this merger is exempt from tax.

(3 marks)

ii) – Tax Implication of 50% and 50% Ownership:

If both companies hold 50% each in the underlying ownership of the assets of the new company, this constitutes a realization of assets, but the gains on this realization are exempt from tax in both Akolo Ltd and Abolo Ltd.

(2 marks)

Lekker Inc (Lekker) is a film company located in South Africa. The company is planning to expand into other African countries. The research department of Lekker recommends Ghana as a good location for establishing a subsidiary due to its abundant talent and political stability. However, the company is unsure whether to establish a completely new subsidiary or acquire an existing film company in Ghana. You have been engaged as a consultant to guide Lekker in taking this decision.

Your preliminary assessment revealed the following:

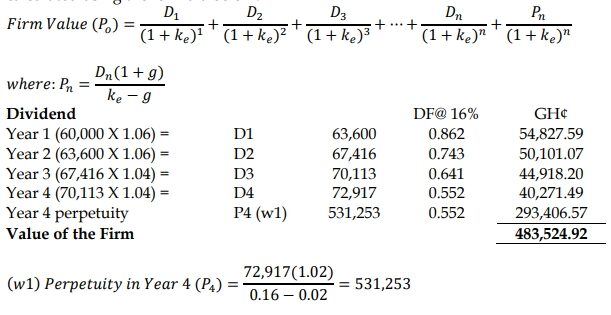

i) You have identified a Ghanaian filmmaker who owns a fast-growing film company called Akwaaba Films (Akwaaba). You observed that the Ghanaian filmmaker is likely to sell Akwaaba if Lekker could pay GH¢450,000 as purchase consideration. Akwaaba is entirely self-financed, with the owner receiving all profits as dividends. You forecast that Akwaaba’s profit after tax will grow at a rate of 6% per year for the first two years, 4% per year for the next two years, and thereafter, grow at a constant rate of 2% per year in perpetuity. The financial information extracted from Akwaaba shows the following:

| Description | GH¢ |

|---|---|

| Revenue | 250,000 |

| Operating Cost | (140,000) |

| Administrative cost | (30,000) |

| Profit before tax | 80,000 |

| Tax @ 25% | (20,000) |

| Profit after tax | 60,000 |

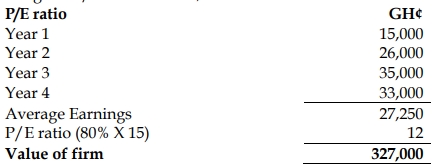

ii) If Lekker decides to set up the subsidiary in Ghana by itself with the same GH¢450,000 purchase consideration for Akwaaba, its after-tax cash flows will be as follows:

| Year | Cash Flow (GH¢) |

|---|---|

| Year 1 | 15,000 |

| Year 2 | 26,000 |

| Year 3 | 35,000 |

| Year 4 | 33,000 |

The overall Price/Earnings (P/E) ratio for the film industry in Ghana is 15 times. The average cash flow risk for unquoted companies in Ghana is 20%. Lekker does not intend to list on the Ghana Stock Exchange.

iii) Lekker’s cost of capital is 16%.

Required:

a) Enumerate THREE (3) advantages of expansion through acquisition over organic expansion to the owners of Lekker. (6 marks)

b) Compute the value of Akwaaba using the dividend valuation method and advise Lekker whether it should acquire Akwaaba at the purchase consideration of GH¢450,000. (8 marks)

c) Using the P/E ratio method, estimate the expected value of Lekker’s subsidiary in Ghana without the acquisition. (4 marks)

d) State TWO (2) reasons mergers and acquisitions may fail to achieve the expected outcomes. (2 marks)

a) Three Advantages of Expansion Through Acquisition Over Organic Expansion:

(6 marks)

b) Value of Akwaaba Using the Dividend Valuation Model:

The Dividend Valuation Model (DVM) can be used to value Akwaaba based on its expected future profits:

Note that the perpetuity is calculated from Year 4 onwards, therefor the discount

factor is the same as that of Year 4 and not Year 5

Conclusion: the purchase consideration of GH¢450,000 quoted by the Ghanaian

filmmaker is lower than the value of the firm, leading to a net gain of 33,524.92.

Based on this Lekker Inc. should purchase Akwaaba Inc

c) Expected Value of Lekker’s Subsidiary Using the P/E Ratio Method:

d) Two Reasons Mergers and Acquisitions May Fail to Achieve Expected Outcomes:

(2 marks)

Amanfi Ltd manufactures cooking oil for the local markets in Ghana. The management of Amanfi Ltd believes that by merging with one of their input suppliers, Aseebu Ltd, the company will be able to control supply, thus giving the Amanfi Group a low-price advantage in the market. Aseebu Ltd is a key supplier of inputs to companies in the cooking oil industry. The financial statements of the two companies are shown below:

Income Statement for the past Five Years (Amanfi Ltd)

| Year (Million GH¢) | 2018 | 2019 | 2020 | 2021 | 2022 (current year) |

|---|---|---|---|---|---|

| Sales | 3,720 | 4,092 | 4,500 | 4,950 | 5,442 |

| Cost of Sales | (1,674) | (1,841) | (2,025) | (2,228) | (2,449) |

| Operating Profit | 2,046 | 2,251 | 2,475 | 2,722 | 2,993 |

| Finance Cost | (252) | (278) | (305) | (336) | (369) |

| Earnings Before Tax | 1,794 | 1,973 | 2,170 | 2,386 | 2,624 |

| Tax @ 30% | (538) | (592) | (651) | (716) | (787) |

| Earnings After Tax | 1,256 | 1,381 | 1,519 | 1,670 | 1,837 |

Income Statement for the past Five Years (Aseebu Ltd)

| Year (Million GH¢) | 2018 | 2019 | 2020 | 2021 | 2022 (current year) |

|---|---|---|---|---|---|

| Sales | 1,860 | 2,046 | 2,250 | 2,475 | 2,496 |

| Cost of Sales | (837) | (921) | (1,013) | (1,114) | (1,123) |

| Operating Profit | 1,023 | 1,125 | 1,237 | 1,361 | 1,373 |

| Finance Cost | (126) | (139) | (153) | (168) | (169) |

| Earnings Before Tax | 897 | 986 | 1,084 | 1,193 | 1,204 |

| Tax @ 30% | (269) | (296) | (325) | (358) | (361) |

| Earnings After Tax | 628 | 690 | 759 | 835 | 843 |

Additional Information:

Amanfi Ltd and Aseebu Ltd have beta of 1.6 and 1.1 respectively. The government treasury bill rate pays a yield of 8% and risk premium on the market is 17%. If the merger goes through, the combined company’s earnings after tax will grow at the same rate as Amanfi Ltd. The merger will lead to annual cost savings of GH¢850 million in perpetuity.

Required:

a) As a Finance Manager, calculate the value of the combined business based on the present value of expected earnings. (8 marks)

b) What is the maximum amount that Amanfi Ltd should pay for Aseebu Ltd? (4 marks)

c) What is the minimum bid that Aseebu Ltd shareholders should be prepared to accept? (4 marks)

d) Calculate the gain/loss from the merger. (2 marks)

e) Identify and explain the type of merger between Amanfi Ltd and Aseebu Ltd. (2 marks)

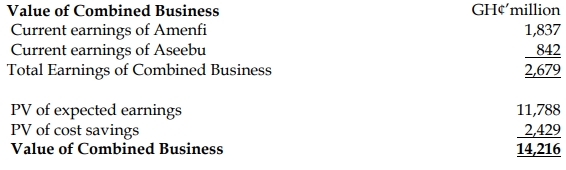

a) Calculation of the Value of the Combined Business Based on the Present Value of Expected Earnings

Value of Combined Business (GH¢’million):

(1 mark for each line up to 5, 1 mark each for the growth rate and 2 marks for cost of equity = 8 marks)

(1 mark for each line up to 5, 1 mark each for the growth rate and 2 marks for cost of equity = 8 marks)

b) Maximum Amount that Amanfi Ltd Should Pay for Aseebu Ltd

Value of Amanfi =  = GH¢8,081 million

= GH¢8,081 million

(2 marks each for the maximum price and the value of Amanfi = 4 marks)

c) Minimum Bid that Aseebu Ltd Shareholders Should Be Prepared to Accept

(2 marks for the minimum price and 1 mark each for the growth rate and the cost of equity = 4 marks)

d) Gain/Loss from the Merger

Gain:

Value of Combined business − (Value of Amanfi + Value of Aseebu)

=14,216 − (8,081 + 4,672) = GH¢1,463 million

e) Type of Merger Between Amanfi Ltd and Aseebu Ltd

Backward Vertical Merger/Acquisition:

A merger between firms that operate at different stages of the same production chain, or between firms that produce complementary goods. This type of vertical merger between a supplier and a firm is known as a backward merger. (2 marks)

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.