Question

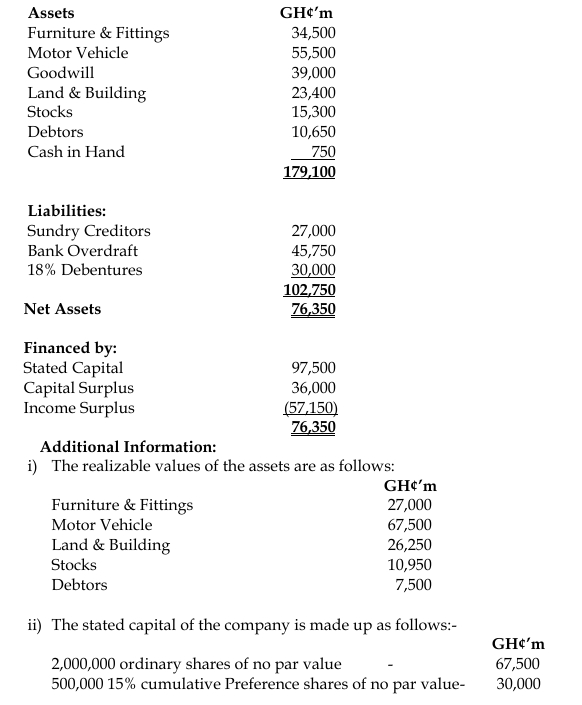

Additional Information:

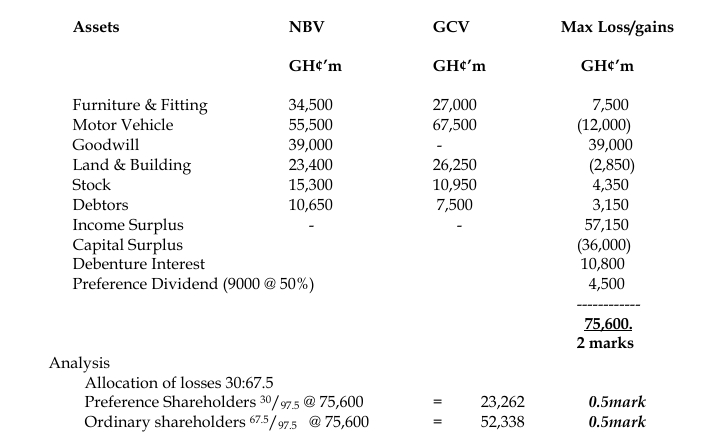

- The realizable values of the assets are as follows:

- Furniture & Fittings: GH¢27.0m

- Motor Vehicle: GH¢67.5m

- Land & Building: GH¢26.25m

- Stocks: GH¢10.95m

- Debtors: GH¢7.5m

- The stated capital of the company is made up as follows:

- 2,000,000 ordinary shares of no par value: GH¢67.5m

- 500,000 15% cumulative preference shares of no par value: GH¢30.0m

- The cost of winding up is estimated at GH¢21.3m.

- The bank overdraft and 18% debentures are secured by a floating charge on the company’s assets.

- The preference dividends and interest on debentures are two years in arrears. However, no provision has been made for these in the financial statement.

- The ordinary shareholders have decided to inject GH¢60.0m in consideration for a new issue of equity shares if the capital reconstruction scheme is accepted.

- Although it is the company’s policy to amortize intangible assets over five years, the Board of Directors has decided to maintain the Goodwill indefinitely in the books due to the persistent losses, in contravention of the company’s policy. Goodwill has been outstanding since 2009. The current financial state of the company negates the value and existence of the goodwill.

- The preference shareholders have indicated their willingness to bear any deficit resulting from the reconstruction in proportion to their interest in the stated capital. In return, their stake would be converted into equity, and they would be permitted to make nominations to key management positions, including chairing the board for the first five years. If these proposals are accepted, the preference shareholders will contribute further equity of GH¢60.0m. They have also agreed to waive 50% of the arrears of dividend and convert the rest into equity.

- Any arrears of preference dividends are to form a first charge upon any surplus on winding up.

- The original ordinary shareholders have decided to waive any dividend due to them during the first two years in order to put the company on sound financial ground.

- The company is expected to improve its cash flow position and commence dividend payments if the additional capital of GH¢120.0m is introduced.

Required:

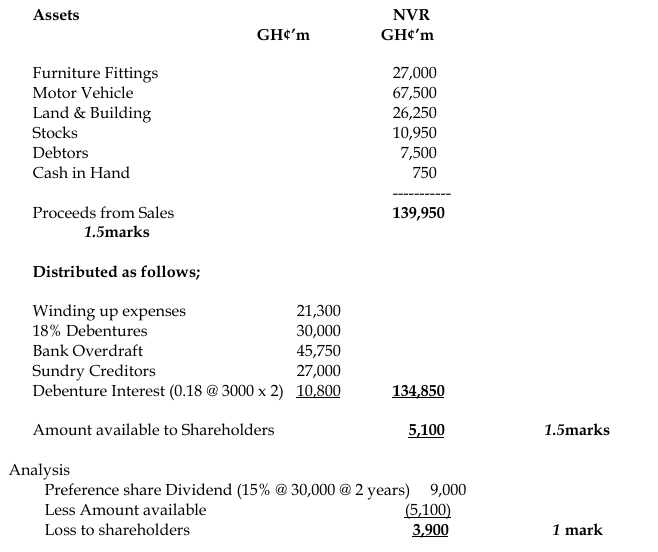

a) Calculate the amount available if Crave Cottage Industry Limited is liquidated and its distribution.

(7 marks)

b) Calculate the maximum possible loss of Crave Cottage Industry Limited and its allocation to Preference Share Capital and Ordinary Share Capital. (6 marks)

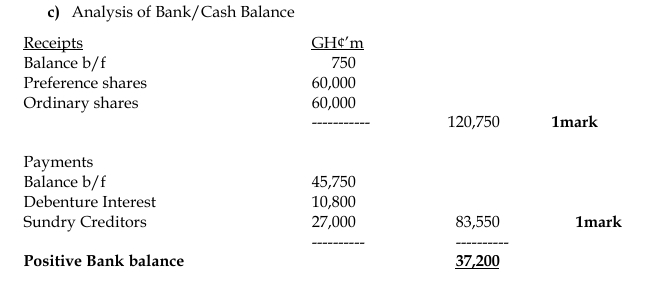

c) Calculate the Bank/Cash balance of Crave Cottage Industry Limited after the reorganization. (2 marks)

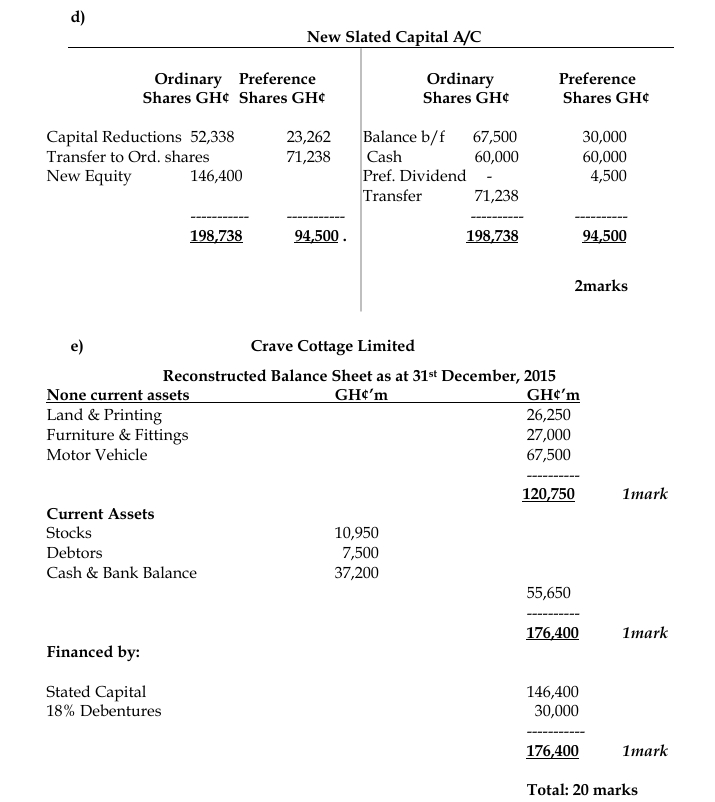

d) Calculate the new stated capital for the company after the reorganization. (2 marks)

e) Prepare a Statement of Financial Position of Crave Cottage Industry Limited showing the position immediately after the scheme has been put in place.

(3 marks)

Answer

5a) Liquidation Amount and Distribution

5b) Loss Allocation to Preference and Ordinary Shareholders

Therefore, the maximum possible loss is GH¢75,600 million, of which GH¢23,262 million is allocated to preference shareholders and GH¢52,338 million is allocated to ordinary shareholders.

(2 marks)