Question

Answer

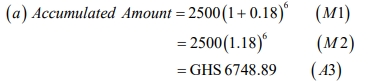

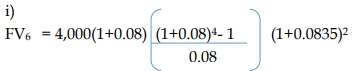

a)

= GH¢22,8530.01

ii)

Size of investment after withdrawal = 22,853.01 – 5,000

= GH¢17,853.01

iii)

Balance after the 8th year = ![]()

= GH¢20,958.94

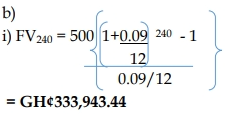

ii)

Amount deposited = 500 x (12 x 20) = GH¢120,000

iii)

Interest earned = GH¢333,943.44 – GH¢120,000 = GH¢213,943.44

iv)

= 15000(7.36) = GHS 110,400.00

The geometric mean of the rates of return is -7.52%.

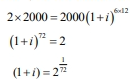

(i) Time to accumulate GHS 800 interest at 10% compounded quarterly:

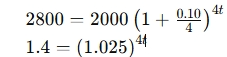

To calculate how long it will take for the GHS 2000 investment to accumulate GHS 800 interest at 10% compounded quarterly, we use the compound interest formula:

Where:

Taking logarithms:

Therefore, it will take approximately 3 years, 4 months, and 11 days for the investment to accumulate GHS 800 interest.

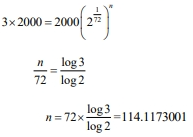

(ii) Time to triple in value if it doubles in 6 years:

If the GHS 2000 investment doubled in value in 6 years, it means the new value after 6 years is GHS 4000. To determine how long it will take for the investment to triple (GHS 6000), we use the same compound interest formula.

Let the time it takes to double be t=6t = 6 years and let the time to triple be t3t_3. We know the investment doubles in 6 years, so the interest rate is compounded monthly. Let rr be the interest rate.

Using the formula for doubling:

We now solve for r and use it to determine how long it will take to triple.

n= 9 years 6 months and 4 days

(iii) Interest rate for doubling in 6 years:

From the logarithmic equation, we have:

![]()

Therefore, the interest rate is 0.96 percent

Calculate the sum of the infinite geometric progressions:

(i) ![]()

(ii) ![]()

(i) The given geometric progression is ![]()

The sum to infinity of a geometric progression is given by: ![]()

(ii) The geometric progression is ![]()

The sum to infinity is ![]()

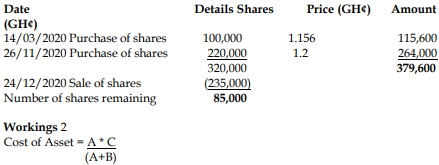

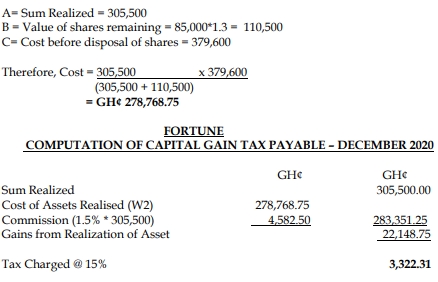

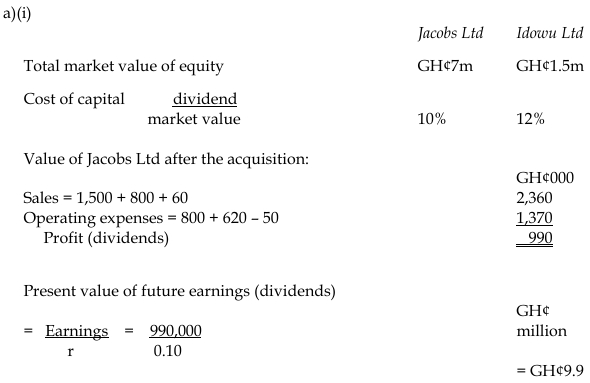

Computation of Cost of Shares Sold:

The sale of the unused machinery would generate GH¢100,000, so the total value after the acquisition is:

TotalValue=GH¢9,900,000+GH¢100,000=GH¢10,000,000Total Value = GH¢9,900,000 + GH¢100,000 = GH¢10,000,000

Step 5: Calculate the maximum price

The maximum price Jacobs Ltd should pay is the difference between the value after the acquisition and its current value before the acquisition.

ii) Minimum price Idowu Co Ltd shareholders should accept

The minimum price that the ordinary shareholders in Idowu Co Ltd should accept is the current market value of their shares.

Thus, the minimum price the ordinary shareholders in Idowu Co Ltd should accept is GH¢1,500,000.

(Total: 10 marks)

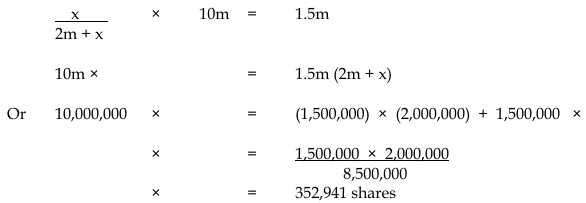

b)

The agreed takeover price for Idowu Co Ltd was GH¢1,500,000, based on the minimum acceptable price for Idowu’s shareholders as calculated in part 3(a)(ii).

We need to determine how the entire benefit from the acquisition will accrue to the shareholders of Jacobs Ltd using a share exchange mechanism.

Let x represent the number of new shares to be issued to Idowu Co Ltd’s shareholders. The total number of shares in issue after the acquisition will be 2,000,000 shares (since Jacobs Ltd originally has 2,000,000 issued shares).

The total value of Jacobs Ltd after the acquisition is GH¢10,000,000 (as calculated in 3(a)(i)).

For the benefit of the acquisition to accrue fully to Jacobs Ltd’s shareholders, the value of the shares issued to Idowu Co Ltd’s shareholders should equal the agreed takeover price of GH¢1,500,000. This gives us the following equation:

The market value per share after the acquisition will be:

![]()

Before the acquisition, the market value of Jacobs Ltd’s shares was GH¢3.50 per share. After the acquisition, the value of each share increases to GH¢4.25, representing a gain of GH¢0.75 per share.

For Jacobs Ltd’s original 2,000,000 shares:

2,000,000×0.75=GH¢1,500,000

Thus, the shareholders of Jacobs Ltd will receive the entire benefit from the acquisition, which is GH¢1,500,000, the same as the agreed takeover price.