Question

Answer

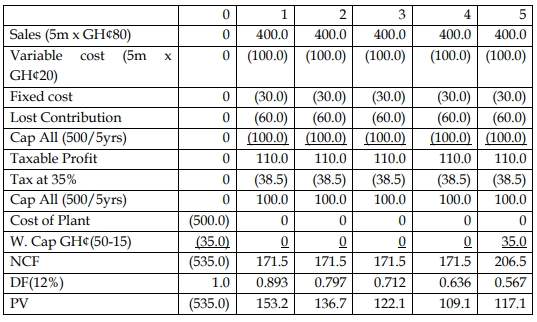

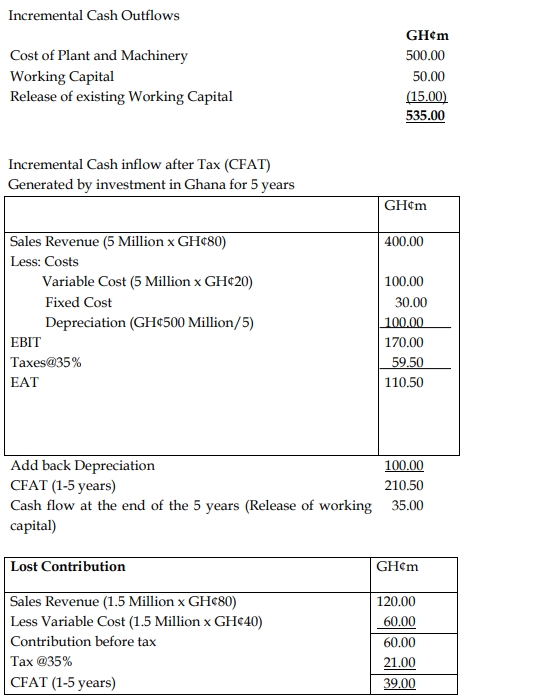

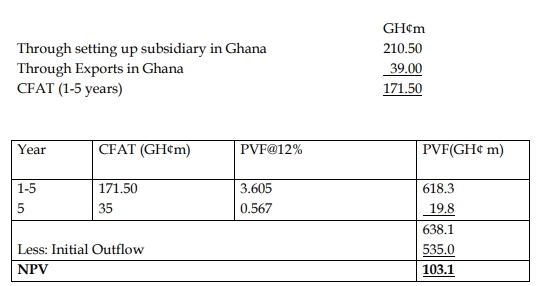

NPV = GH¢103.2m

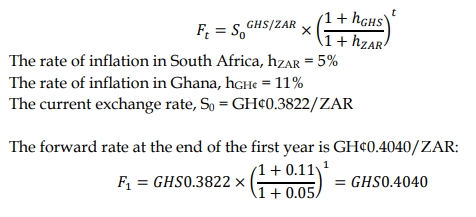

An alternative financial Analysis whether to set up the manufacturing units in Ghana or not may be carried using NPV technique as follows:

NPV = GH¢103.2m

An alternative financial Analysis whether to set up the manufacturing units in Ghana or not may be carried using NPV technique as follows:

i) Evaluation of impact of restriction on profit repatriation on the NPV

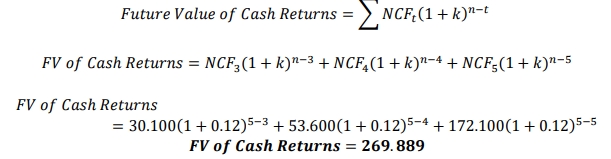

With a restriction on repatriation until exit, all cash returns from year 3 to the end of year 5 will be available to Rock only at the end of year 5 when it exits. As blocked funds can be invested at 12% in South Africa until the end of year 5, the amount that will be repatriated at the end of year 5 is the aggregate future value of the cash returns from year 3 to year 5.

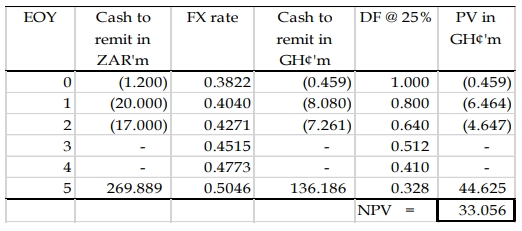

Change in NPV: The NPV decreases by 3.7% compared to the original NPV of GH¢34.325 million.

ii) Suggestions for dealing with blocked funds

Rock Minerals Ltd can manage the risk of blocked funds by implementing any of the following strategies:

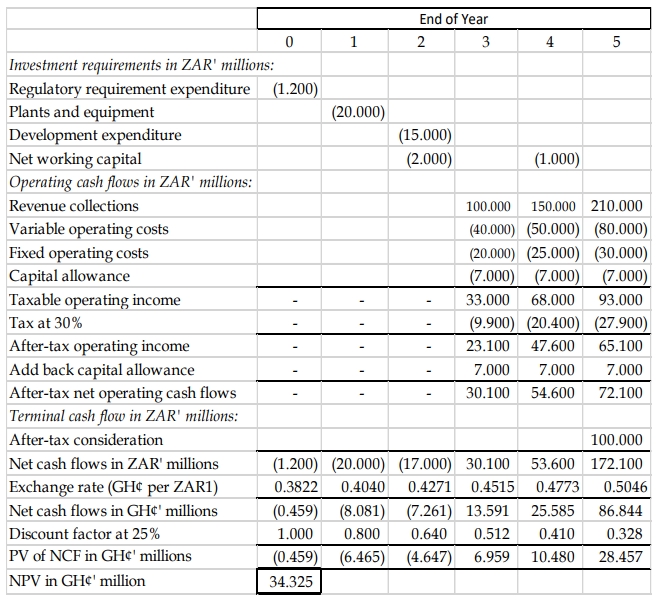

Evaluation of mining project using NPV with no restriction on repatriation

The project’s NPV

Recommendation:

The positive NPV of GH¢34.325 million suggests that the investment should be accepted as it will enhance the value of Rock Minerals Ltd.

Workings: