Question

Answer

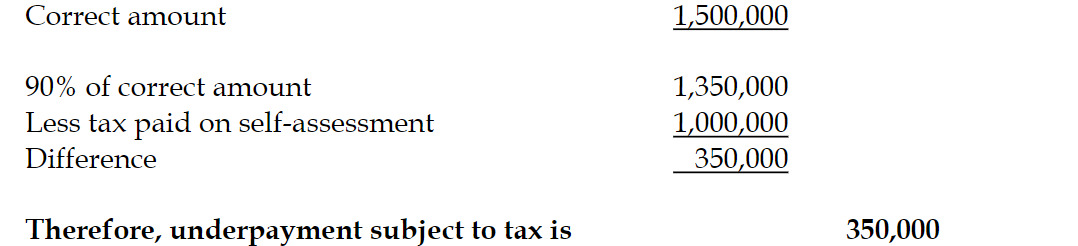

Computation of underpayment to be subjected to

Therefore, underpayment subject to tax is 350,000

(2 marks)

Computation of underpayment to be subjected to

Therefore, underpayment subject to tax is 350,000

(2 marks)