Question

Answer

a) Calculation of Contribution that Will Be Lost if Double Bed Production Ceases:

| Item | GHS |

|---|---|

| Potential loss of revenue | 2,800,000 |

| Less: | |

| – Material cost savings | 1,400,000 |

| – Variable labor cost savings (60% of 1,050,000) | 630,000 |

| – Variable manufacturing overhead savings (50% of 650,000) | 325,000 |

| – Variable administrative cost savings (20% of 100,000) | 20,000 |

| Total potential savings | 2,375,000 |

| Potential contribution to fixed costs that will be lost | 425,000 |

Conclusion:

A contribution of GHS 425,000 will be lost if Double bed production ceases. This loss in contribution will result in a decline in profit by the same amount since fixed costs will still be incurred. Therefore, the company should continue the production of Double beds.

ALTERNATIVELY

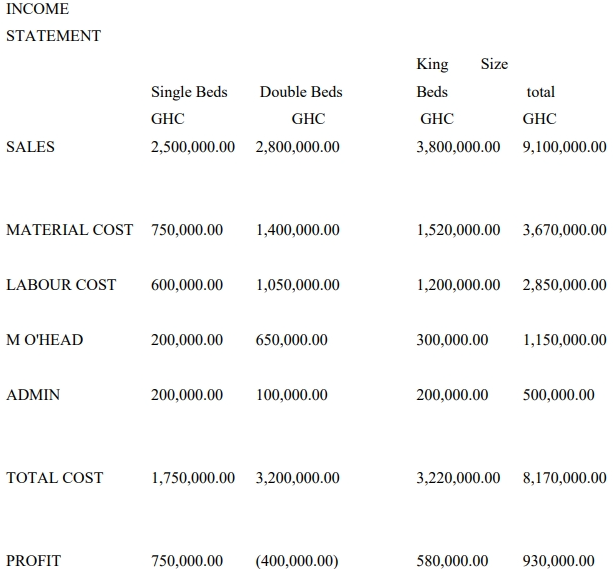

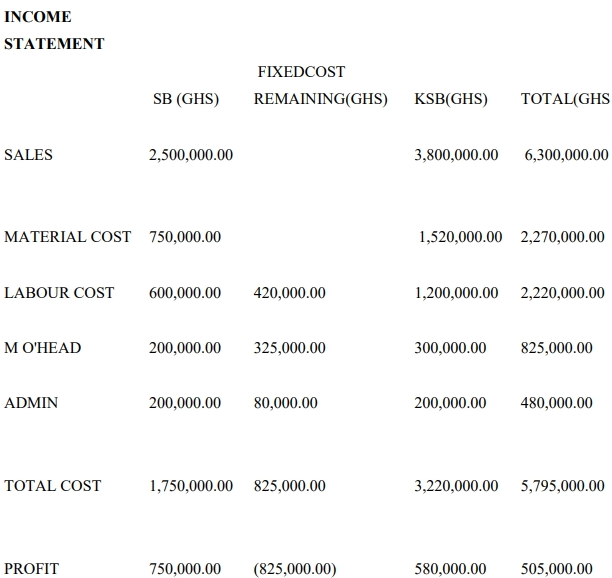

In this case profit reduced from GHC 930,000 to GHC 505,000 a reduction of GHC425, 000

b) Income Statement for 80 Units of Each Product:

| Item | Single bed | Double bed | King Size bed | Total |

|---|---|---|---|---|

| Sales (GHS) | 40,000 | 64,000 | 76,000 | 180,000 |

| Material Cost | 12,000 | 32,000 | 30,400 | 74,400 |

| Labor Cost | 5,760 | 14,400 | 14,400 | 34,560 |

| Manufacturing O’head | 1,600 | 7,428.57 | 3,000 | 12,028.57 |

| Administrative Cost | 640 | 457.14 | 800 | 1,897.14 |

| Total Variable Cost | 20,000 | 54,285.71 | 48,600 | 122,885.71 |

| Contribution | 20,000 | 9,714.29 | 27,400 | 57,114.29 |

| Less Incremental Fixed Costs | 80,000 | |||

| Loss on Order | 22,885.71 |

Conclusion:

The order should be rejected because it will result in an incremental loss of GHS 22,885.71 unless Alom Hotel Limited is willing to pay a higher price to cover the additional costs associated with producing the extra units.