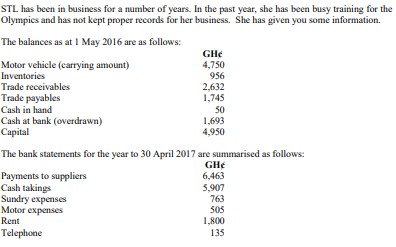

Question

Answer

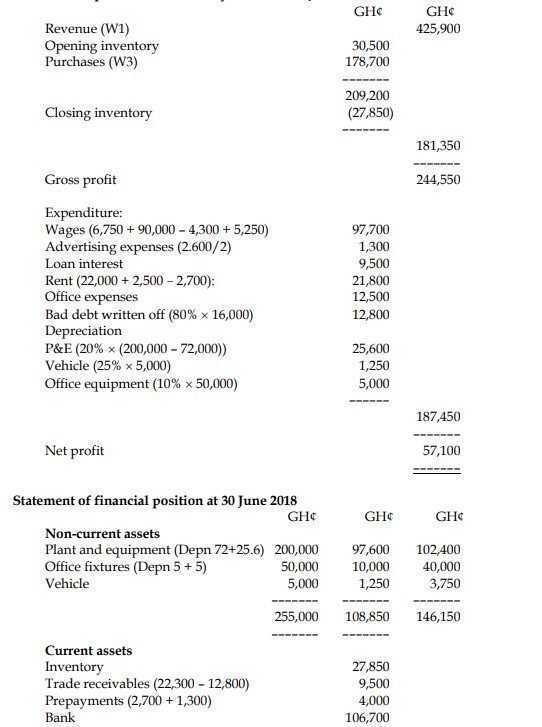

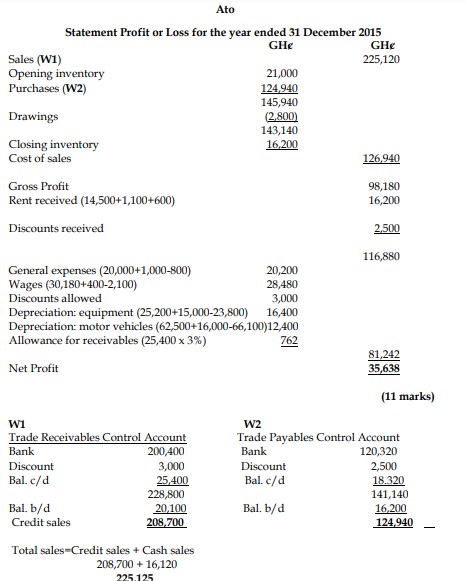

(a) Estimate of Mala’s profit for the year ended 31 December 2015

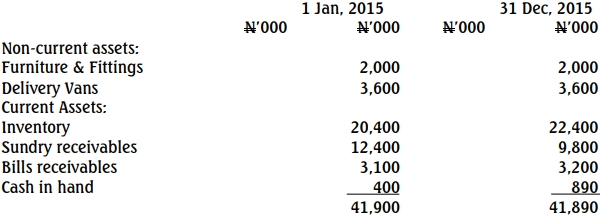

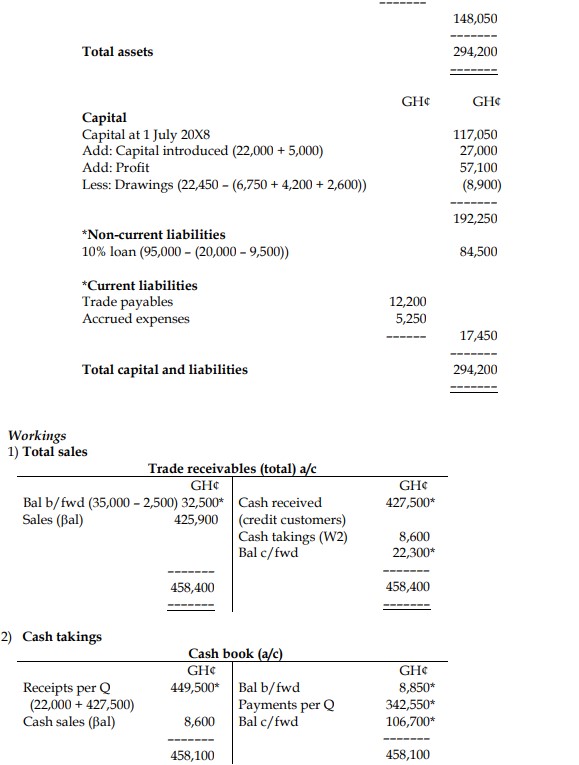

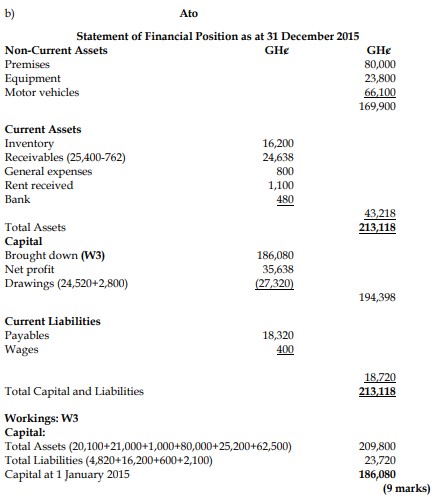

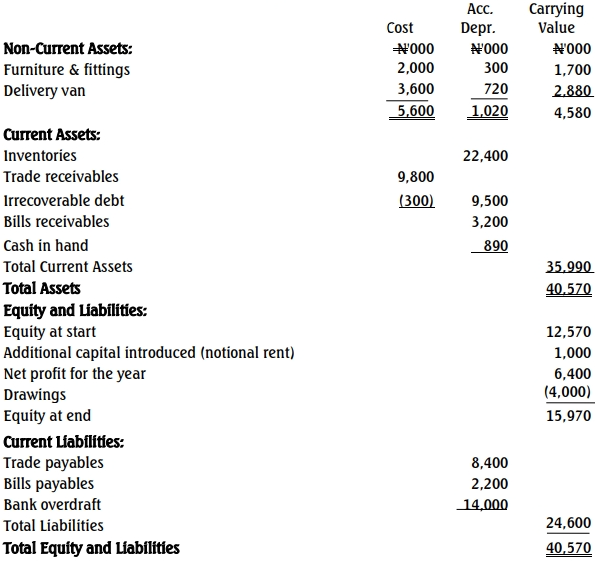

(b) Statement of financial position as at December 31, 2015

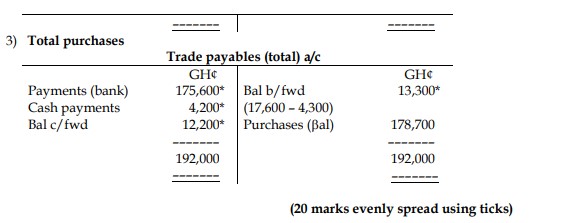

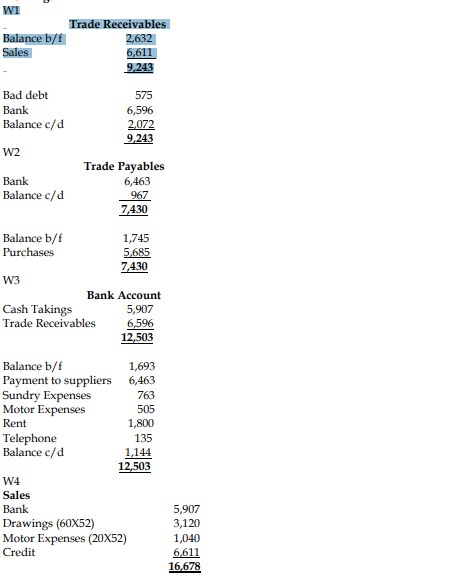

WORKING NOTES

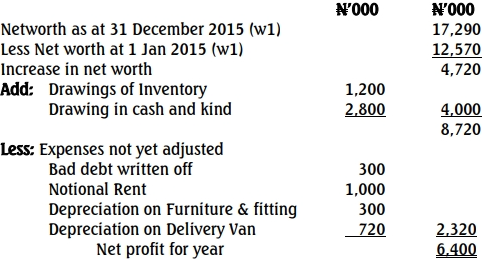

W1 Calc. of Net Worth/Capital as at