Question

Answer

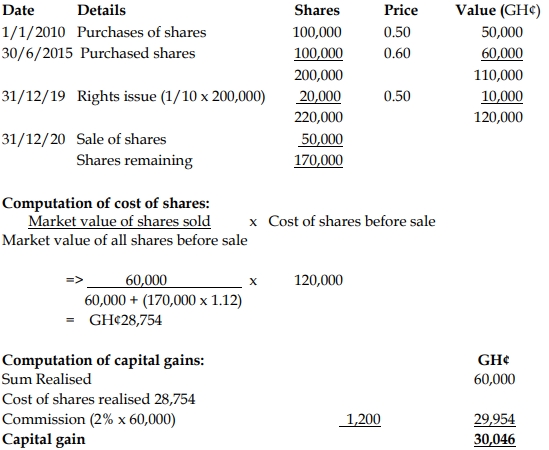

Computation of Cost of Shares:

Maame Adwoa Konadu Yiadom is a shareholder of Asokwa Company Ltd, a company not listed on the Ghana Stock Exchange Market. Maame Adwoa Konadu Yiadom transacted the following business with Asokwa Company Ltd:

Required:

Calculate the capital gain tax, if any.

Computation of Cost of Shares:

Kawukudi Ltd intends to increase its capital requirement. Therefore, it applied to the Registrar General with the following:

Retained Earnings Account (GHȼ)

Required:

Assess with explanation the tax payable under this circumstance.

The transfer of GH¢600,000 as income from the income surplus account to the stated capital is referred to as ‘deemed dividend’. This implies that a tax at the rate of 8% shall be imposed on the transfer. Thus, 600,000 X 8% = GH¢48,000.

There will also be a stamp duty payment of 0.5%. Thus, 0.5% x 600,000 = GH¢3,000.

The Chief Executive Officer of LOBILO Limited, producers of Alata Local Soap for the Ghanaian market, returned from a Tax Seminar organized by The Institute of Chartered Accountants, Ghana (ICAG) and called you, the Tax Manager of LOBILO, into his office and stated:

“LOBILO Company Limited has been shortchanged over the years on account of tax losses.” He said that carryover of losses as an incentive was discussed at length at the Tax Seminar. He further added that LOBILO Limited has not carried over its tax losses as provided for in the tax laws. He states, “Tax Manager, please act now by writing to the Ghana Revenue Authority to recognize the tax losses of LOBILO, since the losses are within the five years in order to help reduce the taxes of the Company now that the Company is making profits,” he ended.

You are required to:

Explain clearly the provision of tax laws on carryover of losses and to what extent do you agree with the position of the Chief Executive Officer of LOBILO Company Limited.

Under section 22 of the Internal Revenue Act 2000, Act 592, as amended by Act 2002, Act 622, Act 2006, Act 700, and Act 2007, Act 731, there shall be deducted losses of the previous five years incurred by that person on that business. The loss shall be deducted in the order in which they occur.

Persons that can carry their losses are as follows:

i. Farming business

ii. Mining business

iii. Information Technology Business (ICT – Software development)

iv. Tourism business registered with the Ghana Tourism Authority

v. Agro-processing companies

vi. Manufacturing mainly for exports

vii. A loss incurred by a qualifying venture capital financing company from the disposal of shares in any venture investment under section 17 of the Venture Capital Trust Fund Act, 2004 (Act 684)

viii. In the case of petroleum upstream contractors, they are permitted to carry over their losses indefinitely.

In conclusion, it is not all persons that are allowed to carry over their losses.

The statement by the Chief Executive Officer can, therefore, be supported by the provision of the law as the Company is into the production of the Alata Soap, which is covered under the carryover of loss provision under section 22 of the Internal Revenue Act 2000, Act 592, as amended. Any effort put in by LOBILO Company Limited to enjoy the benefit on the carryover of losses can be sustained.

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.