Lawaaba Guo is a Ghanaian born in Nigeria and has lived all his life there. He got an opportunity to relocate to Ghana and took up an appointment as a lecturer in one of the prestigious universities within the first three months of his arrival in Ghana in 2018.

He took up employment with ABB Ltd as a procurement officer. The following relates to his employment details for 2020 year of assessment:

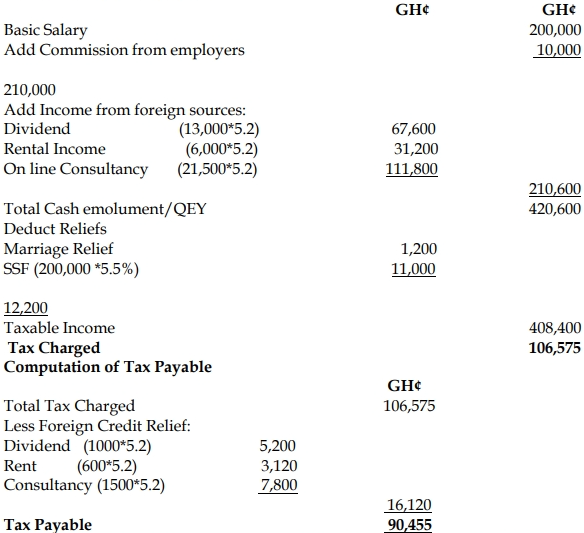

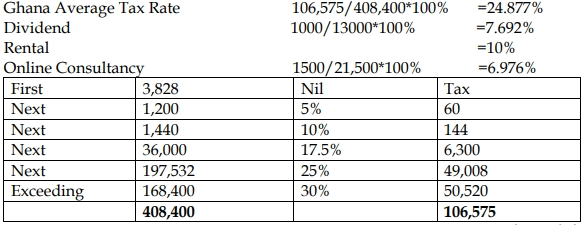

Salary: GH¢200,000

Commission from employers: GH¢10,000

Interest on savings from a Bank in Ghana (Gross): GH¢1,000

His investment income and other returns received from Nigeria are as follows:

Dividend of US$ 12,000 net of tax. Tax of US$ 1,000 was paid.

Rental Income of USD 6,000 gross with tax at the rate of 10%.

On-line consultancy fee USD 20,000 net of tax. Tax of USD1,500 was paid.

Additional information:

He is married.

Children (2): both schooling in Nigeria.

Contributes to Social Security at 5.5%.

Exchange Rate USD1 = GH¢5.2.

Required:

Determine the following:

i) Chargeable Income

ii) Tax Payable

iii) Amount of foreign credit relief granted

Any resident person other than a partnership may be allowed a foreign tax credit relief on any income that is earned outside Ghana subject to the fulfillment of certain conditions, which are critical in the granting of the relief.

Required:

What are the conditions to satisfy before the foreign tax credit relief is granted?

Answer

The foreign tax credit relief is granted subject to the following conditions:

Income Assessment: The income corresponding to the tax must have been assessed.

Tax Credit Certificate: Submission of a tax credit certificate from the tax department of the foreign country signifying the nature of income and the quantum of taxes paid by the taxpayer.

Official Receipt: Providing an official receipt or a functional equivalent of a tax credit certificate from the tax department of the foreign country.