Question

Answer

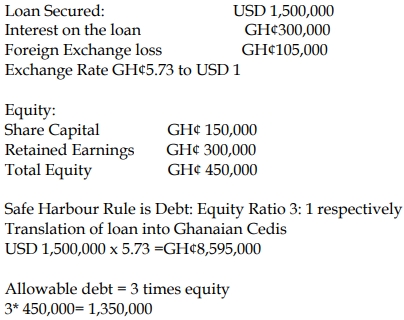

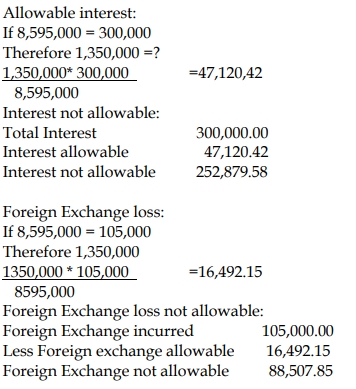

The following information is relevant to Mandy Ltd (Ghana), a subsidiary of Menkay Incorporated, a company resident in Japan.

Following Mandy Ltd’s operational challenges, a loan of US$1,500,000 was secured from its parent company in 2019 year of assessment.

Additional information relevant to Mandy Ltd’s operations:

| Description | Amount (GH¢) |

|---|---|

| Interest on loan paid in 2019 | 300,000 |

| Foreign exchange loss | 105,000 |

| Equity: | |

| Share capital | 150,000 |

| Retained earnings | 300,000 |

| Total equity | 450,000 |

Exchange rate: 1US$ = GH¢5.73

Required:

Determine the tax implication of the above transaction.

a) The current level of government borrowing has become a topical issue for discussion, causing observers to wonder whether borrowing is good or bad. In the light of this, you are required to:

Below is the capital structure of Nyameke Ghana Limited for the 2014 year of assessment:

| GH¢ | |

|---|---|

| Equity | 20,000,000 |

| Loans | 80,000,000 |

| Total | 100,000,000 |

The loans were taken by Nyameke Limited from the parent company based in Nigeria. During the year under review, the subsidiary paid GH¢700,000 as interest on the loan and also incurred an exchange loss of GH¢500,000 on the repayment of a loan taken earlier from the parent company.

Required:

Determine how the above transaction will be treated for tax purposes. (6 marks)

This is a case of interest and foreign exchange loss being subjected to thin capitalization rules. The thin capitalization rules typically limit the amount of interest that can be deducted for tax purposes based on a prescribed debt-to-equity ratio.

Summary:

| Item | Total (GH¢) | Allowable (GH¢) | Disallowed (GH¢) |

|---|---|---|---|

| Interest | 700,000 | 350,000 | 350,000 |

| Foreign Exchange Loss | 500,000 | 250,000 | 250,000 |

| Withholding Tax on Interest | 56,000 | – | – |

The management of Kelkadadi Ltd, a company resident in Ghana since the year of assessment 2007, is a wholly owned subsidiary of Danlerigu Ltd, a company resident in Nigeria. The Finance Manager of Kelkadadi has invited you as a final level three candidate of ICAG and also a Tax Intern with Danlerigu to analyze the transaction below and provide tax implications thereon.

Kelkadadi Ltd contracted a loan of $10 million from Danlerigu Ltd to help it meet its operational activities. The balance standing on the loan account at the beginning of 2018 stood at $5 million and $4.1 million at the end of 2018 year of assessment. The exchange rates are as follows:

The extract of the financial statement at the beginning of the year 2018 was as follows:

Interest on the debt paid during the year amounted to GH¢90,124 and foreign exchange loss on the loan repayment stood at GH¢147,000.

Required:

Write a memo on the possible tax implication(s) on this arrangement to the Finance Manager.

MEMO

TO: Tax Manager

FROM: Tax Intern

DATE: 7th July 2019

SUBJECT: Tax Implication on Thin Capitalization Rules

INTRODUCTION

Following your request for me to provide the tax implication on the thin capitalization, I furnish as follows:

ISSUES

Kelkadadi Ltd is a subsidiary of Danlerigu and any loan that is granted shall be subject to Thin capitalization rule which states that the debt secured should not be more than 3 times the equity of the entity.

In this particular situation, the debt exceeds the three times. Consequently, the interest paid or payable that exceeds the 3:1 ratio shall be added to income and taxed and also the foreign exchange loss paid or payable.

Additionally, the total interest paid or payable attracts a withholding tax at the rate of 8%.

Summary of Interest

Total Interest: GH¢90,124.00

Interest Allowable: GH¢14,922.45

Interest to be disallowed (difference): GH¢75,201.55

From W2 as attached, total interest of GH¢90,124.00 shall attract interest at 8% which is (90,124.00 * 8%)=GH¢7,209.92

Interest of GH¢75,201.55 shall be disallowed, meaning it should not be an allowable deduction out of GH¢90,124 with GH¢14,922.45 allowable.

Summary of Foreign Exchange Loss

Total Foreign Exchange: GH¢147,000.00

Foreign Exchange Allowable: GH¢24,339.81

Foreign Exchange unallowable: GH¢122,660.19

From W3 as per the schedule attached, the total foreign exchange loss of GH¢147,000 only GH¢24,339.81 shall be allowable with GH¢122,660.19 not allowable for tax purposes.

CONCLUSION

In conclusion, the attached schedule will aid your comprehension of the issues as stated above.

Thank you.

Yours faithfully,

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.