Question

Answer

Financial appraisal of ABC Ltd’s proposed air conditioner manufacturing project

The project presents different business risk (as it involves a new business venture) and increases

financial risk (as its financing method will increase the company’s gearing). In addition, there are associated financing side effects that need to be factored into the financial appraisal. Adjusted

present value (APV) will be a more efficient appraisal method than the traditional NPV

approach.

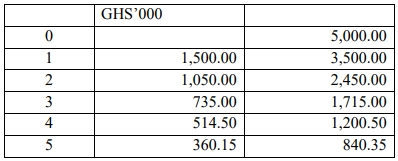

Step 1: Compute the base case NPV

Workings:

1. Tax-allowable depreciation

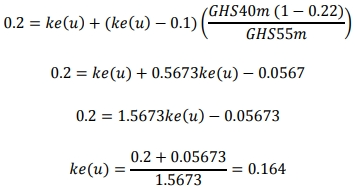

2. Cost of equity as if company is ungeared

As the new project is a completely new business, an appropriate cost of equity is one that

reflects the level of business risk associated with the new business. This can be derived from

that of the competitor, XYZ as under:

Using MM Proposition II with tax:

![]()

XYZ’s cost of equity, ke(g) = 20%

Market value of XYZ’s equity = 10m x GHS5.5 = GHS55m

Market value of XYZ’s debt = GHS40m

XYZ’s tax rate, t = 22%

Cost of debt, kd = 10% (taken to be the treasury note rate)

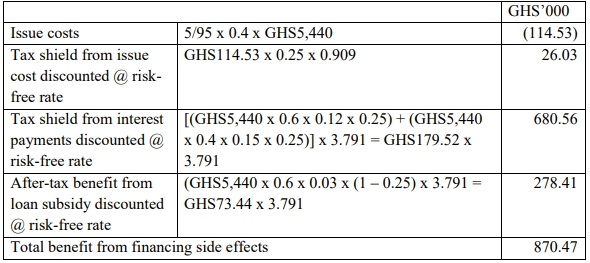

Step 2: Calculate PV of financing side effects

Financing side effects that apply in this case are –

- the issue cost and its associated tax shield

- annual interest payments on debt financing

- benefit from subsidized loan from the government

Necessary adjustments for the financing side effects follow.

Notes:

- The issue costs may be included in funds borrowed instead.

- The calculation above assumes that the entire issue costs will be expensed in the

first year. One may choose to amortize it over the 5-year forecast period and

discount the annual tax shields accordingly. - PV of tax shield and subsidy benefit are based on the 5-year government debt yield

rate. It may be discounted at the company’s cost of debt, 15% (5-year yield rate

plus 500 basis points) on the grounds that the benefits will accrue to the company

only when it is able to discharge its financial obligation and 15% reflects the credit

risk of the company.

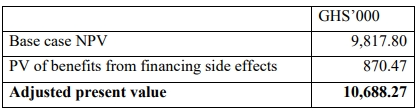

Step 3: Compute APV by adjusting base case NPV for financing side effects

Conclusion:

As the APV is positive, the value of ABC will increase if the proposed project is implemented.