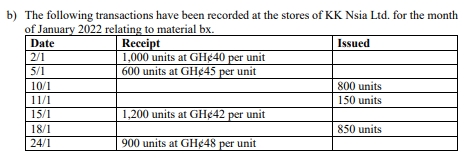

Question

a) Inventory refers to the goods and materials that a business holds for the ultimate goal of resale, production, or utilization in the near future. Inventory could be in the form of raw materials, finished goods, work in progress, among others.

Required:

Identify FIVE (5) reasons actual inventory counted may be different from the balance in the inventory records. (5 marks)