Question

Answer

a) Three Advantages of Expansion Through Acquisition Over Organic Expansion:

- Speed of Market Entry:

Acquiring an existing company like Akwaaba allows Lekker to enter the Ghanaian market quickly, without the delays associated with setting up a new subsidiary from scratch. - Established Market Presence:

Through acquisition, Lekker would gain immediate access to Akwaaba’s existing customer base, established brand, and market relationships, which would take time to develop through organic growth. - Lower Risk:

Acquiring an existing, successful company like Akwaaba reduces the risk associated with entering a new market, as the business model, management team, and market strategy are already proven.

(6 marks)

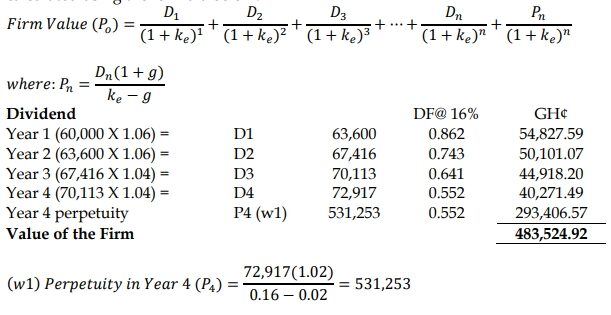

b) Value of Akwaaba Using the Dividend Valuation Model:

The Dividend Valuation Model (DVM) can be used to value Akwaaba based on its expected future profits:

Note that the perpetuity is calculated from Year 4 onwards, therefor the discount

factor is the same as that of Year 4 and not Year 5

Conclusion: the purchase consideration of GH¢450,000 quoted by the Ghanaian

filmmaker is lower than the value of the firm, leading to a net gain of 33,524.92.

Based on this Lekker Inc. should purchase Akwaaba Inc

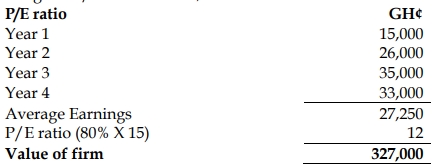

c) Expected Value of Lekker’s Subsidiary Using the P/E Ratio Method:

d) Two Reasons Mergers and Acquisitions May Fail to Achieve Expected Outcomes:

- Cultural Integration Issues:

Differences in corporate cultures can lead to conflicts and inefficiencies post-merger, hampering the realization of expected synergies. - Overvaluation of Target Company:

If the acquiring company overestimates the value of the target company, the merger may not deliver the anticipated financial benefits, leading to losses.

(2 marks)