Question

Answer

i) Maame Agyeiwaa

b) Maame Agyeiwaa is a junior staff member of KayDee Ltd. Her monthly basic salary is GH¢800. She was paid an overtime allowance totalling GH¢100 during the month of January 2021. In February 2021, Maame Agyeiwaa was paid overtime allowance totalling GH¢500.

Required:

i) Compute her tax liability on the overtime allowance for the month of January 2021.

(2 marks)

ii) Compute her tax liability on the overtime allowance payments for the month of February 2021.

(3 marks)

i) Maame Agyeiwaa

Bisa works with Kaydei Ltd and earns an annual basic salary of GH¢140,000. He was paid a bonus of GH¢45,000 in 2021.

Required:

Determine the tax liability on the bonus.

(3 marks)

Bisa

Bonus as a percentage of basic salary

Bonus is more than 15% of annual basic salary therefore part of the bonus will be

taxed at 5% and the excess will be taxed at graduated rate.

Tax on Bonus: GH¢ GH¢

15% x GH¢140,000 = 21,000 x 5% = 1,050.00

Total Bonus 45,000

Added to other income 24,000

Gift means a receipt without consideration or for inadequate consideration.

When an individual receives a gift in relation to employment, business, investment, or otherwise, the following tax treatment applies:

1. Income Inclusion: The gift is added to the individual’s income and is taxed accordingly.

3. Tax Rate for Gifts: The individual may elect for the gift to be taxed separately. In such a case, the gift will be taxed at the rate of 15% on the total value of taxable gifts received by the person within a year of assessment.

(5 marks)

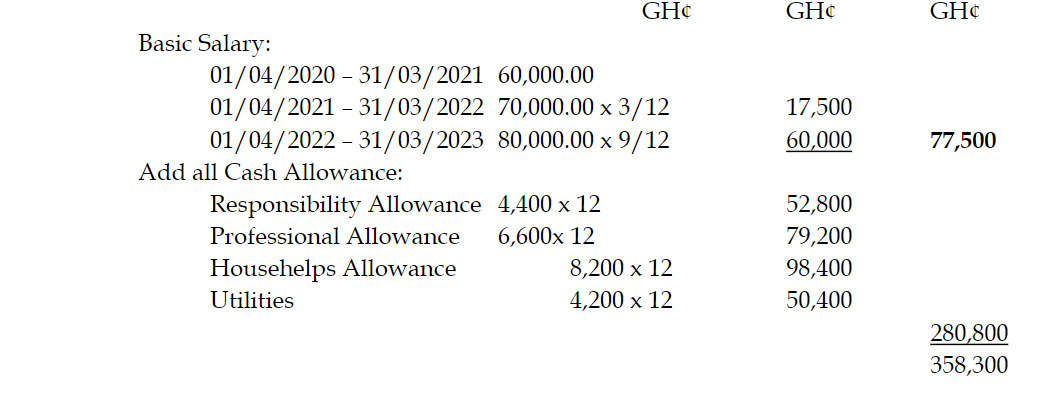

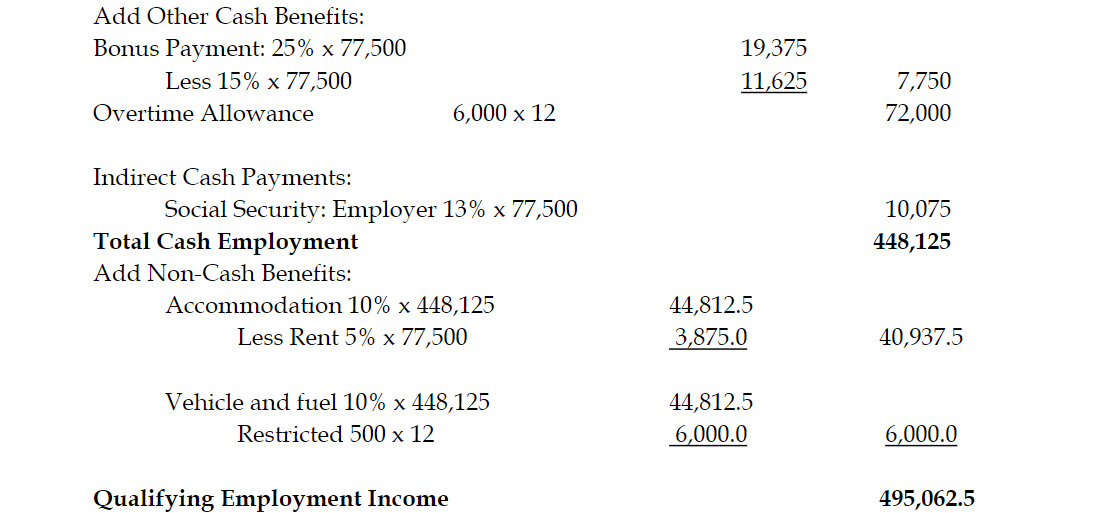

Mr. Antitom (physically challenged) was employed as a Chief Accountant of Nangode Ltd on 1 April 2020 on an annual basic salary of GH¢60,000 x 10,000 – GH¢100,000. He was entitled to the following monthly allowances and benefits:

Allowances & Benefits Monthly Amount (GH¢)

Responsibility Allowance 4,400

Professional Allowance 6,600

House Help Allowance 8,200

Utilities 4,200

Overtime Allowance 6,000

Provision of furnished accommodation by the employer for which he paid 5% of his basic salary.

Provision of vehicle and fuel by the employer for both official and private use.

Bonus payment amounting to 25% of his basic salary.

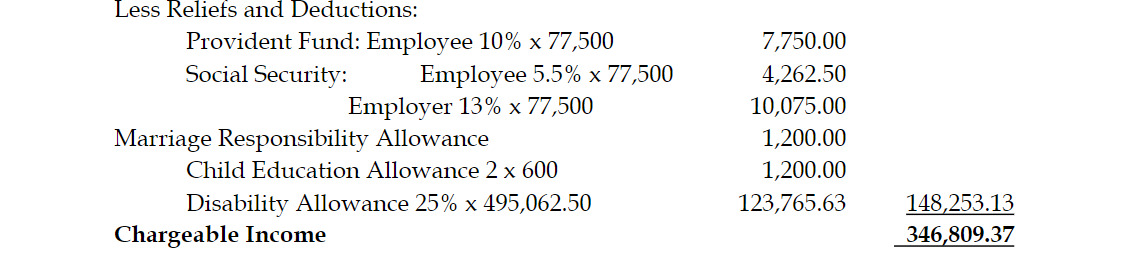

He contributed 5.5% of his basic salary to the Mandatory Pension Scheme and an additional 10% to a Voluntary Pension Scheme approved by the National Pension Regulatory Authority.

Married with 3 children, 2 in approved Senior High Schools in Ghana, 1 at the University of South Africa.

Earned interest of GH¢4,000 on a savings account with Kilma Bank.

Received a net dividend of GH¢20,480 from an investment with Enoga Securities.

Required:

Compute the chargeable income of Mr. Antitom for the 2022 year of assessment.

(20 marks)

Antitom Computation Of Chargeable Income Year Of Assessment: 2022

Basis Period: January to December, 2022

Add Other Cash Benefits:

Less Reliefs and Deductions:

Note: Candidates who considered the non-taxation of interest and dividend income correctly were awarded marks.

(20 marks evenly spread using ticks)

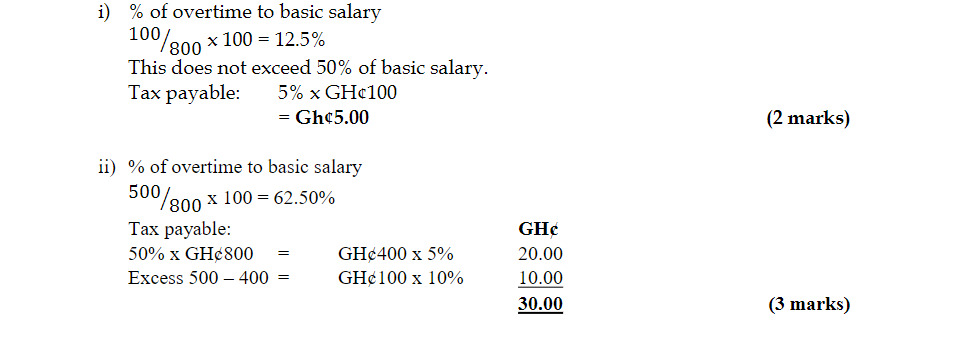

a) King Peter is a Junior Staff member of Sir James Company Limited. His monthly basic salary is GH¢700.00. He was paid overtime totaling GH¢50.00 during the month of January 2019.

Required:

i) Compute his tax liability on overtime for the month of January 2019. (2 marks)

In the month of February 2019, King Peter was paid overtime totaling GH¢500.00.

ii) Compute his tax liability on the overtime payments for the month of February 2019. (3 marks)

i) January 2019:

Description Amount (GH¢)

Percentage of overtime to basic salary: GH¢50/GH¢700 x 100% = 7.14%

This does not exceed 50% of basic salary.

Tax payable (5% of the overtime amount) 5% x GH¢50.00 = GH¢2.50

(2 marks)

ii) February 2019:

Description Amount (GH¢)

Percentage of overtime to basic salary: GH¢500/GH¢700 x 100% = 71.43%

This exceeds 50% of basic salary.

Tax payable will be calculated as follows:

(3 marks to be allocated)

c) What are the taxation rules for overtime payments and bonus payments under employment income?

(7 marks)

Overtime Payments:

Where an employer makes a payment for overtime work to a qualifying junior employee during a year of assessment, and the payment is up to 50% of the basic salary of the employee for the month, the employer is required to withhold tax at the rate of 5% from the payment. Any excess above the 50% is taxed at 10%.

A junior employee is the one whose qualifying employing income does not exceed eighteen thousand currency points (GH¢18,000.00) per annum.

(2 points @ 1.5 marks = 3 marks)

Bonus Payments:

(4 points @ 1 mark each = 4 marks)

What constitutes employment for the purposes of tax? (4 marks)

For tax purposes, employment is defined as follows:

Additionally, employment for tax purposes involves a contract of service rather than a contract for service, meaning the employer bears the risk of losses, and the employee is entitled to certain benefits and remuneration.

The table below shows the incomes of three employees of Agana Ltd in 2022 year of assessment.

| Income Details | Adom | Aseda | Ayeyie |

|---|---|---|---|

| Basic Salary (GH¢) | 120,000 | 160,000 | 180,000 |

| Medical Allowance (5% of Basic Salary) | 6,000 | 8,000 | 9,000 |

| Rent Allowance (10% of Basic Salary) | 12,000 | 16,000 | 18,000 |

| Fuel Allowance (15% of Basic Salary) | 18,000 | 24,000 | 27,000 |

| Total Cash Emoluments | 156,000 | 208,000 | 234,000 |

Besides the cash emoluments stated above, the employees received loans from the employer as follows:

i) Adom received a loan of GH¢24,000 at a rate of 5% payable within 12 months.

ii) Aseda received a loan of GH¢48,000 at a rate of 8% payable within 24 months.

iii) Ayeyie received a loan of GH¢100,000 at a rate of 10% payable within 36 months. This loan is in addition to an outstanding loan of GH¢50,000 with the same terms and conditions during the previous twelve months. (Assume that the statutory rate is 30% per annum).

Required:

Determine the loan benefits applicable to each of the three employees for the 2022 year of assessment. (16 marks)

i) Adom

Since the loan repayment period does not exceed 12 months and the loan amount does not exceed Adom’s three months’ basic salary (GH¢30,000), no loan benefit is applicable for Adom.

(4 marks)

ii) Aseda

Loan Benefit Formula:

Loan benefit = (Interest payable at statutory rate) – (Interest paid by the employee)

= (GH¢48,000 × 30% × 2 years) – (GH¢48,000 × 8% × 2 years)

= GH¢28,800 – GH¢7,680

= GH¢21,120

Since the taxable loan benefit is limited to 25% of the total benefit:

Taxable loan benefit = GH¢21,120 × 1/4 = GH¢5,280

Applicable for 2 years, loan benefit for 2022 = GH¢5,280 ÷ 2 = GH¢2,640

(5 marks)

iii) Ayeyie

Loan Benefit Formula:

Loan benefit = (Interest payable at statutory rate) – (Interest paid by the employee)

= (GH¢150,000 × 30% × 3 years) – (GH¢150,000 × 10% × 3 years)

= GH¢135,000 – GH¢45,000

= GH¢90,000

Since the taxable loan benefit is limited to 25% of the total benefit:

Taxable loan benefit = GH¢90,000 × 1/4 = GH¢22,500

Applicable for 3 years, loan benefit for 2022 = GH¢22,500 ÷ 3 = GH¢7,500

(5 marks)

An individual who is required to furnish the Commissioner-General (CG) with a return in relation to a gift has to do so to enable the CG subject it to appropriate tax.

Required:

Explain the treatment of a gift not received under employment or business.

An individual who receives a gift not related to employment or business can elect to have the market value of the gift taxed separately at a flat rate of 15%. The individual must furnish the Commissioner-General with a written return within 30 days of receiving the gift. The return is necessary to include the gift in the calculation of profits and gains of the individual, as required by the Income Tax (Amendment) (No. 2) Act, 2016 (Act 924)

Abotsi has been in employment at Asempa Ltd since 1 August 2019 as Finance Manager on a salary scale of GH¢32,000 by GH¢8,000 to GH¢48,000.

His service conditions include the following:

i) Responsibility allowance of 18% of basic salary

ii) Utilities allowance per annum of 10% of basic salary

iii) Risk allowance of 20% on basic salary and car maintenance allowance of 5% of basic salary

iv) Leave allowance of GH¢1,900 per annum

v) Medical allowance per annum of GH¢3,500

vi) Meals allowance of GH¢700 per month

vii) Two house helps on GH¢500 wages per month each. The amount is paid to Abotsi in cash directly by the company

viii) Bonus of 25% of annual basic salary

ix) Annual Overtime allowance of GH¢18,000

x) Unaccountable entertainment allowance of GH¢2,000 a year

xi) Provision of a well-furnished bungalow in respect of which he pays GH¢400 per month as rent by way of deduction at source

xii) Provision of a vehicle with driver and fuel for both official and private purposes

xiii) Special retirement package by way of a provident fund of which he contributes 9% of his basic salary, while the company contributes 11%. (The scheme is approved by the regulatory body)

xiv) Social Security and National Insurance Trust contribution of 5.5% and the employer contributes 13% of basic salary

xv) On 1 January 2021, he was given a car loan of GH¢20,000 to purchase a car for his mother at a simple interest rate of 15% per annum. The institution gives similar facilities to other customers at the rate of 28% but the statutory rate (Bank of Ghana rate) is 25%. The loan is to be paid within the period of 24 months

xvi) He is married to Abotsiwaa and Abotsimaa who are unemployed and contribute little or no financial support to their husband. Their responsibilities are limited to the management of the house

xvii) He has six (6) children, four (4) of whom are in Silicon Valley International School, Accra-Ghana, while the rest are working

xviii) He is also responsible for the upkeep of four (4) aged relatives of his

xix) He is currently pursuing MPHIL in Finance at UPSA where he incurred GH¢25,000 by way of educational expenses in 2021

xx) He is a director of Adwoa Mansa Ltd and receives a director’s emolument of GH¢24,450 (net of taxes)

xxi) He received a dividend of GH¢20,000 (net of taxes) from the Afia Manu Bank. The dividend was taxed at 8%.

Required:

Calculate his chargeable income for the 2021 Year of Assessment. (20 marks)

Abotsi – Computation of Chargeable Income

Year of Assessment: 2021

Basis Period: January to December

| Description | GH¢ |

|---|---|

| Basic Salary (August 2019 – July 2020) | 32,000.00 |

| Basic Salary (August 2020 – July 2021) | 40,000.00 (7/12) = 23,333.33 |

| Basic Salary (August 2021 – July 2022) | 48,000.00 (5/12) = 20,000.00 |

| Total Basic Salary: | 43,333.33 |

Total Cash Employment Income: GH¢126,833.33

Qualifying Employment Income: GH¢142,416.66

Net Employment Income: GH¢120,733.33

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.