Question

Answer

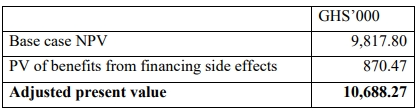

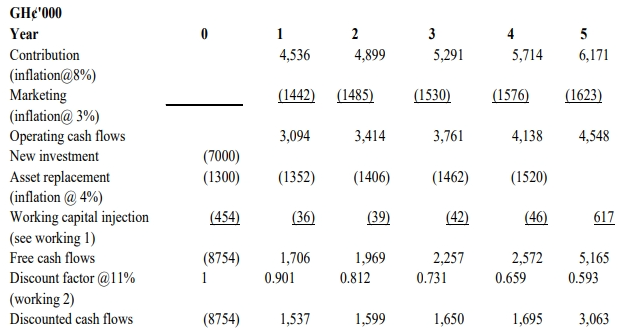

The Net present value = -8754 + 1,537+1,599+1,650+1,695+3,063 = 790,000

The positive NPV shows the project is worthwhile.

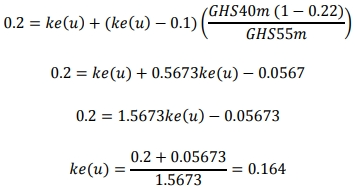

W2, cost of capital

(1+i)=(1+r)(1+h)=(1+0.06)(1+0.047)=1.11, hence 11%