Question

Answer

a)

| Quarter | Trend Sales Units | Actual Sales Units | Variation |

|---|---|---|---|

| 1 | 18,000 | 20,250 | +12.5% |

| 2 | 21,000 | 19,425 | -7.5% |

| 3 | 24,000 | 25,200 | +5.0% |

| 4 | 27,000 | 24,300 | -10.0% |

Forecast sales:

- Year 2 Quarter 1 = 15,000 + (3,000 x 5) = 30,000 + 12.5% = 33,750 units

- Year 2 Quarter 2 = 15,000 + (3,000 x 6) = 33,000 – 7.5% = 30,525 units

- Year 2 Quarter 3 = 15,000 + (3,000 x 7) = 36,000 + 5.0% = 37,800 units

- Year 2 Quarter 4 = 15,000 + (3,000 x 8) = 39,000 – 10.0% = 35,100 units

b)

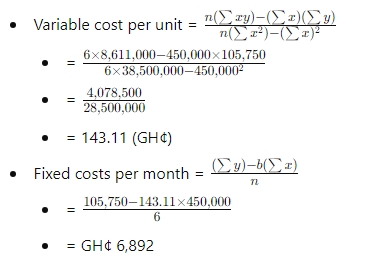

| Direct Labour Hours (x) | Total Overheads (y) | xy | x² |

|---|---|---|---|

| 50,000 | 14,800 | 740,000 | 2,500,000 |

| 80,000 | 17,000 | 1,360,000 | 6,400,000 |

| 120,000 | 23,800 | 2,856,000 | 14,400,000 |

| 40,000 | 11,900 | 476,000 | 1,600,000 |

| 100,000 | 22,100 | 2,210,000 | 10,000,000 |

| 60,000 | 16,150 | 969,000 | 3,600,000 |

| Total | 450,000 | 8,611,000 | 38,500,000 |

c) i) Direct Material Cost Standard:

- Quality Standard: Specifications for the material’s quality.

- Quantity Standard: Amount of material required per unit.

- Price Standard: Cost of the material per unit.

ii) Direct Labour Cost Standard:

- Standard Wage Rate: Rate of pay per hour for workers.

- Standard Labour Time: Amount of time required to complete a unit.

- Efficiency Standard: Expected efficiency level of workers.