Question

Answer

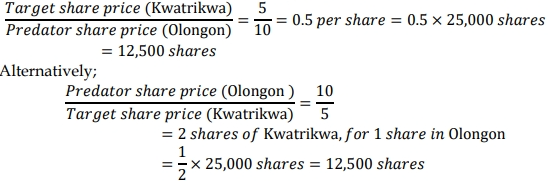

a) Shares of Olongon that should be exchanged for all the share of Kwatrikwa

b) Value of the combined business using the following:

- 𝑀𝑎𝑟𝑘𝑒𝑡 𝑣𝑎𝑙𝑢𝑒 = 𝑇𝑜𝑡𝑎𝑙 𝑠ℎ𝑎𝑟𝑒𝑠 𝑜𝑓 𝑐𝑜𝑚𝑏𝑖𝑛𝑒𝑑 𝑏𝑢𝑠𝑖𝑛𝑒𝑠𝑠 × 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

𝑀𝑎𝑟𝑘𝑒𝑡 𝑣𝑎𝑙𝑢𝑒 = (25,000 + 12,500) × 10 = 𝑮𝑯𝑺𝟑𝟕𝟓, 𝟎𝟎𝟎

𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠 𝑜𝑓 𝑐𝑜𝑚𝑏𝑖𝑛𝑒𝑑 𝑏𝑢𝑠𝑖𝑛𝑒𝑠𝑠 = (0.5 × 25,000) + (0.5 × 25,000) = 𝐺𝐻𝑆25,000

c) Cost of the acquisition if Olongon pays GH¢130,000 in cash for Kwatrikwa.

Cost of Acquisition = Cash paid – Value of Target (Kwatrikwa)

Cost of Acquisition = 130,000 – 125,000 = GH¢5,000

The acquisition is good for Kwatrikwa’s shareholders, they can gain GH¢5,000 for

free.

d) Defensive tactics the management of Kwatrikwa can employ to prevent Olongon

from acquiring the company.

- Staggered board: The board is classified into three equal groups. Only one group

is elected each year. Therefore, the bidder cannot gain control of the target

immediately. - Supermajority: A high percentage of shares, typically 80%, is needed to approve

a merger. - Fair price: Mergers are restricted unless a fair price (determined by formula or

appraisal) is paid. - Restricted voting: Shareholders who acquire more than a specified proportion of

the target have no voting rights unless approved by the target’s board. - Waiting period: Unwelcome acquirers must wait for a specified number of years

before they can complete the merger. - Poison pill: Existing shareholders are issued rights that, if there is a significant

purchase of shares by a bidder, can be used to purchase additional stock in the

company at a bargain price. - Poison put: Existing bondholders can demand repayment if there is a change of

control as a result of a hostile takeover. - Litigation: Target files suit against bidder for violating antitrust or securities laws.

- Asset restructuring: Target buys assets that bidder does not want or that will

create an antitrust problem. - Liability restructuring: Target issues shares to a friendly third party, increases the

number of shareholders, or repurchases shares from existing shareholders at a

premium. - Crown jewels: Crown jewels are options under which a favored party can buy a

key part of the target at a price that may be less than its market value. - Golden parachutes: Golden parachutes are additional compensations to the

target’s top management in the case of termination of its employment following a

successful hostile acquisition.