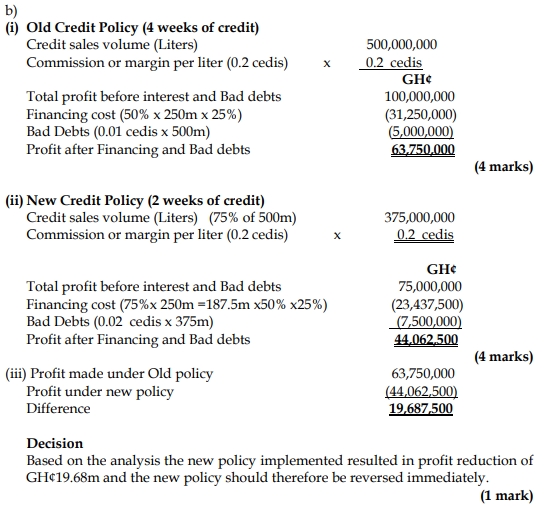

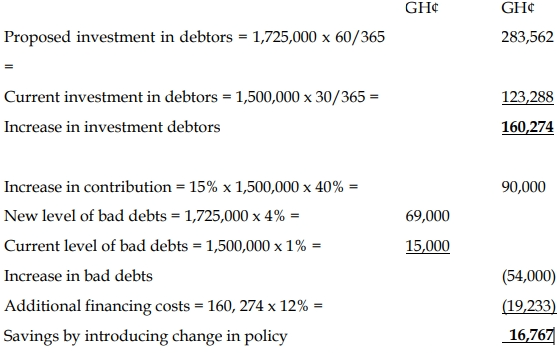

- 13 Marks

Question

Innovate Ghana Ltd is a dealer in household consumables in Ghana. It currently sells on a cash-only basis. The company’s current annual sales are GH¢10 million. The operating cost structure is as follows:

- Cost of sales: 55% of sales

- Staff cost: 10% of sales

- Marketing and distribution cost: 15% of sales

Management in a meeting concluded that introducing credit sales will help boost sales in the light of the current tightness in liquidity in the market, the drive by other competitors, and pressure from the sales team.

It is projected that total sales will grow by 50% solely from the credit sales. The customers are offered 1-month credit, and a new credit department is set up to assess and monitor these credit sales. The monthly cost of running this credit department is GH¢20,000, and bad debts are expected to be 4% of the credit sales.

To finance this credit, Innovate Ghana Ltd will borrow at an interest rate of 25% per annum.

Required:

i) Calculate the total profit before tax before the introduction of the new policy.

(4 marks)

ii) Calculate the total profit before tax after the introduction of the new policy.

(6 marks)

iii) Advise management whether the initiative should be undertaken.

(3 marks)

Answer

i) Total Profit Before Tax Before the Introduction of the New Policy

| Description | Amount (GH¢) |

|---|---|

| Sales | 10,000,000 |

| Cost of Sales (55% of sales) | (5,500,000) |

| Gross Profit | 4,500,000 |

| Staff Cost (10% of sales) | (1,000,000) |

| Marketing & Distribution | (1,500,000) |

| Net Profit Before Tax | 2,000,000 |

(4 marks)

ii) Total Profit Before Tax After the Introduction of the New Policy

| Description | Amount (GH¢) |

|---|---|

| Sales (150% of 10 million) | 15,000,000 |

| Cost of Sales (55% of sales) | (8,250,000) |

| Gross Profit | 6,750,000 |

| Staff Cost (10% of sales) | (1,500,000) |

| Marketing & Distribution | (2,250,000) |

| Credit Admin Cost (20,000 x 12) | (240,000) |

| Bad Debts (4% of credit sales) | (200,000) |

| Interest or Financing Cost | (104,167) |

| Net Profit Before Tax | 2,455,833 |

(6 marks)

iii) Management Advice

Profit before tax after the policy: GH¢2,455,833

Less: Profit before tax before the policy: GH¢2,000,000

Increase in Profit: GH¢455,833

The introduction of the credit sales policy has resulted in an incremental profit of GH¢455,833. Therefore, the initiative should be undertaken as it leads to higher profitability.

(3 marks)

- Topic: Working Capital Management

- Series: MAY 2020

- Uploader: Theophilus