Question

Answer

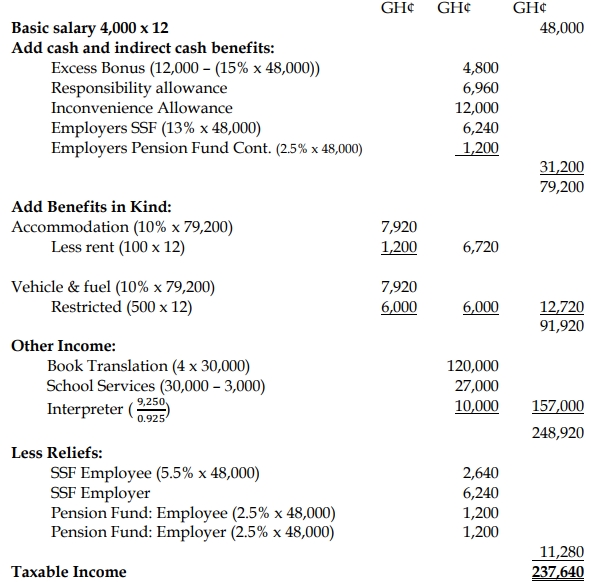

a) Agyeiwaa Grace

Computation of Taxable Income for the 2020 Year of Assessment

b) Possible Gains and Profits from Employment

The following are possible individual gains and profits from employment for a year of assessment:

- Salary, Wages, and Bonuses: Payments such as salary, wages, leave pay, and bonuses are considered part of employment gains.

- Allowances: Personal allowances like cost of living, subsistence, rent, entertainment, and travel allowances.

- Payments for Agreements to Conditions: Payments received for an individual’s agreement to employment conditions.

- Gifts and Benefits in Kind: Gifts or benefits received in respect of employment are taxable gains.

- Retirement Contributions: Contributions made to a retirement fund on behalf of the employee and retirement payments related to employment.

- Discharge of Expenses: Any payments that discharge expenses incurred by the individual or an associate of the individual.