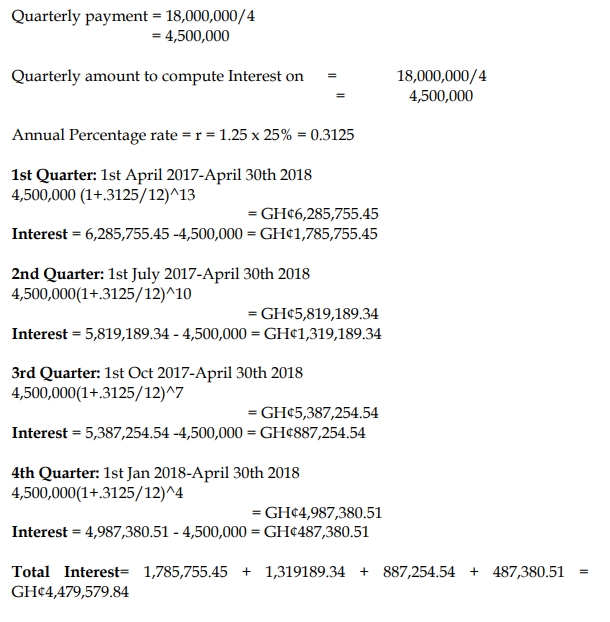

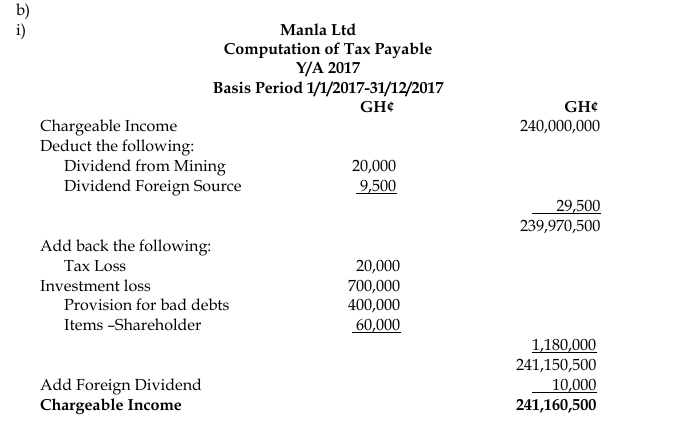

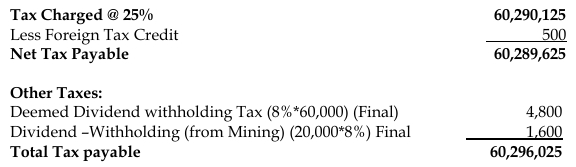

Question

Answer

c) Taxes payable for BMC for each quarter

![]()

Where A = Tax payable (Annual tax payable),

B = All withholding up to the end of the

respective quarter + any other taxes paid in respect of that annual tax payable,

C = the number quarters remaining

1st Instalment

A = 25% X GH¢3,000,000 = GH¢750,000

B = 100,000

C = 4

Instalment payment = (750,000 – 100,000)/4 = GH¢162,500

2nd Instalment

A = GH¢750,000

B = 100,000 + 120,000 +162,500= 382,500

C = 3

Instalment payment = (750,000 – 382,599)/3 = GH¢122,500

3rd Instalment

A = 25% x GH¢4,500,000 = 1,125,000

B = 100,000 + 162,500 + 120,000 + 122,500 + 200,000 = 705,000

C = 2

Instalment payment = (1,125,000 – 705,000)/2 = GH¢210,000

4th Instalment

A = GH¢1,125,000

B = 705,000 + 210000 = 915,000

C = 1

Instalment payment = (1,125,000 – 915,000)/1 = GH¢210,000

(Marks are evenly spread = 10 marks)