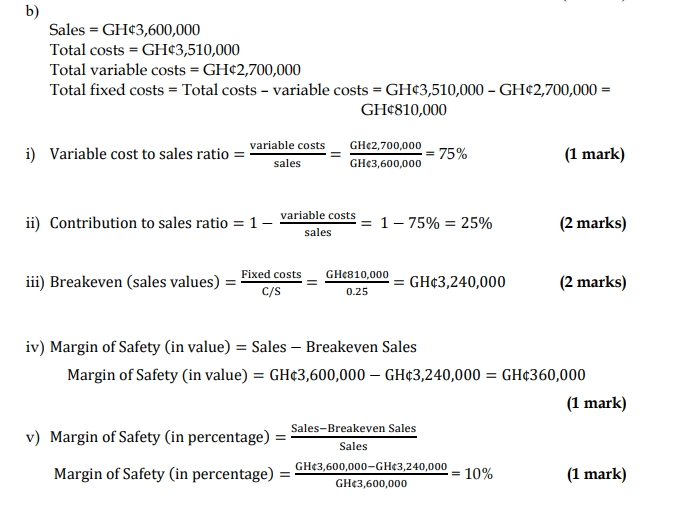

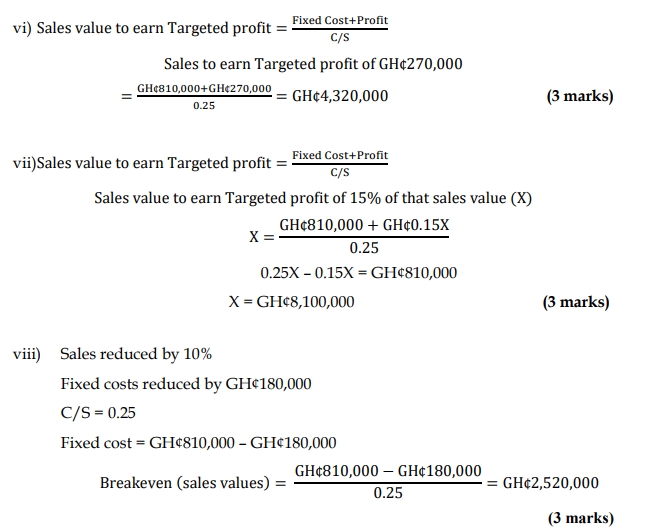

Question

Answer

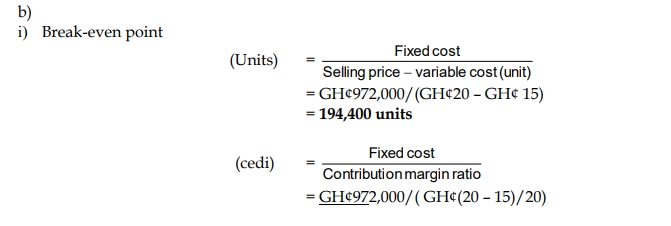

a. Break-even point in units = Total fixed cost / contribution per unit = N160,000/ (20 – 18) = 80,000 units

Break-even point in value = Total fixed cost / contribution Margin Ratio = N160,000/ (2 / 20) = N1,600,000

b. Fixed cost: Fixed Cost = ₦1,600,000

c. Variable cost per unit:

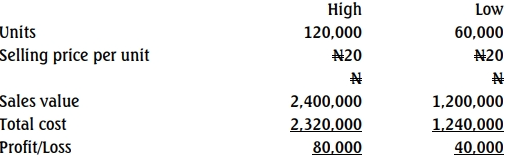

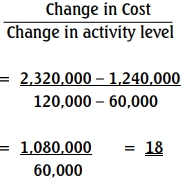

Using High and Low Methods

Variable cost per unit = N18

d. Profit volume ratio: Profit / Volume Ratio = 2 / 20 x 100 = 10%

e. Contribution, assuming 70,000 bottles are sold: 70,000 x N2 = N140,000

f. Margin of safety assuming 90,000 bottles are sold: 90,000 – BEP in units = 90,000 – 80,000 = 10,000 units

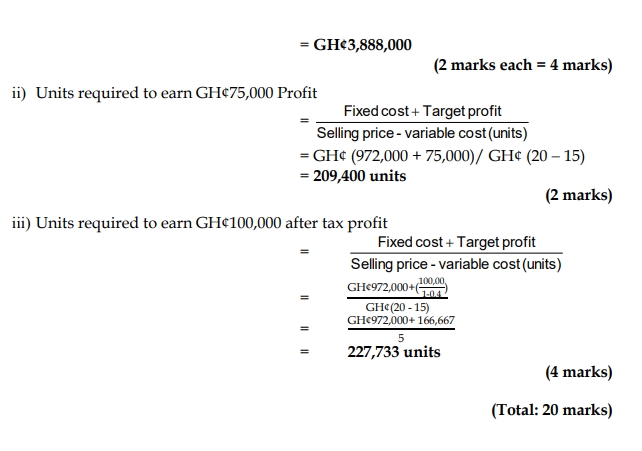

g. The number of bottles to be sold to generate a profit after tax of ₦70,000 assuming the tax rate is 30%:

Sales in units = (Total fixed cost + target profit) / contribution per unit

Target profit = N70,000 / 30% = N233,333

Sales in units = (N160,000 + N233,333)/2 = 196,667 bottles