Question

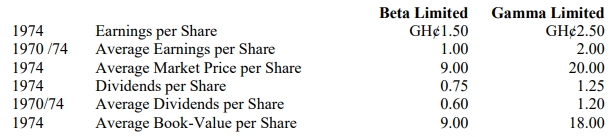

At a meeting of the Directors of the Alpha Company Limited – a privately owned company – in May 1975, the recurrent question is raised as to how the company is going to finance its future growth and at the same time enable the founders of the company to withdraw a substantial part of their investment. A public quotation was discussed in 1974 but because of the depressed nature of the stock market at that time, consideration was deferred. Although the matter is not of immediate urgency, the Chairman of the company – one of the founders – produces the following information which he has recently obtained from a firm of financial analysts in respect of two publicly quoted companies, Beta Limited and Gamma Limited, which are similar to Alpha Limited in respect to size, asset composition, financial structure, and product mix.

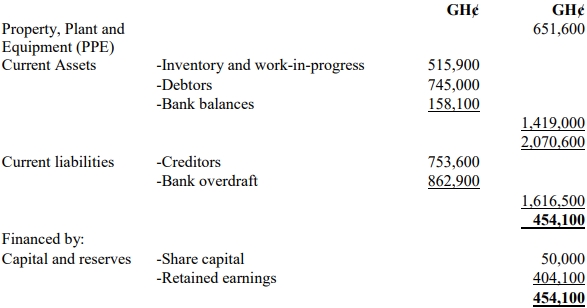

The only information you have available at the meeting in respect of Alpha Limited is the final accounts for 1974, which disclose the following:

Alpha Limited

Share Capital (no variation for 8 years) 100,000 Ordinary GH¢1 Share

Post-Tax Earnings GH¢400,000

Gross Dividends GH¢100,000

Book Value GH¢3,500,000

From memory, you are of the view that the post-tax earnings and gross dividends for 1974 were at least one-third higher than the average of the previous five years.

Required:

i) Use the information provided to answer the Chairman’s question on what Alpha Ltd was worth in 1974.

ii) Discuss FOUR (4) factors to be taken into account in trying to assess the potential market value of shares in a private company when they are first offered for public subscription.

Answer

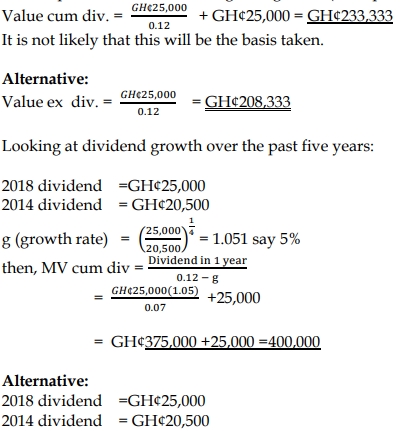

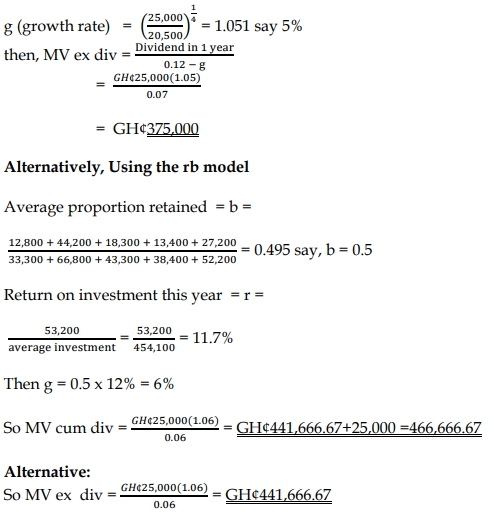

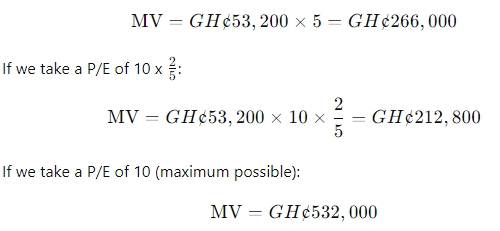

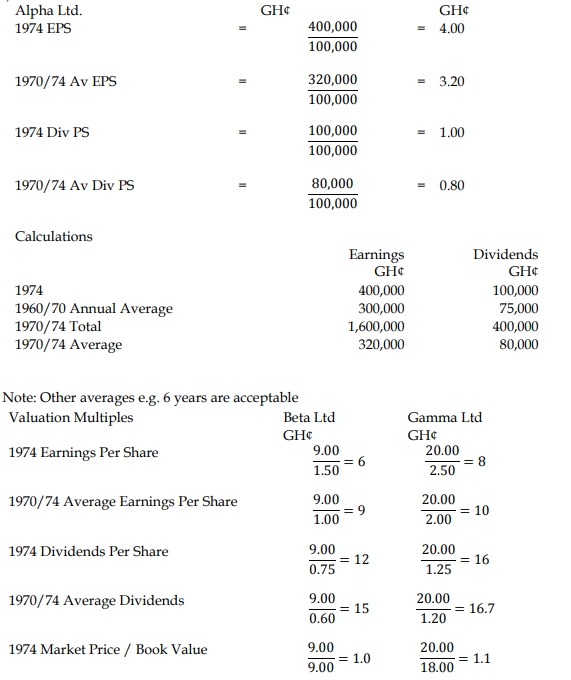

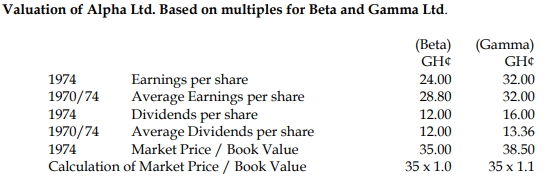

i) Valuation of Alpha Ltd

ii) Factors to Consider in Valuing a Private Company for Public Offering

- Opportunity Cost:

Investors will compare the expected returns from the company’s shares with the returns from alternative investments. If the potential return on investment is not competitive, investors may not subscribe to the shares. - Risk Perception:

The perceived risk of investing in a private company will affect its valuation. Private companies generally carry higher risk, and this may result in a lower valuation due to risk premiums. - Marketability:

The ease with which shares can be traded once they are publicly listed will influence valuation. Less liquid shares may be valued lower due to the risk of being unable to quickly sell them when needed. - Information Asymmetry:

Investors may have limited information about the private company’s operations and finances, which increases uncertainty and can lead to lower valuation. Public companies generally provide more transparency, reducing this gap.