- 1 Marks

FA – Nov 2012 – L1 – SA – Q2 – Financial Statements

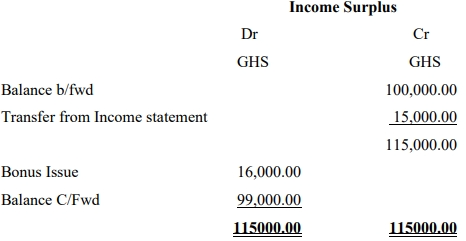

Identifying a non-characteristic of a bonus issue.

Question

Which of these is NOT a characteristic of bonus issue?

A. Increasing capital without diluting current shareholdings

B. Capitalising reserves, so that they cannot be paid as dividends

C. Not raising cash

D. Generating new shares

E. Could jeopardise payment of future dividend if profit declines

Find Related Questions by Tags, levels, etc.

Report an error

You're reporting an error for "FA – Nov 2012 – L1 – SA – Q2 – Financial Statements"

- 1 Marks

FA – Nov 2012 – L1 – SA – Q2 – Financial Statements

Identifying a non-characteristic of a bonus issue.

Question

Which of these is NOT a characteristic of bonus issue?

A. Increasing capital without diluting current shareholdings

B. Capitalising reserves, so that they cannot be paid as dividends

C. Not raising cash

D. Generating new shares

E. Could jeopardise payment of future dividend if profit declines

Find Related Questions by Tags, levels, etc.

Report an error