Question

Answer

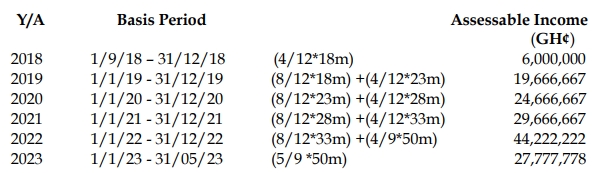

Computation of Assessable Income for Hajia Bintu for all relevant years

Hajia Bintu has been in business from 1 September 2018, preparing accounts to 31 August each year. She ceased to operate the business on 31 May 2023. The agreed profits for the past years of operations are as follows:

| Year | Agreed Profits (GH¢) |

|---|---|

| Year to 30/8/2019 | 18,000,000 |

| Year to 30/8/2020 | 23,000,000 |

| Year to 30/8/2021 | 28,000,000 |

| Year to 30/8/2022 | 33,000,000 |

| Period to 31/5/2023 | 50,000,000 |

Required:

Calculate the assessable income for all relevant years.

Computation of Assessable Income for Hajia Bintu for all relevant years

State the Basis Periods for the following persons as provided in the Income Tax Act, 2015 (Act 896):

i) A sole proprietorship

ii) A company

iii) A trust

iv) A partner of a partnership

The Basis Periods for the different persons are as follows:

i) Sole Proprietorship: The basis period for a sole proprietor is the calendar year (January to December).

ii) Company: The basis period for a company is its accounting year, which may vary depending on the company’s financial reporting period.

iii) Trust: The basis period for a trust is the accounting year of the trust.

iv) Partner of a Partnership: The basis period for a partner in a partnership is the calendar year (January to December).

The determination of a person’s tax liability is in relation to the concept of “Year of Assessment” and “Basis Period”.

Required:

In relation to the statement above, distinguish between the concept of Year of Assessment and Basis Period as used in income taxation.

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.