Question

Answer

a)

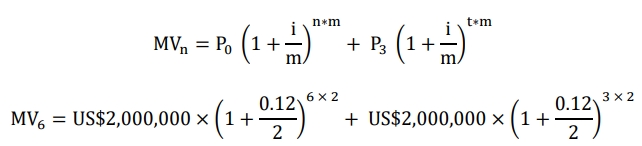

i) Computation of the maturity value of the loan at the end of six years:

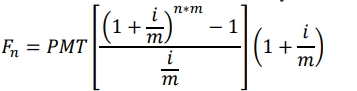

ii) Computation of the size of the quarterly deposits into the sinking fund:

The objective of the sinking fund is to raise money to settle the maturity value of the loan in six years’ time. The future value of the fund (F) should be equal to the maturity value of the loan:

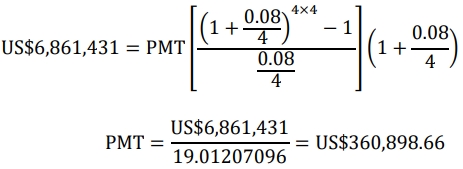

F6 = MV6 = US$6,861,431

As the deposits are to be made at the beginning of each period, this case is an annuity due. The future value formula of an annuity due is used:

Where:

- Future value = US$6,861,431

- Annual interest rate,

- Investment period, years (year 3 to year 6)

- Frequency,

iii) Comparing and contrasting annuity due and ordinary annuity:

Annuity due and ordinary annuity are both forms of a series of equal cash flows. They are similar in the amount of cash flows in the series and the time interval between the cash flows. In both cases, the cash flows are equal in size and occur within the same time interval (e.g., monthly, quarterly).

The difference between the two lies in the timing of the cash flows:

- Annuity Due: Cash flows occur at the beginning of each period.

- Ordinary Annuity: Cash flows occur at the end of each period.

(Marks allocation: 3 marks)

b)

i) Justify the type of option Klessy should buy:

A call option gives the holder the right to buy the underlying asset at an agreed price before or on the expiration date. In contrast, a put option gives the holder the right to sell the underlying asset at an agreed price before or on the expiration date. Klessy should buy call options on the Australian dollar. Klessy needs to buy the Australian dollar next month to settle the invoice value of the consignment of barley bought. Thus, it needs to buy call options to get the right to buy the Australian dollar at the quoted strike price.

(Marks allocation: 3 marks)

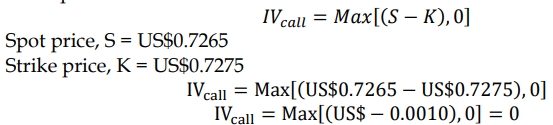

ii) Computation and interpretation of the intrinsic value of the call option:

The intrinsic value of a call option is the maximum of the spot price minus the strike price and zero:

The intrinsic value of the call option is zero, meaning the call option is currently out-of-the-money and will not be profitable to exercise now.

(Marks allocation: 4 marks)

iii) The distinction between option premium and option strike price:

- Option Premium: The price paid for the right to trade the underlying asset at a given strike price before or on a specified expiration date. For example, Klessy would have to pay US$0.0131 to obtain the right to buy one Australian dollar.

- Option Strike Price: The agreed price for the underlying asset. If Klessy buys the call option and elects to exercise the option, it will pay US$0.7275 for every Australian dollar in the contract. The premium is payable when the option contract is bought, while the strike price is payable later when the option is exercised, and the asset is traded.

(Marks allocation: 3 marks)