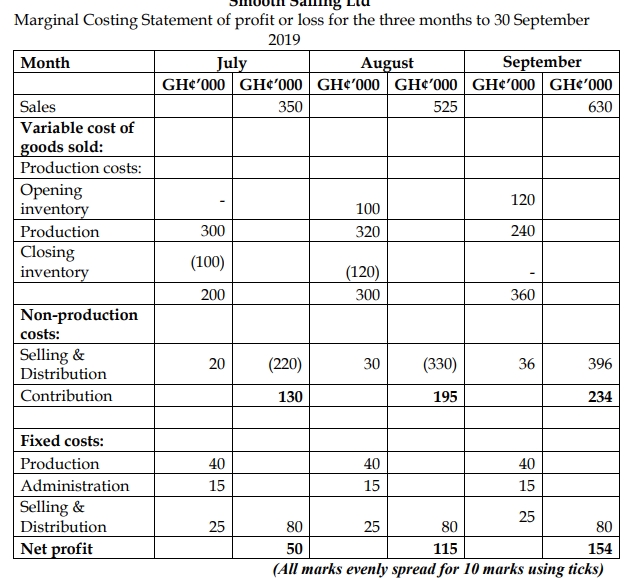

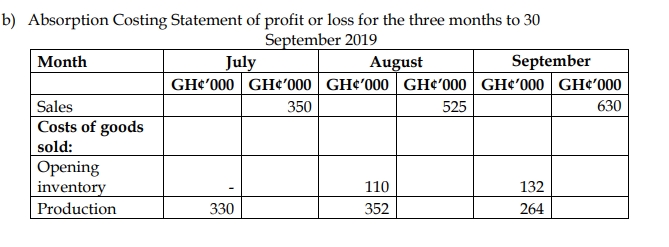

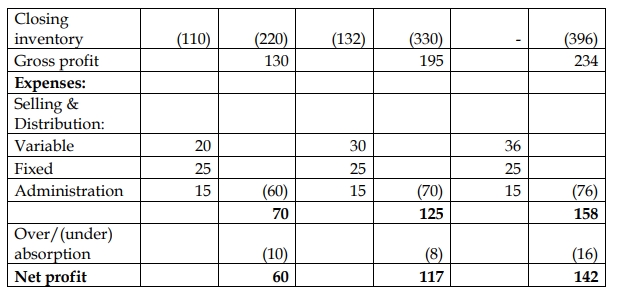

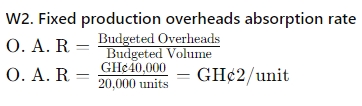

Question

Answer

i. Full production cost per unit and value:

Production in units = 25 000 000 / 4 = 625,000 units

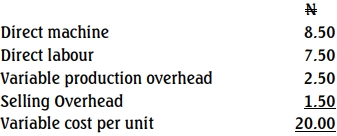

ii. Variable cost per unit and value:

Value 625,000 x N20.00 = 12,000,000

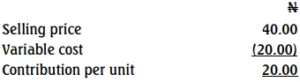

iii. Contribution per unit and value

Value 625,000 x N20.00 = 125,000,000

iv. Break even point in value

![]()

![]() = N15,000,000

= N15,000,000

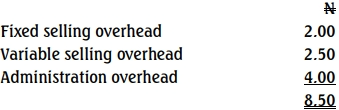

v. Total non-production cost per unit and value

Value 625,000 x N8.50 = N5,312,000

vi. New break-even cost point

= ![]()

= ![]()

= ![]() = N18,243,243

= N18,243,243