Question

Answer

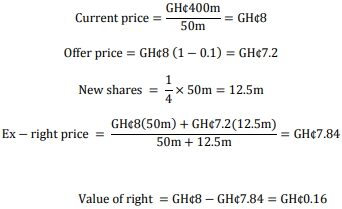

i) Value of a Right

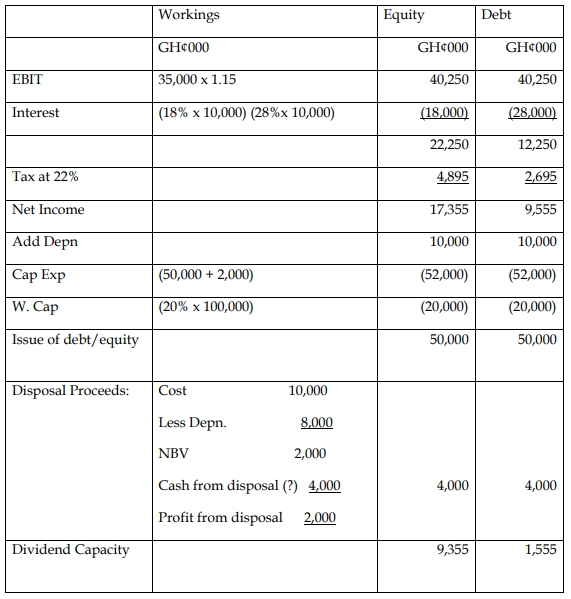

ii) Dividend Capacity Forecast

Conclusion:

Asana would be able to meet its dividend capacity requirement if equity finance is used, as the dividend capacity (GH¢7.81 million) exceeds the minimum required. However, under debt financing, the dividend capacity (GH¢4.30 million) would not meet the required threshold, and the company would not be able to pay dividends.

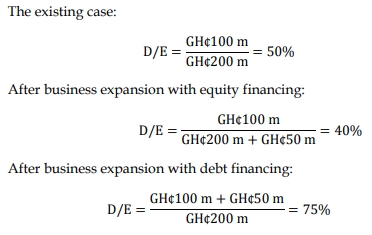

iii) Debt-to-Equity Ratio

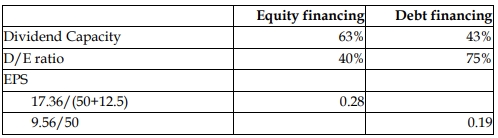

iv) Evaluation of Financing Methods

- If equity finance is used, the company will have a lower debt-to-equity ratio (40%) and be able to pay dividends to shareholders, meeting both debt and dividend requirements.

- If debt finance is used, the company will have a higher debt-to-equity ratio (75%) close to the maximum limit of 80%, leaving little room for future borrowing. Additionally, the company will not meet the minimum dividend capacity requirement.

Conclusion: Equity finance is the better option for the planned business expansion.