Question

Answer

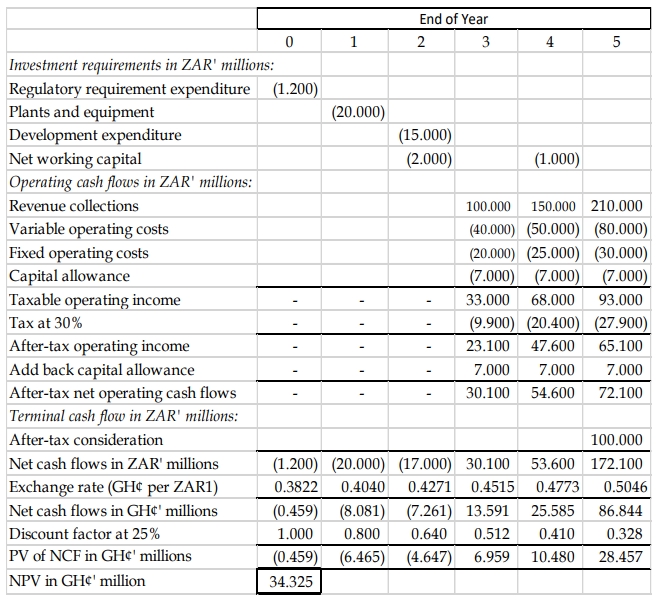

Evaluation of mining project using NPV with no restriction on repatriation

The project’s NPV

Recommendation:

The positive NPV of GH¢34.325 million suggests that the investment should be accepted as it will enhance the value of Rock Minerals Ltd.

Workings:

- Capital Allowance: Capital allowance is granted at 20% per annum on ZAR35 million starting from year 3, resulting in ZAR7 million of annual capital allowance.

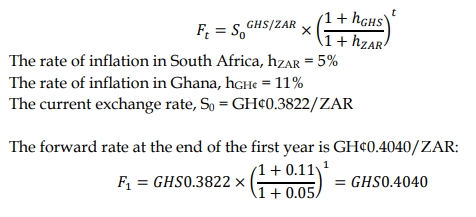

- Exchange Rate Forecasting: Forecasted exchange rates based on purchasing power parity, assuming inflation rates of 11% in Ghana and 5% in South Africa