Question

Answer

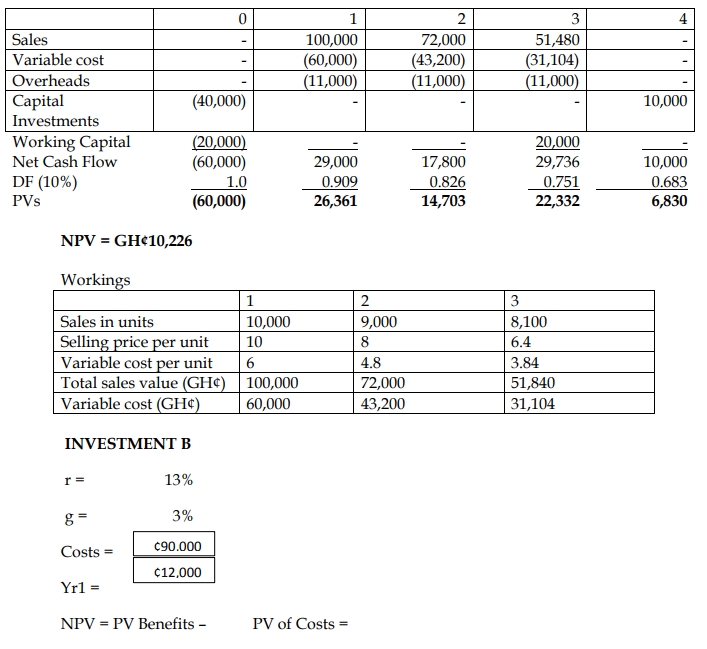

a) Net Present Value (NPV) Analysis (15 marks):

Investment A:

Recommendation:

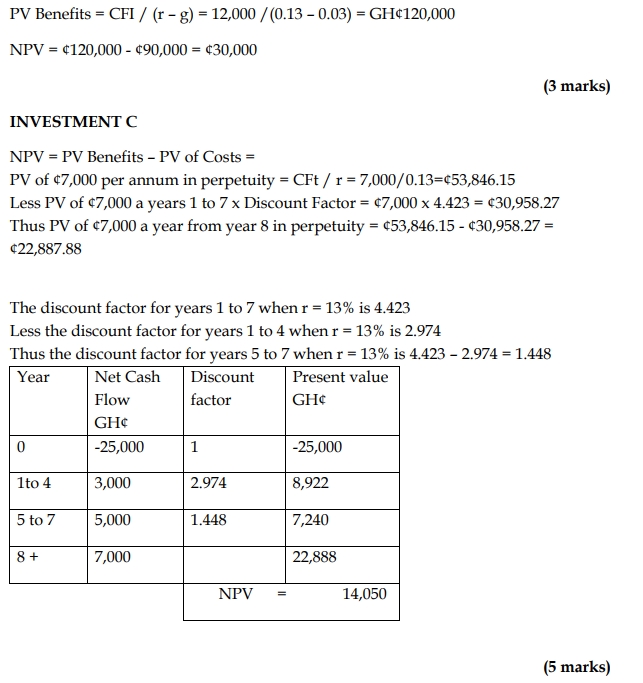

All projects have positive NPVs and should be undertaken, but Investment B is the most attractive with the highest NPV (GH¢30,000), followed by Investment A and Investment C.

b) Internal Rate of Return (IRR) Analysis (5 marks):

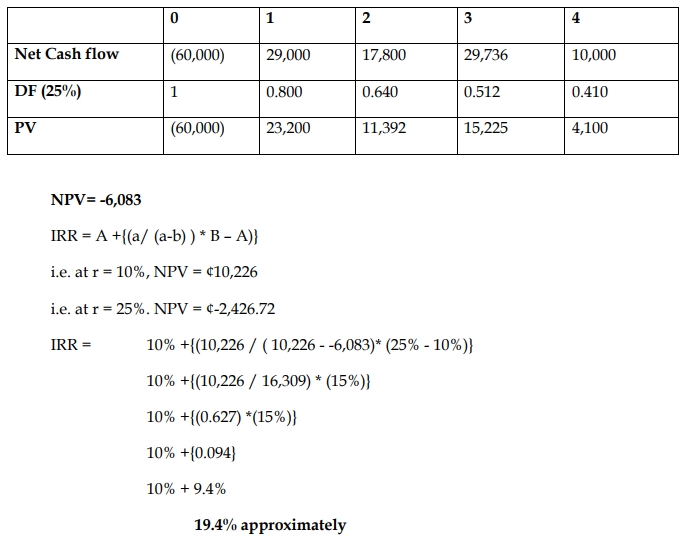

Investment A:

Conclusion:

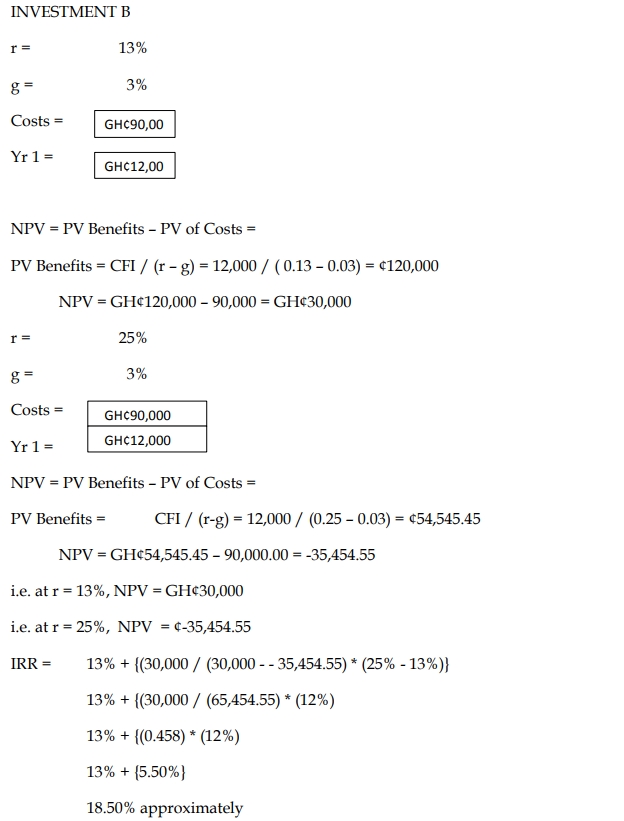

Both Investment A and Investment B have IRRs above their required rates of return (10% for A and 13% for B). Investment A has a higher IRR (19.4%) than B (18.5%), but Investment B remains more favorable due to its higher NPV.