Question

Answer

i) Net Assets Method

To value Tinto Ltd using the Net Assets Method, the adjustments to the net assets based on the information provided are as follows:

| Adjustments to Net Assets of Tinto Ltd | Amount (GH¢ million) |

|---|---|

| Net assets per financial statements | 14.40 |

| Revaluation surplus on buildings | +1.50 |

| Fair value adjustment on financial assets | +0.10 |

| Allowance for bad debts | -0.75 |

| Impairment of plant | -0.02 |

| Revised Net Assets | 15.23 |

Thus, the value of the business using the Net Assets Method is GH¢15.23 million.

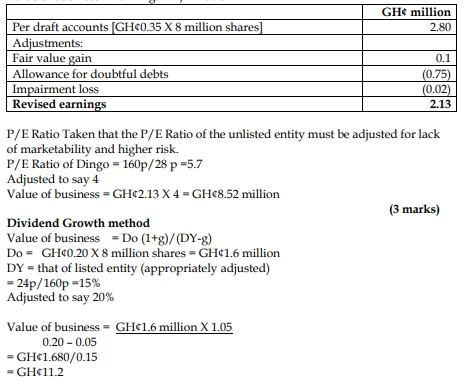

ii) Price-Earnings Method

To value Tinto Ltd using the Price-Earnings (P/E) Method, the earnings and the appropriate P/E ratio must be calculated and adjusted for risk and marketability.