Question

Answer

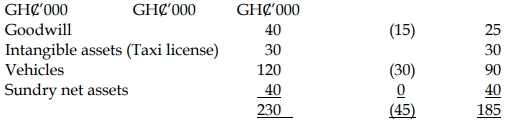

Under IAS 36 Impairment of Assets, Afoko Ltd must determine the recoverable amount of the taxi business, which is the higher of fair value less costs to sell and value in use. If the recoverable amount is lower than the carrying amount, an impairment loss should be recognized.

Steps to account for impairment:

Determine the carrying amount of the business as of 1 February 2015:

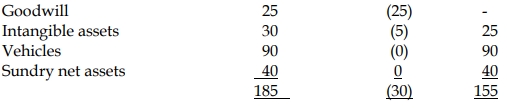

Determine the recoverable amount as of 1 March 2015:

In this case, since there is no goodwill, the impairment loss should be allocated to the remaining assets. The intangible asset (taxi license) would likely be impaired due to the competitive pressures from the rival company.

Conclusion:

Afoko Ltd should recognize an impairment loss of GH¢10,000 in its financial statements, reducing the carrying amount of the intangible asset (taxi license).