- 8 Marks

Question

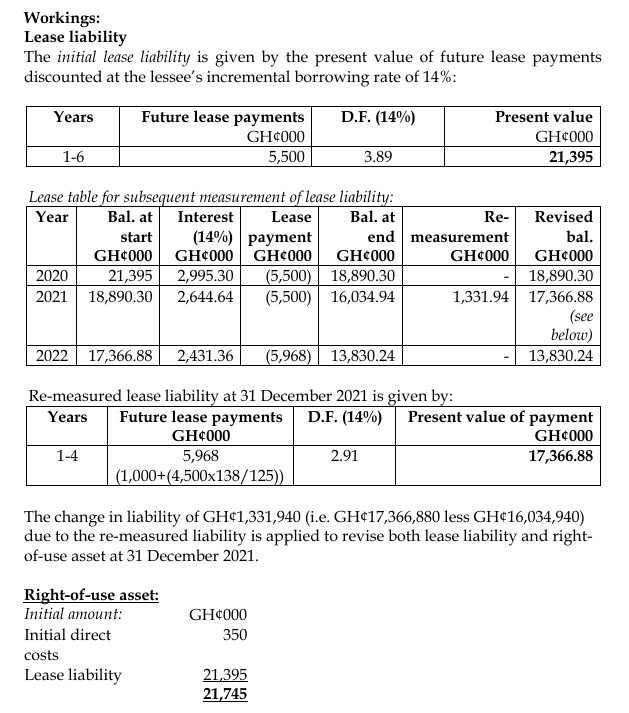

On 1 January 2020, Zigi Plc (Zigi) entered into a 6-year lease of a manufacturing plant with annual lease payments of GH¢5.5 million, starting from 31 December 2020. The lease agreement specified that the lease payments (except yearly baseline payments of GH¢1 million included in the GH¢5.5 million) would increase every two years on the basis of the Consumer Price Index (CPI) for the preceding 24 months. The CPI at the commencement date was 125. Additionally, Zigi is required to pay GH¢500,000 every year once cost savings in that year reach at least GH¢6 million. Zigi’s cost savings achieved with its other assets had been averaging GH¢5.1 million prior to 1 January 2020. The initial direct non-reimbursable cost incurred by Zigi was GH¢350,000.

The rate implicit in the lease, which should have been 12% per annum, was not readily determinable by Zigi. Zigi’s incremental borrowing rate was 14% per annum. At 31 December 2021, the CPI was revised to 138. The actual cost savings achieved by Zigi in the years ended 31 December 2020 and 31 December 2021 were GH¢5.3 million and GH¢6.8 million, respectively.

The cumulative discount factors based on 12% and 14% are provided below:

| Years | 12% | 14% |

|---|---|---|

| 6 | 4.11 | 3.89 |

| 5 | 3.60 | 3.43 |

| 4 | 3.04 | 2.91 |

Required:

In accordance with IFRS 16: Leases, explain how the above lease would affect Zigi’s financial statements for the years ended 31 December 2020 and 2021.

(Total: 8 marks)

Answer

- Tags: CPI Adjustments, Finance Costs, Lease Liability, Right-of-Use Asset, Variable Payments

- Level: Level 3

- Topic: IFRS 16: Leases

- Series: DEC 2022

- Uploader: Dotse