Question

Answer

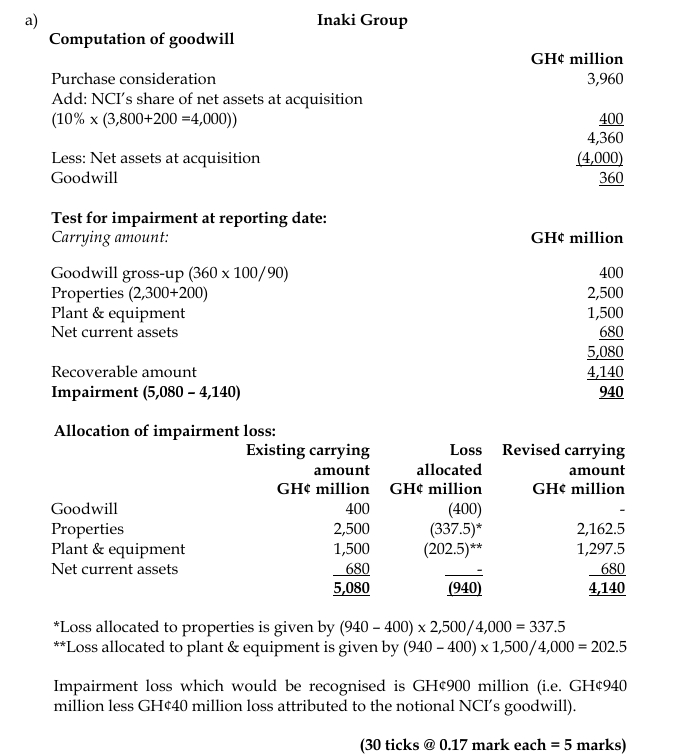

Computation of goodwill:

| GH¢ million | |

|---|---|

| Purchase consideration | 3,960 |

| Add: NCI’s share of net assets at acquisition (10% x (3,800+200 =4,000)) | 400 |

| Total | 4,360 |

| Less: Net assets at acquisition | (4,000) |

| Goodwill | 360 |

Test for impairment at reporting date:

| GH¢ million | |

|---|---|

| Goodwill gross-up (360 x 100/90) | 400 |

| Properties (2,300 + 200) | 2,500 |

| Plant & equipment | 1,500 |

| Net current assets | 680 |

| Total carrying amount | 5,080 |

| Recoverable amount | 4,140 |

| Impairment | (940) |