Question

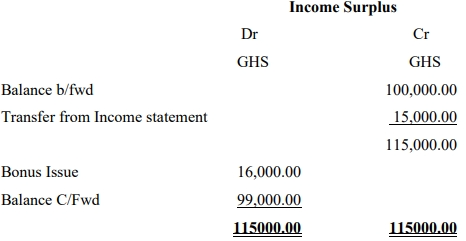

The following is a statement of retained earnings:

Required:

What is the tax implication, if any, on the above income statement?

The following is a statement of retained earnings:

Required:

What is the tax implication, if any, on the above income statement?