Question

b) Abigail Acheampong is in the process of preparing budgets for the period October to December 2017. The following information has been provided to assist in the budgeting process:

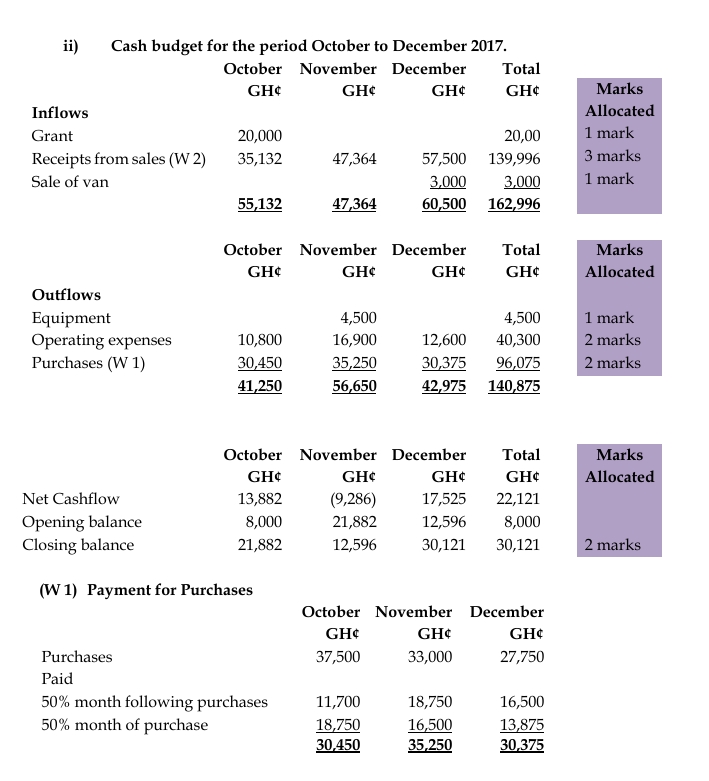

- Sales are 20% cash and 80% credit. Credit sales are collected over a three month period, 15% in the month of sale, 70% in the month following sale and 15% in the second month following sale. Bad debts of 5% are anticipated on all credit sales.

- Total sales revenue in August amounts to GH¢30,000 and September’s total sales revenue amounts to GH¢36,000.

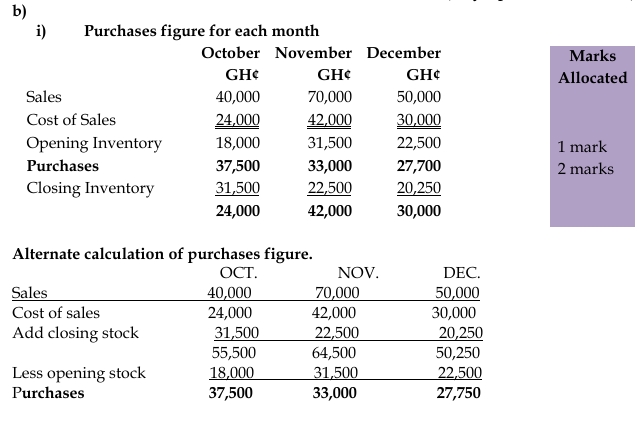

- Cost of sales is expected to amount to 60% of sales revenue each month.

- The business maintains its closing inventory levels at 75% of the following month’s cost of sales. Inventory at the beginning of October is expected to amount to GH¢18,000.

- 50% of inventory purchased is paid in the month of purchase. The remaining 50% is paid for in the month following purchase. As at 30 September 2017, amount owed for purchases are GH¢11,700.

- A grant of GH¢20,000 is expected to be received in mid-October.

- A second hand van which cost GH¢8,000 three years ago is expected to be sold in December 2017 for GH¢3,000. At this time the expected net book value of the van is GH¢1,800.

- Equipment costing GH¢4,500 will be purchased and paid for in November 2017. The equipment will be depreciated on a straight line basis over three years.

- Operating expenses are paid as incurred. These have been estimated as follows: GH¢ October 12,800 November 18,900 December 14,600 The above figures include depreciation on existing assets of GH¢2,000 per month.

- The cash balance on 1 October is expected to amount to GH¢8,000

Required: i) Calculate the purchases figure for each month from October 2017 to December 2017.

(3 marks)

ii) Prepare a cash budget on a monthly basis and in total for the period October 2017 to December 2017. (12 marks)

Answer